Michael Collins

I wrote the story below in response to an outrageous trick Congress just tried to play on the public. As many of you know, the Senate passed 0/congress/bills/111/hr3808/text">HR 3808 The Interstate Recognition of Notarizations Act of 2010 unanimously on September 27. The bill was a carefully crafted, stealth "silver bullet" for the big banks to deal with their increasing legal problems with foreclosures. President Obama exercised a "pocket veto," which means he let it die after Congress adjourned. (Image)

While my story focused on the process and contempt shown to citizens by Congress in that process, I became aware of a much broader issue. We may well be on the verge of a real estate value meltdown as a result of very bad behavior, illegal in many cases, by the big banks combined with the legitimate push back of mortgage holders.

If banks can't foreclose and people can do a strategic default and walk away (0r live free in their residence), what will happen to real estate values?

The larger question emerged in reviewing bank bad behavior.

If there are fundamental flaws in many, maybe most mortgage, flaws of a serious legal nature, what if a strategic default movement spreads beyond just those facing foreclosure? That's where Armageddon comes in

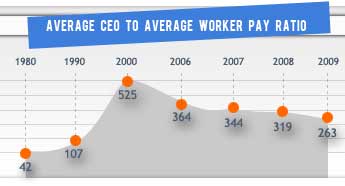

What ever happened to executive compensation reform? Like all great ideas, it died in Congressional committee, or watered down to meaningless if passed.

What ever happened to executive compensation reform? Like all great ideas, it died in Congressional committee, or watered down to meaningless if passed.

It's Friday Night! Party Time! Time to relax, put your feet up on the couch, lay back, and watch some detailed videos on economic policy!

It's Friday Night! Party Time! Time to relax, put your feet up on the couch, lay back, and watch some detailed videos on economic policy!

Recent comments