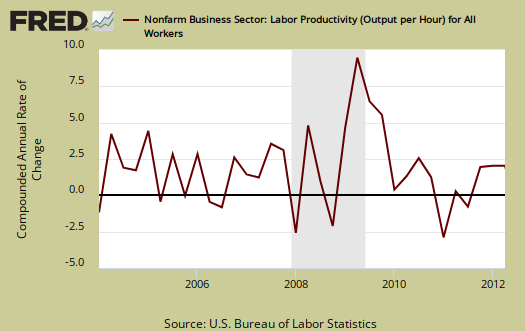

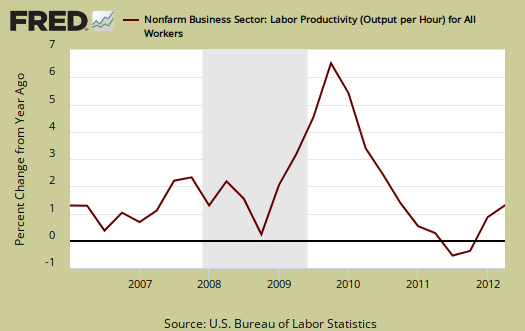

The Q2 2012 Productivity & Costs revision shows Labor productivity increased an annualized +2.2% instead of +1.6%. Output was revised to +2.4% from +2.0% and hours worked were downgraded to +0.1% instead of the originally reported +0.4%. The revisions continue to show bad news for workers, more output for less hours means worker squeeze and less hires and it's worse than we thought with these revisions. Graphed below is business, nonfarm labor productivity per quarter.

The basic equation for labor productivity is , where

is the total output of industry.

How does the BLS calculate labor productivity?

Labor productivity is calculated by dividing an index of real output by an index of the combined hours worked of all persons, including employees, proprietors, and unpaid family workers.

, or Labor, is measured in hours only. Both values are normalized to a base year, 2005. Business Output directly correlates to real GDP, minus the government, all of those nonprofits and our infamous, often illegal nannies and gardeners, and equivalent rent of owner occupied properties. The output, or

is about 75% of real GDP reported. Farms, if you can believe this, only subtract off about 1% from output totals. Labor productivity is reported annualized. The main productivity numbers above are all business, no farms, or nonfarm business, whose labor cost are over 60% of output.

From Q2 2011, or a year ago, annual productivity was also revised up to +1.2%, from +1.1%, output was revised up a 10th of a percentage point to +3.0%, and hours was revised down a 10th of a percentage point to +1.7%. Changes from a year ago show a little less worker squeeze for increased output than the annualized change from the last quarter. Output only growing 3.0% from a year ago is still anemic economic growth.

BLS defines unit labor costs as the ratio of hourly compensation, , to labor productivity,

, or

. For more formula definitions see the BLS handbook. From the report is the relationship of the ratios:

BLS defines unit labor costs as the ratio of hourly compensation to labor productivity; increases in hourly compensation tend to increase unit labor costs and increases in output per hour tend to reduce them. Real hourly compensation is equal to hourly compensation divided by the consumer price series.

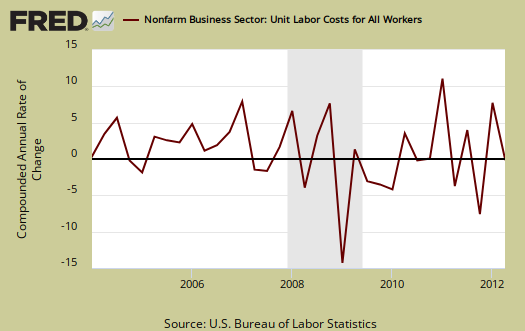

Graphed below are unit labor costs, compounded annual rate, percent change. Annualized unit labor costs still increased, but were revised down, from +1.7% to +1.5% for Q2 2012. From a year ago, Q2 2011, labor costs are are up +0.9% with the revision, implying workers are really still very cheap. Increases in unit labor costs are due to mo' money, increased compensation for the same output. Increased productivity, or output per hour, for the same $$ paid to workers should show lower unit labor costs.

