We told ya so, yet people don't listen. The Federal Reserve FOMC meeting minutes were released and showed no quantitative easing for you.

Here is the money shot from the FOMC minutes:

A couple of members indicated that the initiation of additional stimulus could become necessary if the economy lost momentum or if inflation seemed likely to remain below its mandate-consistent rate of 2 percent over the medium run.

The FOMC has 10 voting members. The news is clear, those in favor or more quantitative easing are now 8 to 2 and if and only if the economy goes further into the tank.

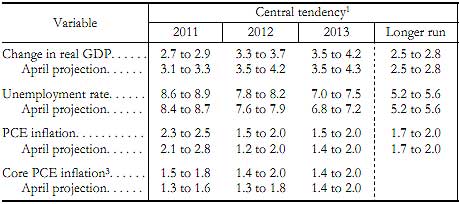

Nevertheless, the staff continued to forecast that real GDP growth would pick up only gradually in 2012 and 2013, supported by accommodative monetary policy, easing credit conditions, and improvements in consumer and business sentiment

We're sure some will hold out hope against hope that more quantitative easing will happen. After all there are two members of the FOMC leaving the door open on more quantitative easing if the unemployment situation gets worse. That said, the next time you see some major investment group claiming QE3 is sure to arrive, check their interests and why that group is making such a claim. Alternatively just read us, we sure knew QE3 was not gonna happen.

Welcome to the weekly roundup of great articles, facts and figures. These are the weekly finds that made our eyes pop.

Welcome to the weekly roundup of great articles, facts and figures. These are the weekly finds that made our eyes pop.

Federal Reserve Chair Ben Bernanke gave his long awaited

Federal Reserve Chair Ben Bernanke gave his long awaited  Originally published by

Originally published by

Recent comments