Bloomberg News has researched a bombshell story, the Federal Reserve gave $1.2 trillion in secret loans to banks during the financial crisis, from August 2007 until April 2010. This is in addition to the TARP bail outs which was publicly known.

The $1.2 trillion peak on Dec. 5, 2008 -- the combined outstanding balance under the seven programs tallied by Bloomberg -- was almost three times the size of the U.S. federal budget deficit that year and more than the total earnings of all federally insured banks in the U.S. for the decade through 2010, according to data compiled by Bloomberg.

The top three banks at peaking borrowing are: Morgan Stanley, $107.3 billion, Citigroup took $99.5 billion, Bank of America $91.4 billion, or a total of $298.2 billion. Gets worse, foreign banks amounted to half the loans.

Half of the Fed’s top 30 borrowers, measured by peak balances, were European firms. They included Edinburgh-based Royal Bank of Scotland Plc, which took $84.5 billion, the most of any non-U.S. lender, and Zurich-based UBS AG (UBSN), which got $77.2 billion. Germany’s Hypo Real Estate Holding AG borrowed $28.7 billion, an average of $21 million for each of its 1,366 employees.

Welcome to the weekly roundup of great articles, facts and figures. These are the weekly finds that made our eyes pop.

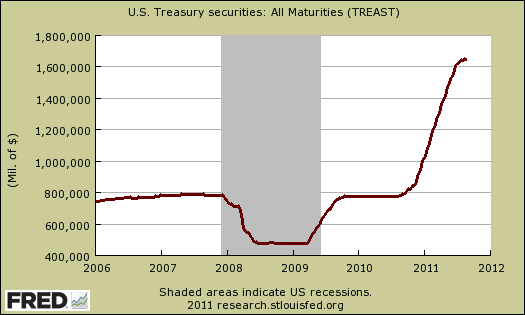

Welcome to the weekly roundup of great articles, facts and figures. These are the weekly finds that made our eyes pop. The Federal reserve announced Operation Twist, an action from 1961 where the Fed swaps out treasuries of short maturity lengths, for longer ones, all in an attempt to flatten, or twist the

The Federal reserve announced Operation Twist, an action from 1961 where the Fed swaps out treasuries of short maturity lengths, for longer ones, all in an attempt to flatten, or twist the

Federal Reserve Chair Ben Bernanke gave his long awaited

Federal Reserve Chair Ben Bernanke gave his long awaited  Is Gold money? Apparently not according to Ben. While technically correct, all of those gold bugs hording their physical gold for the impending Global Economic Armageddon, round 3, are jumping at the ready.

Is Gold money? Apparently not according to Ben. While technically correct, all of those gold bugs hording their physical gold for the impending Global Economic Armageddon, round 3, are jumping at the ready.

Recent comments