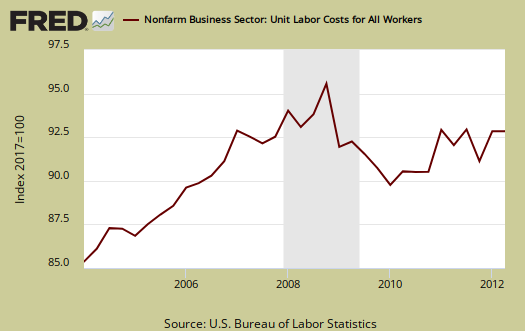

Graphed below are unit labor costs, indexed to 2005. We can see the decline starting in the Great Recession. This Q2 2012 increase in unit labor costs is only slightly better news for workers' pockets.

Real hourly compensation is wages adjusted for inflation. Real hourly compensation is equal to hourly compensation divided by the consumer price series, or .

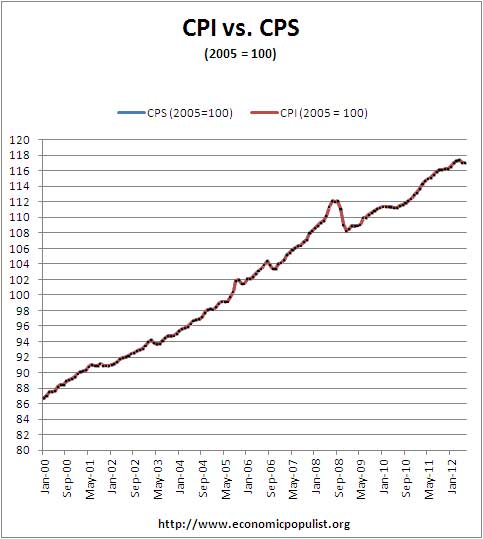

The consumer price series, , increased at a 0.75% annual rate for Q2, which is a fairly low rate of inflation. By comparison's sake CPI also increased 0.75% annualized for Q2. Now here we have a bone to pick. If one derives the CPS utilized for this report, it is to six significant digits instead of the published four for the CPI-RS-U series, which supposedly is what the consumer price series is.

The change for recent quarters is based on the Consumer Price Index for all urban consumers (CPI-U). The trend from 1978-2011 is based on the Consumer Price Index research series (CPI-U-RS)

Guess what happens? Instead of an annualized 0.84% annualized increase in inflation, utilizing CPI-U-RS, we get a 0.75% increase. This has the effect of reducing the reported decline in real hourly compensation, simply by a lack of the correct number of significant digits for percentage resolution. That said, the last two quarters reported does use CPI-U and not CPI-RS-U. We've actually managed to piss off the BLS productivity division over this issue, but it clearly matters when one is reporting real compensation. On the other hand, if one takes CPI-U, the numbers for not just the last two quarter, but all quarters, it more closely matches the actual consumer price series used in the productivity report than the published one decimal place CPI-U-RS. Bottom line, when using price deflators, inflation adjusters, accuracy, significant digits matters.

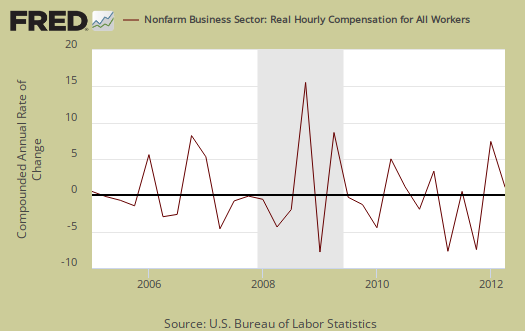

In terms of real dollars, adjusted for inflation, we have a revised annualized +2.9% increase in real hourly compensation for Q2 2012, non-farm businesses, from the originally reported +2.6% real hourly compensation increase. In comparison to Q2 2011, real hourly compensation was revised to +0.3% from the originally reported no change. This is a little better than previous reports, but still shows wages are barely keeping up with inflation overall. Below are quarterly changes to hourly compensation, adjusted for consumer prices. You can see the rise and fall with deflation and inflation.

