The Consumer Price Index for February 2011 increased 0.5% from last month. For the year, the Consumer Price Index for all Urban Consumers (CPI-U) has risen 2.1%. January CPI was 0.4%.

The Consumer Price Index for January 2011 increased 0.4% from last month. For the year, the Consumer Price Index for all Urban Consumers (CPI-U) has risen 1.6%. December CPI was revised to 0.4%.

The Federal Reserve has a dissident in their midst who is about to get FOMC voting rights. Philadelphia Federal Reserve President Charles I. Plosser gave one wallop of a speech making it very clear he disagrees with the Federal Reserve bailing out the Banksters and the Housing Market. He also disagrees with intervention in assets as well as giving the illusion the Federal Reserve can really do something about unemployment. From the speech:

I have suggested that the System Open Market Account (SOMA) portfolio, which is used to implement monetary policy in the U.S., be restricted to short-term U.S. government securities. Before the financial crisis, U.S. Treasury securities constituted 91 percent of the Fed’s balance-sheet assets. Given that the Fed now holds some $1.1 trillion in agency mortgage-backed securities (MBS) and agency debt securities intended to support the housing sector, that number is 42 percent today. The sheer magnitude of the mortgage-related securities demonstrates the degree to which monetary policy has engaged in supporting a particular sector of the economy through its allocation of credit. It also points to the potential challenges the Fed faces as we remove our direct support of the housing sector.

The Consumer Price Index for November 2010 increased 0.1% from last month. For the year, the Consumer Price Index for all Urban Consumers (CPI-U) has risen 1.1%. Core CPI, or all items less food and energy, also increased, 0.1%, it's first increase in 4 months. For the year, core CPI, or minus food and energy, is off it's record lows, now at 0.8%.

The Consumer Price Index for October 2010 increased 0.2% from last month. For the year, the Consumer Price Index for all Urban Consumers (CPI-U) has risen 1.2%. The increase this month was all gas. The energy index increased 2.6% with gas jumping 4.6% in a month. Core CPI, or all items less food and energy, was unchanged, 0.0%, now three months in a row.

The Producer Price Index for finished goods increased 0.4% in October 2010. The PPI measures prices obtained for U.S. goods. Intermediate goods prices increased 1.2% and crude or raw materials prices went up 4.3%. PPI is often called wholesale inflation by the press.

The reason finished goods prices increased was all energy, up 3.7% in one month.

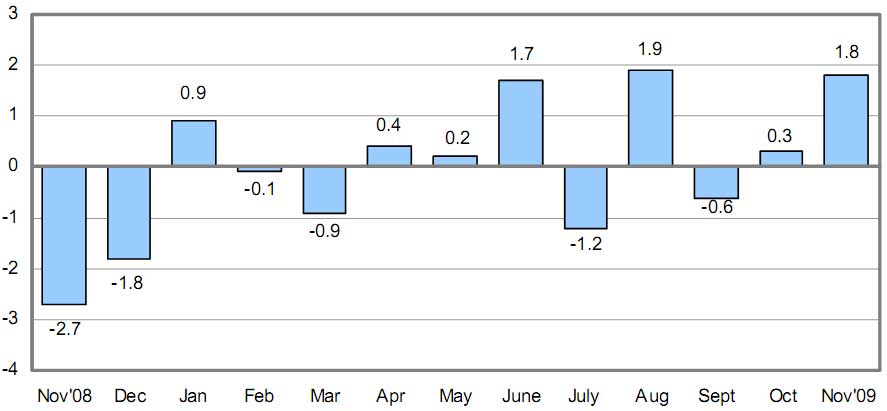

The Producer Price Index, otherwise known as PPI, rose 1.8% on finished goods for November 2009. Graphs below in two different flavors, percent change for the year and aggregate:

In a new op-ed Joseph Stiglitz argues that due to the national debt (projected to be $9.05 trillion over the next 10 years), America should get on the we need a new reserve currency beyond the dollar bus. Kind of a if you can't beat 'em, join 'em message. (see China and the Dollar for details on the Chinese game of chicken while pushing for a new reserve currency).

Our budget deficit, as well as the Federal Reserve's ballooning lending programs and other financial obligations, will accelerate a process already well underway -- a changing role for the U.S. dollar in the global economy.

Producer prices for finished goods declined (-2.8%) on a non-seasonal basis in October, a much greater decrease than expected. On a year-over-year basis, the rate of producer price inflation has declined from 9.8% in July to 5.1% in October. We can expect this decline to continue when this month's number is released in a month, because producer prices had increased 2.6% in November 2007 alone.

This is a slice of good news. Typical post-WW2 recessions have ended at roughly the time when both the rate of producer price and consumer price inflation are declining (check), producer prices are declining faster than consumer prices (almost certainly check), and producer price inflation is less than consumer price inflation (not yet, but maybe in a month). That means producer profits margins are increasing, which makes business expansions more likely.

Cross your fingers that the decline isn't simply measuring our trajectory towards a full-fledged deflationary spiral.

Philadelphia Federal Reserve President Charles I. Plosser gave one wallop of a speech making it very clear he disagrees with the Federal Reserve bailing out the Banksters and the Housing Market. He also disagrees with intervention in assets as well as giving the illusion the Federal Reserve can really do something about unemployment. From

Philadelphia Federal Reserve President Charles I. Plosser gave one wallop of a speech making it very clear he disagrees with the Federal Reserve bailing out the Banksters and the Housing Market. He also disagrees with intervention in assets as well as giving the illusion the Federal Reserve can really do something about unemployment. From

Recent comments