The Obama administration is pre-announcing the regulatory reforms announcements (see their outline below), so much so one might miss what is coming out of Congressional hearings on the topic.

I believe that only ostriches can now deny the need for establishing a federal insurance resource center and a basic federal insurance regulatory structure.

Geither's response? Let's ignore the entire insurance industry. What's in a name? (AIG)

(Reuters) - U.S. credit card defaults rose to record highs in May, with a steep deterioration of Bank of America Corp's (BAC - News) lending portfolio, in another sign that consumers remain under severe stress.

...

Bank of America Corp -- the largest U.S. bank -- said its default rate, those loans the company does not expect to be paid back, soared to 12.50 percent in May from 10.47 percent in April.

The bank is paying the price of expanding rapidly in recent years and of holding one of the highest concentrations of subprime borrowers among the top card issuers, analysts said.

Contained within the Q&A is this fantastic question by Representative Alan Grayson (D-FL-8th): How do we hold these executives accountable when they have destroyed their own banks?

April's LEI were the most strongly positive indicators in 2 years, and the first batch of readings for May were similarly positive. By June 1, we already knew that, by weight over 50% of the indicators would be positive. Real money supply was still strong as the Fed continues to re-liquify (or re-solvenc-fy) the banking system. The yield curve was even more strongly positive than before, due to the backup in long term rates while short term rates are still essentially 0%. Stock prices (over the last 90 days) also strongly rallied. Consumer expectations about the future is rising sharply. Average initial claims for unemployment insurance were basically flat for the month. By weight, that's 52% positive, and 3% neutral.

So May's data started out looking very positive. As we shall see, the suckerpunch was saved for the end.

The shear amount of information uncovered is staggering. Hopefully it will keep your interest.

Let me warm up here with a couple of interesting quotes.

"Gold was not selected arbitrarily by governments to be the monetary standard. Gold had developed for many centuries on the free market as the best money; as the commodity providing the most stable and desirable monetary medium." Murray N. Rothbard

Why Gold and Why Now?

"If you don't trust gold, do you trust the logic of taking a beautiful pine tree, worth about $4,000 - $5,000, cutting it up, turning it into pulp and then paper, putting some ink on it and then calling it one billion dollars?" Kenneth J. Gerbino

Ever wonder why banks and governments like a paper currency system? Why they fully embraced the Keynesian theory of deficit spending?

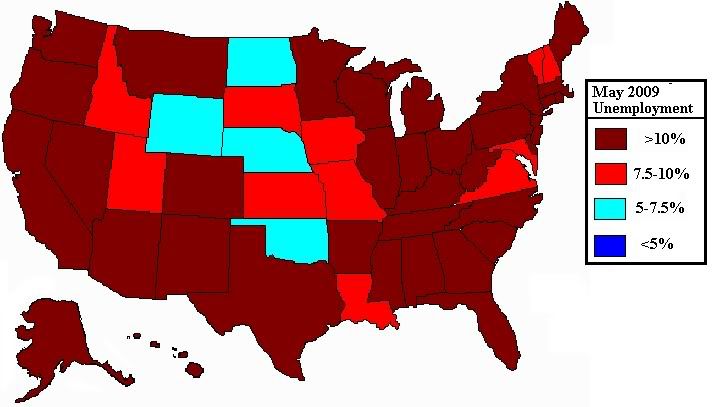

Unemployment is a malleable thing. The official unemployment rate released by the BLS (Bureau of Labor Statistics) excludes those individuals who have not looked for work in the last month and those forced to work part time for economic reasons. In short the official rate (U-3) tends to vastly understate the unemployment rate, creating the impression that things are better than they actually are. For many, years the BLS has released what it calls alternative measures of labor underutilization that provide details of the percentage of workers who would like to work (but haven't actively sought it in the last month) and those working part time for economic reasons at the national level.

However, until very recently, the BLS has not released this data at the state level. That has changed. When we look at this broader unemployment rate at the state level, the picture isn't pretty.

This isn't a conspiracy. The problem is small sample size. The BLS uses surveys with a very large number of participants to drive down the marign of error. So the number that we get at the national level is basically the same that you'd get if you called everyone in the US. But, when you go to the states, the number of participants shrink, and when you include a large number of categories, the margin of error goes up. It's still quite low, just not the gold standard that the BLS has set for national unemployment figures.

For those of us here, I imagine that this will come as no great surprise:

At a time when it's more competitive than ever to get into the University of Illinois, some students with subpar academic records are being admitted after interference from state lawmakers and university trustees, a Tribune investigation has revealed.

Hundreds of applicants received special consideration in the last five years, according to documents obtained by the Tribune under the state's Freedom of Information Act. The records chronicle a shadow admissions system in which some students won spots at the state's most prestigious public university over the protests of admissions officers, while others had their rejections reversed during an unadvertised appeal process.

Representative George Miller is waging a lonely war against powerful enemies. He's trying to reform the 401(k) system, a system that most on Wall Street don't want reformed.

The key to Miller's plan is to force 401(k) providers to disclose their fees in plain English. If you don't think this is important, consider that those fees can eat up 75% of your potential retirement savings.

If you look at the system, basically what you have is working families making the conscious decision every month to try to save some money for retirement. Then along comes people managing those funds for them and they start dipping into those funds for fees that are really not in the best interest of those savers. So, you have elite financial managers getting rich off the back of middle-class working people. The last thing they really want is transparency.

"The 401(k) system today in the United States has been an acknowledged failure."

- Alicia Munnell, director of the Center for Retirement Research at Boston College's Carroll School of Management.

It's Friday Night! Party Time! Time to relax, put your feet up on the couch, lay back, and watch some detailed videos on economic policy!

It's Friday Night! Party Time! Time to relax, put your feet up on the couch, lay back, and watch some detailed videos on economic policy!

Recent comments