This is the advanced Q4 GDP and it's a blow out. GDP increased 5.7% in Q4 2009.

Party on Garth! This is an advanced report, so there might be significant revisions. Recall Q3 2009 GDP originally came in at 3.5% and was revised down to 2.2%.

The acceleration in real GDP in the fourth quarter primarily reflected an acceleration in private inventory investment, a deceleration in imports, and an upturn in nonresidential fixed investment that were partly offset by decelerations in federal government spending and in PCE.

Just a little bit, investment is a blow out at 39.3% increase!

One must wonder how much of the business investment credit from the Stimulus, which was a 50% bonus depreciation, and allows a 50% write off on business investments in the first year, is the reason for this private inventory investment acceleration.

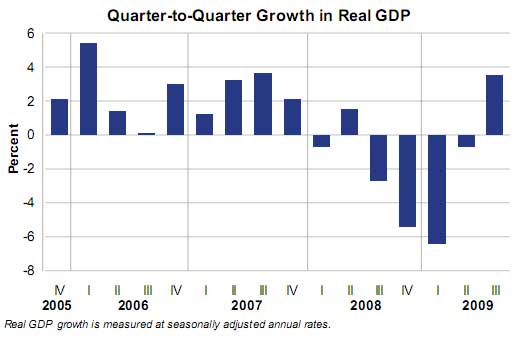

All three major indices surged higher following reports that GDP grew 3.5% in the third quarter. That was better than the 3.2% rate economists were expecting.

CNBC has an interesting news bit about something Volker said. First off, let me give kudos to AmericaBlog for first picking this up. In a meeting at the White House, the famed former Fed chairman basically said we need to rebalance the economy. That to have a GDP where over half (well 70% give or take) is due to consumption is not sustainable long term.

The alternatives to help bolster future economic growth include boosting exports, applying innovative technology to green issues and improving the nation's infrastructure, Volcker said.

The former Federal Reserve chairman, who now heads the White House Economic Recovery Advisory Board, said Obama understands that "We cannot have so much consumption."

The Bureau of Economic Analysis put out a information release showing the GDP slowdowns of U.S. metro areas in 2008.

The dark blue is the biggest increase in GDP, the darker tan is the biggest decrease.

New statistics released today by the U.S. Bureau of Economic Analysis show that the slowdown in U.S. economic growth was widespread: 60 percent of metropolitan areas saw economic growth slow down or reverse. Real GDP growth slowed in 220 of the nation’s 366 metropolitan statistical areas (MSAs) in 2008 with downturns in construction, manufacturing, and finance and insurance restraining growth in many metropolitan areas. Growth in real U.S. GDP by metropolitan area slowed from 2.0 percent in 2007 to 0.8 percent in 2008.

We know you go home and stroke that GDP, salivating at the prospect of that magic number turning positive so you can deny all that is wrong with the economy...but Joseph Stiglitz just called you out:

Most governments make a fetish out of it. If you take one message out of our report, make it avoid GDP fetishism. The message is to encourage political leaders away from that.

So many things that are important to individuals are not included in GDP. There needs to be an array of numbers but we need to understand the role of each number. We may not be able to aggregate everything together.

The article cites examples, such as increased consumer debt contributing to GDP but not adding to economic output in reality.

Andrew Leonard has a short piece over at Salon titled, Chicago School: Bloodied But Unbowed. It's an interesting little piece full of links to previous articles and statements. It also includes this zinger:

.... some of the Chicago economists don't sound a whole lot different from your typical South Carolina Republican. Here's Sam Peltzman, the Ralph and Dorothy Keller distinguished service professor emeritus of economics (italics mine):

"This experience is going to seal the tomb on socialism for all time," he says. "If this can't bring it back, it's hard to think about what could." A burst of Keynesianism should surprise no one, he argues. Of course we hope the government can step in and save the economy. In a crisis people "become infantilized and go back to what's comforting to you as a child."

It looks like you weren't crazy after all. This Depression really is as bad as it seems.

(Bloomberg) -- The first 12 months of the U.S. recession saw the economy shrink more than twice as much as previously estimated, reflecting even bigger declines in consumer spending and housing, revised figures showed.

The Commerce Department’s Bureau of Economic Analysis actually went back and revised their economic figures all the way to 1929, although most of the revisions are since 1997. So as not to bore you with too many details, I'll keep this short and sweet and only touch on the highlights.

February 14th, 2008 – Paulson: (the economy) "is fundamentally strong, diverse and resilient."

Recent comments