The Federal Reserve Industrial Production & Capacity Utilization report shows a 1.0% increase in industrial production for September. Manufacturing alone grew by 0.5%, cancelling out last month's -0.5% decline. Utilities exploded with a 3.9% monthly increase. Mining grew by 1.8%, also a sizable amount for a month. The G.17 industrial production statistical release is also known as output for factories and mines. This is the largest industrial production monthly gain since September 2012.

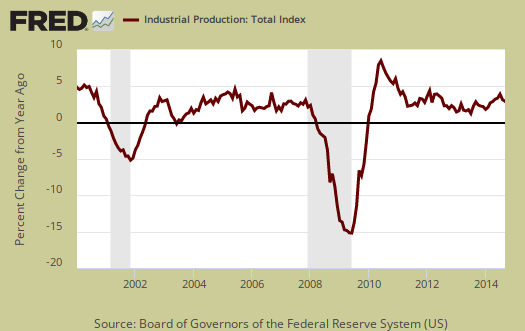

Total industrial production has increased 4.3% from a year ago. Currently industrial production is 5.1 percentage points above the 2007 average. Below is graph of overall industrial production's percent change from a year ago.

For Q3, overall industrial production increased 3.2% annualized. The breakdown is manufacturing production increased 3.5% annualized, the output from mines was an annualized 8.7%, while utilities dropped -8.5%. Utilities output has contracted for two quarters in a row.

Here are the major industry groups industrial production percentage changes from a year ago. We can see the sudden jump up from utilities this month isn't a trend at all.

- Manufacturing: +3.7%

- Mining: +9.1%

- Utilities: +0.9%

Manufacturing output is just a smidge 0.5 points above it's the 2007 average. Below is a graph of just the manufacturing portion of industrial production.

Within manufacturing, durable goods increased 0.4% for the month and has increased 6.6% annualized for Q3. Manufacturing durable goods has increased every quarter since 2009.

Nondurable goods manufacturing increased by 0.5% for the month and increased 1.1% for Q3, annualized.

Publishing is clearly dying as the Fed reports a downward trend for the last 15 years. The non-NAICS industries, primarily logging and publishing are contracting. From the report:

The output of non-NAICS manufacturing industries (publishing and logging) was unchanged in September following a decrease of 0.6 percent in August. The index dropped at an annual rate of 12.5 percent in the third quarter. As a result of continuing declines in the index for publishing, the output of non-NAICS manufacturing industries has trended downward over the past 15 years.

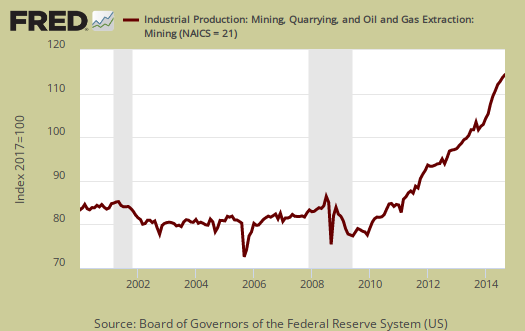

Mining with U.S. oil & gas production is growing. Mining showed a 1.8% monthly increase and for the year has increased 9.1%.

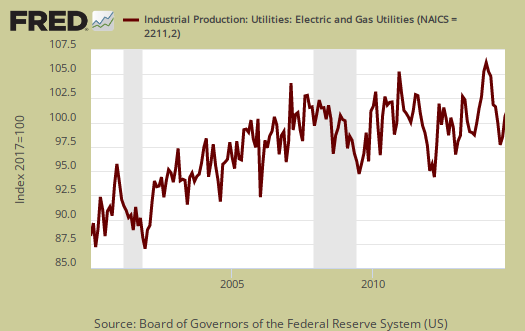

Utilities are volatile due to weather and why the below graph shows the wild swings. It is guessed air conditioning is the reason for September's 3.9% monthly spike in utilities.

There are two reporting methodologies in the industrial production statistical release, market groups and industry groups. Market groups is output bundled together by market categories, such as business equipment or consumer goods. Industrial output is by NAICS codes and is for all manufacturing, or all types of durable goods manufacturing*. Below is the Fed's description of Market groups from the report and their monthly percent changes.