The BLS productivity statisticians use CPI-U-RS up to Q1 2012 and then for the current quarter, re-adjust CPI-U, but indexed to 2005. First, the CPI-U-RS is a research measure. This consumer price series seems to flatten inflation, thus make the decline in U.S. wages less, although when normalized to a base year of 2005 the two series are the same for all practical purposes for over a decade. The implicit price deflator, applied to nonfarm business output (productivity), is from the BEA. CPS and the price deflator are all to remove inflation effects from the productivity statistics.

The BLS also reports separately on manufacturing productivity, but uses a different calculation method than the one for business productivity. So, don't think ya can subtract the below and get services productivity, the two ain't the same.

Manufacturing is sales, removing duplicates, adjusting for prices and output () is correlated to shipments and the industrial production. indexes. Hours are hours like above. Page 4 of the report has the manufacturing productivity measurement nitty gritty.

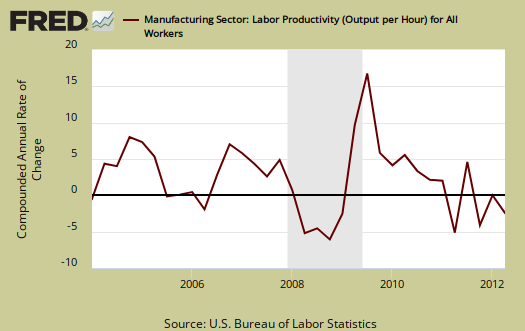

Manufacturing productivity was revised down a 10th of a percentage point to +0.1%, annualized, for Q2 2012. Manufacturing output was revised to +1.5% from +1.7% while hours worked increased 1.4% and wasn't revised. Since Q2 2011, productivity remained the same, an increase of +2.9%, but output was revised to +5.5% from +5.6% and hours remained the same, a +2.6% increase.

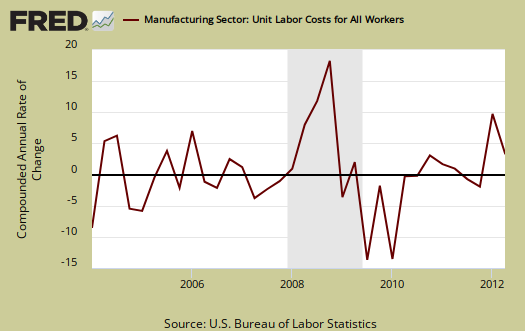

Manufacturing unit labor costs were revised to +0.8% from an originally reported 0.3% for Q2 2012. From a year ago, manufacturing unit labor costs are down -2.4%, revised from -2.9%.

Q2 2012 real compensation (wages) in manufacturing was revised to +0.2% from -0.3%, even though compensation per hour, not adjusted for inflation was revised to +0.9% from +0.5%.

Since Q2 2011, real hourly compensation has dropped to a revised -1.4% from the original -1.9% reported, with compensation per hour, not adjusted for prices, increasing +0.4%, also revised from -0.1%.

Manufacturing wages are beyond not keeping up with inflation, the numbers look like plain labor arbitrage. Below is real hourly compensation for all manufacturing.

