Wall Street was all aghast that their quantitative easing was about to disappear. The FOMC decided to taper in January and now stocks soar. Why? Because the taper is minimal and the FOMC announced the federal funds rate will remain an effective zero for much longer than previously estimated.

Beginning in January, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $35 billion per month rather than $40 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $40 billion per month rather than $45 billion per month.

This is only $10 billion less in additional purchases than previously. This means quantitative easing is still continuing, just as a slightly smaller size than previously. $75 billion is additional purchases so the Fed did not go cold turkey on additional purchases of mortgage backed securities and U.S. Treasuries. Additionally the Fed did not announce a schedule for tapering, additional reductions are dependent on economic conditions:

If incoming information broadly supports the Committee's expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings. However, asset purchases are not on a preset course, and the Committee's decisions about their pace will remain contingent on the Committee's outlook for the labor market and inflation as well as its assessment of the likely efficacy and costs of such purchases.

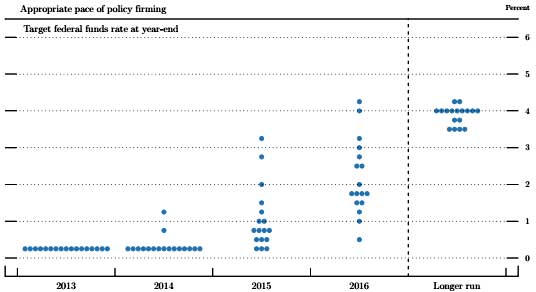

The FOMC also released a timing chart on when they expect the federal funds rate to rise and what value. The dots in the chart are individual FOMC members and to the right is the expected federal funds rate. Most of the members, 12, expect to raise the federal funds rate in 2015.

The FOMC also announced an unemployment rate figure, 6.5%, before they consider raise the Federal Funds rate from it's effective zero percent. They also set a maximum annual inflation rate of 2.5% These are threshold figures, not hard, written in stone rates. There are many other economic metrics which can be horrific news, yet result in both low inflation and a low official unemployment rate. Specifically Bernanke mentioned the labor participation rate being artificially low and the lack of job hires, as seen in the piss poor JOLTS statistics.. This gives a much wider timeline before the Fed would raise interest rates. From Bernanke's opening statement at the press conference:

the Committee now anticipates it will likely be appropriate to maintain the current federal funds rate target well past the time that the unemployment rate declines to below 6-1/2 percent, especially if projected inflation continues to run below its 2 percent goal. In part this expectation reflects our assessment, based on a comprehensive set of indicators, that there will still be a substantial amount of slack in the labor market when the unemployment rate falls to 6-1/2 percent. This continuing job market slack imposes heavy costs on the unemployed and the underemployed and their families and reduces our nation’s productive capacity, warranting our ongoing highly accommodative policy. But, as the last phrase of the enhanced guidance underscores, the prospects for inflation provide another reason to keep policy accommodative. The Committee is determined to avoid inflation that is too low as well as inflation that is too high, and it anticipates keeping rates low at least until it sees inflation clearly moving back toward its 2 percent objective.

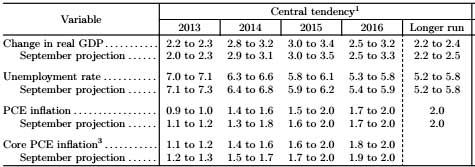

Below are the new FOMC economic projections upon which they base the above decisions on. While we see a 2014 6.5% unemployment rate projection, the above expected time line to rate interest rates in 2015 shows the official unemployment rate is not the only metric the FOMC is looking at to raise interest rates.

Bernanke also gave probably his last press conference. Under employment and low inflation are one of the reasons the Fed is justifying continuing quantitative easing in spite of the slight reduction in asset purchases by $10 billion to a still massive $75 billion a month. The FOMC recognized many people are not part of the labor force who could be as well as the large number of long-term unemployed.

The recovery clearly remains far from complete, with unemployment still elevated and with both underemployment and long-term unemployment still major concerns. We have also seen ongoing declines in labor force participation, which likely reflect not only longer-term influences such as the aging of the population but also discouragement on the part of potential workers.

Bernanke also emphasized data dependent analysis for the FOMC to take action. Bernanke mentioned tight fiscal policy causing a drag on the economy over and over. Yet Bernanke punted on much Q&A that could be headliners in the press. It seems Bernanke is setting up a smooth transition for Janet Yellen to head the Fed, as she was all in on the FOMC decision and new Fed policy.

Generally speaking the Fed is clearly very stimulative and using the federal funds rate as an effective methadone program to get Wall Street off of their quantitative easing crack cocaine seems to be acceptable to markets.

Recent comments