The production of consumer goods rose 0.5 percent in September but decreased at an annual rate of 0.6 percent in the third quarter. After having dropped 3.6 percent in August, the output of consumer durables declined 0.3 percent further in September. Within consumer durables, losses in the indexes for automotive products and for home electronics slightly outweighed gains elsewhere. The production of non-energy nondurables moved up 0.3 percent, while the output of consumer energy products gained 2.2 percent. Within non-energy nondurables, gains in the indexes for clothing and for chemical products were partly offset by a decrease in the production of paper products.

The production of business equipment increased 0.3 percent in September; the indexes for transit equipment and for information processing equipment each moved up 0.5 percent or more, while the output of industrial and other equipment was unchanged. For the third quarter, the index for overall business equipment advanced at an annual rate of 4.9 percent, with gains in all three of its major categories.

The production of defense and space equipment rose 1.4 percent in September. The index increased 3.2 percent at an annual rate in the third quarter after having gained 4.6 percent in the second quarter.

Among nonindustrial supplies, the production of construction supplies rose 0.4 percent in September and moved up at an annual rate of 10.2 percent in the third quarter; nevertheless, output in September was more than 10 percent below its level just prior to the most recent recession. The index for business supplies gained 1.4 percent in September and increased at an annual rate of 1.8 percent in the third quarter.

The output of materials rose 1.4 percent in September and advanced at an annual rate of 4.6 percent in the third quarter. Durable materials recorded an increase of 0.7 percent in September; among its components, the indexes for equipment parts and for other durable materials moved up and the output of consumer parts fell. The output of nondurable materials rose 0.7 percent, with increases in all of its major components. The output of energy materials jumped 2.3 percent in September and rose at an annual rate of 4.4 percent in the third quarter; the index has increased in each quarter since the second quarter of 2011.

Capacity utilization, or of raw capacity, how much is being used, for total industry is 79.3%, a 0.6 percentage point monthly increase. How much plants are utilized is now 0.8 percentage points below the average from 1972 to 2013. Capacity utilization has increased 1.0 percentage points from a year ago. Manufacturing capacity utilization is now 77.3% and is 1.1 percentage points higher than a year ago. Mining capacity utilization is 90.1% and is up 0.6 percentage points from a year ago. Utilities use of it's capacity is 79.2% and this is no change from a year ago. Manufacturing is still 1.4 points below the long term average (1972-2013).

Capacity utilization is how much can we make vs. how much are we currently using, of what capacity is available now, or output rate. Capacity utilization is also called the operating rate. Capacity utilization is industrial production divided by raw capacity.

Capacity growth is raw capacity and not to be confused what what is being utilized. Instead, this is the actual growth or potential to produce. Capacity is the overall level of plants, production facilities, and ability to make stuff, that we currently have in the United States. Capacity growth overall has increased 2.9 percentage points from a year ago. Below is the capacity growth increase from a year ago of the subcategories which make up industrial production.

- Manufacturing: +2.1%

- Mining: +8.3%

- Utilities: +1.0%

Below is the Manufacturing capacity utilization graph, normalized to 2007 raw capacity levels, going back to the 1990's. Here is where offshore outsourcing really shows up.

Here are our previous overviews, only graphs revised. The Federal Reserve releases detailed tables for more data, metrics not mentioned in this overview.

All this seems to look good, yet most people don't seem to

be benefiting from it. Except for a couple of charts one wouldn't know that 7 million families have been foreclosed on, we have maybe 9 million loans underwater, 100 million people in or near poverty (1 of 4), and an economy being propped up by creating zeroes on a computer, diluting the value under it.

Why the disconnect, or is it just me? Is that also showing us inequality, since most likely wealthier people and those with investment portfolios are the ones most raking it in from this, and this mostly shows us what they are getting?

Just wondering...

Bait and Switch Tactics

The corporate media is keeping the people "dumbed down" and getting them to vote against their best interests:

The Guardian: "Elections are not simple horse races between differing opinions, they are heavily influenced by advertising paid for by political machines that raise money from competing interest groups. The New York Daily News reported, in 2013, that a US Senate seat now costs $10.5 million to win. It is difficult for me to believe that this money is spent to endow potential voters with facts that they need in order to inform their own pre-existing preference orderings over outcomes. Money buys votes by shaping opinion."

http://www.theguardian.com/business/economics-blog/2014/oct/20/wealth-ta...