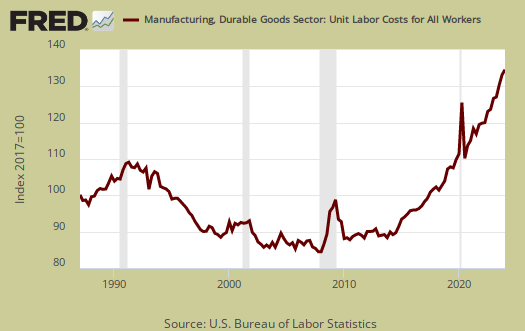

For Q2 2012, durable good manufacturing productivity numbers were significantly revised. Productivity grew at +3.7% instead of the reported 4.3%, output was revised down, from +6.2% to +5.4% and hours were revised to +1.6% from the originally reported +1.9% increase. Yet none of this translated to workers. Durable goods labor unit costs dropped -3.2% from an originally reported -4.9% and real compensation declined -0.4%, revised from -1.5% Actual hourly wages were revised from a reported -0.8% to +0.4%. All of these figures are the change from Q1 2012 and are presented as annualized rates. Below is the durable goods manufacturing real hourly compensation index. Note it's decline.

Unit labor costs in durable goods shows the decline of the American worker for they are returning to their record lows. Unit labor costs show real output per hour. Durable goods workers are producing more and more and U.S. workers are getting less reward.

Nondurable manufacturing was significantly revised with productivity being -3.8%, output was -2.8% and hour worked up +1.0%. Unit labor costs increased +6.1%, hourly compensation was up +2.0% and real hourly compensation increased +1.3%. It looks like we have some positive movement on wages for those workers in nondurable goods manufacturing, although from a year ago, real hourly compensation is still down -1.4%.

What you see these days in productivity is not what it appears. The press will claim increased productivity is a great thing, and maybe that's true for corporate profits, but it's clearly not translating into wages and jobs for workers.

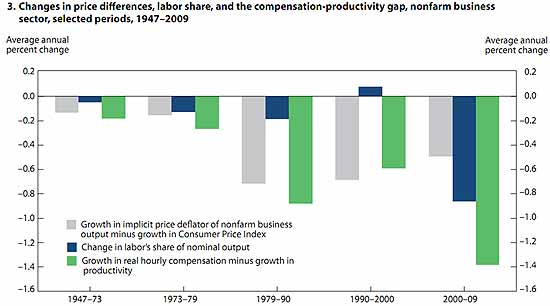

While leads me to this paper from the Monthly Labor Review, The compensation-productivity gap: a visual essay. Now these are the people who maintain the BLS productivity statistics. In the report, they go over their methods, calculations, which can make a huge difference in results. Bottom line they show since the 1970's, workers are getting less and less of the labor share or payout, less of a slice from the American pie called increased economic output. What they found was most of the productivity vs. how much you get in your pocket to spend gap before year 2000 could be attributed to a couple of different measures for inflation. After 2000, the gap is because workers are getting screwed.

From the paper:

Labor share is a measure of how much of the economic pie goes to all workers. When labor share is constant or rising, workers benefit from economic growth. When labor share falls, the compensation–productivity gap widens. Concurrently, nonlabor costs—which include intermediate inputs into production and returns to investments, or profits—represent a greater share of output.

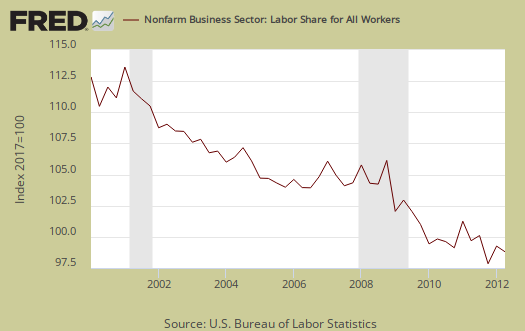

Below is labor market share for nonfarm business which shows workers overall are getting less and less of the productivity pie.

Their paper is loaded with graphs, but the above was reprinted for it shows clearly, since 2000, American workers are simply getting shafted while those making the profits are taking it to the bank.

Productivity and Costs was significantly revised. It's tied to GDP, which is revised heavily, with benchmarks, as well as other inputs which are revised. Here is the original Q2 Productivity & Costs overview, although graphs are updated, text is not. Then, here is last quarter's overview, text only unrevised.

Recent comments