Despite large bonuses for some, average real disposable income per capita in February remained lower than in March 2007 as real spending stagnates with meager savings.

Today’s BEA report on personal income and spending in February provides important context for anticipating the possible depth and length of the current recession.

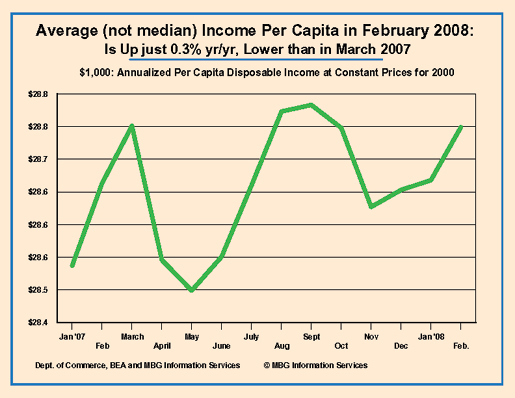

BEA reports that even with large end-of-year bonuses for a few (mostly in the debt industry that is seeking taxpayer bailouts for their looted companies,) the average real disposable income per capita rose only 0.3% in February, up only 0.3% yr/yr and still below levels reached in March 2007. All of the gain in worker compensation in February (and more than all in January) is accounted for by the large bonuses. Proprietor income fell sharply in February and is down sharply yr/yr.

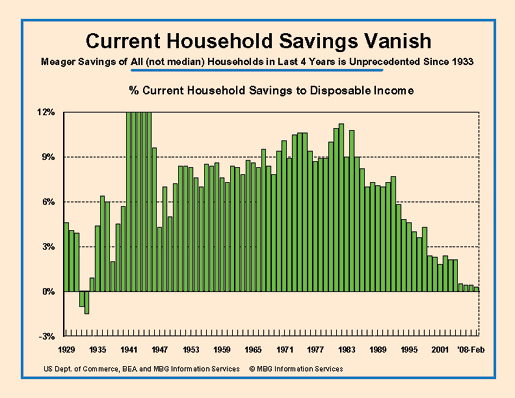

Real spending was unchanged in February (down slightly on a per-capita basis) as households reacted to the first 3 consecutive months on record (and likely since 1933) in November-to-January that after-tax incomes failed to keep up with spending. Because of the huge bonuses for some in February, total after-tax income for all Americans was 0.3% more than total spending in February. These bonuses account for more than half the total US household savings in February. This is now the fourth consecutive year when total (not median) after-tax incomes exceed total household spending by less than 0.5%; by far the worst financial condition since 1933.

The after-tax incomes for most Americans are falling further behind price increases, they have no current savings (even including monthly retirement contributions and mortgage payments,) even as they face record debts and debt-service obligations and their homes are losing value. And media pundits are surprised that consumer expectations for the future are plummeting!? The small tax rebate check that most will receive this summer can’t come soon enough but will have little, and very short-lived effect.

The current recession could easily be comparable to the recession of 1982 when the US economy was last at a crossroads and chose the cotton candy voodoo of unsustainable debt-dependence over the more complicated but stable path to prosperity through smart industrial and trade policies. Yesterday’s speech by Senator Obama resurrecting the essential government role of regulating markets to assure broad and stable prosperity was a hopeful moment. The economy needs much more and quickly; this economic crisis will not wait.

Recent comments