The cost of mass deportations in states like Minnesota—and what federal tax dollars could be funding instead

This week, EPI will release a new tool showing the cost of mass deportations to taxpayers in every U.S. city, county, and state. For the first time, the actual economic tradeoffs imposed on all taxpayers will be shown in one place. Below, we preview the data for Minnesota, a prominent target of the Trump administration’s immigration enforcement crackdown earlier this year.

At a time when families across the country are struggling to afford housing, health care, and education, the Trump administration and its allies in Congress have been cutting support for basic needs and diverting huge sums of money to deportations.

In Minnesota, $4.4 billion in federal taxpayer dollars is being spent on detaining immigrants—many of whom are in the country lawfully—and even some U.S. citizens. That means, on average, every household in the state is paying roughly $2,000 to track down, intimidate, detain, or deport people.

If that money were spent instead on programs proven to improve the lives of working families—education, health care, living wages—it could improve Minnesota communities dramatically. Here are a few different ways the money could be spent over the remaining 2.5 years of the Trump administration:

- Schools across the state are being forced to cut staff and increase class size. With the money being spent on mass deportations, the state could hire 14,000 more full-time school teachers. This would mean, for example:

- 1,100 more teachers in Minneapolis

- 340 more teachers in Minnetonka

- 215 more teachers in Bloomington

- 140 more teachers in Duluth

- With the cuts to the Affordable Care Act, over 140,000 people in Minnesota are projected to lose their health insurance. Due to cuts in Medicaid funding, hospitals are at risk of closing down in Austin, Staples, Mahnomen, Baudette, Little Falls, Hibbing, and Minneapolis. With the money being spent on deportations, we could keep 129,000 people on health insurance, which would also help keep hospitals open.

- Over 400,000 Minnesotans rely on food stamps, primarily working families with children and elderly people on fixed incomes. But because of cuts in the 2025 Republican tax and spending megabill (the OBBBA), 45,000 people across the state are at risk of being cut off. With the money being spent on deportations, Minnesota could protect food stamps for all hungry families in the state.

- Last year, over 600 Veterans Administration positions were cut in Minnesota. With the funds being diverted to deportations, we could reverse all these cuts and guarantee Minnesota veterans the care they deserve.

- Or, instead of restoring any of these services, every household in Minnesota could be given a $2,000 tax refund.

EPI and others have documented the economic harms of a draconian immigration policy and enforcement on immigrants and their families, as well as U.S.-born workers and the economy as a whole. Any of the alternatives listed above would be a better use of taxpayer dollars for improving the welfare of everyday Minnesotans. It is critical that we take into account the missed opportunities of funding a mass deportation regime, including the badly needed services being ignored or cut off to keep this policy funded and to keep immigrants living in fear.

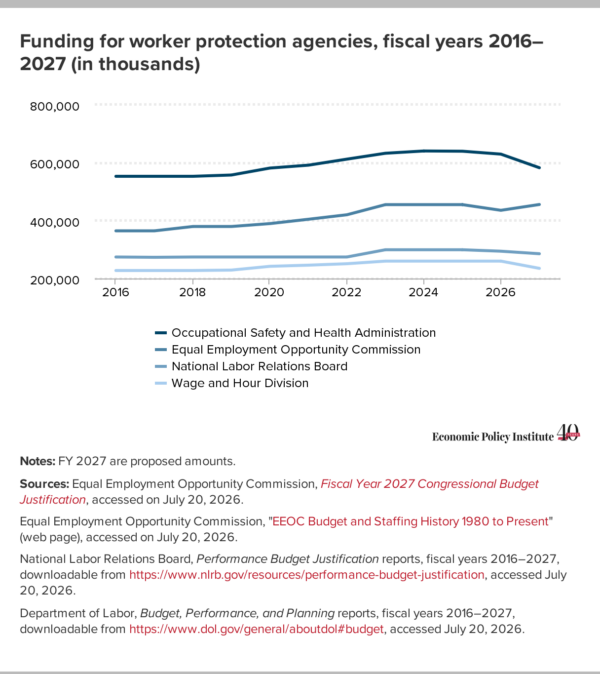

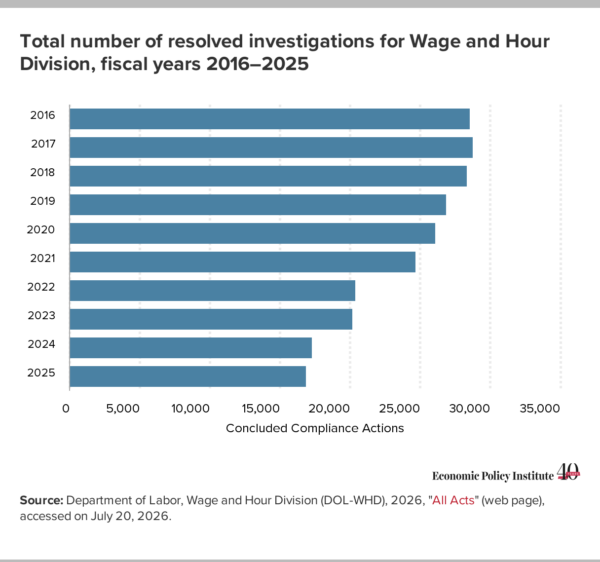

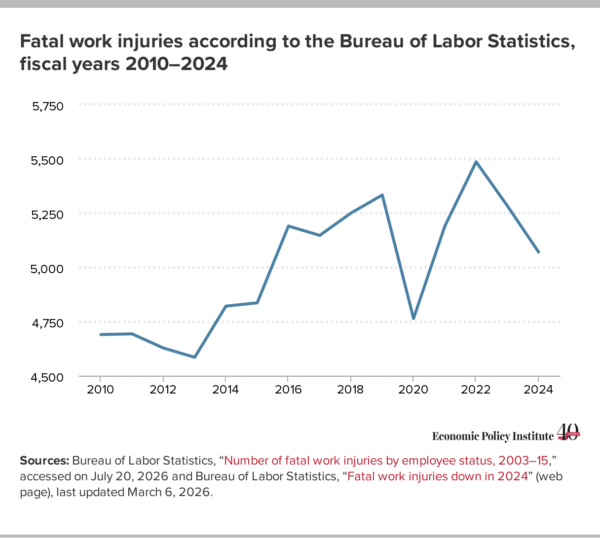

The consequences of underfunding worker protection agencies

The consequences of underfunding worker protection agencies

Recent comments