The long awaited day is here. In the spirit of QE2, aka quantitative easing part II, the Federal Reserve has announced $600 billion in U.S. Treasury purchases:

The Committee intends to purchase a further $600 billion of longer-term Treasury securities by the end of the second quarter of 2011, a pace of about $75 billion per month. The Committee will regularly review the pace of its securities purchases and the overall size of the asset-purchase program in light of incoming information and will adjust the program as needed to best foster maximum employment and price stability.

Also, the thing every one knows, they will keep the Federal Funds Rate at effective zero and sure doesn't look like they will raise it anytime soon:

The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels for the federal funds rate for an extended period.

Kansas City Fed President Thomas M. Hoenig voted against this.

But wait! There's more. From the New York Federal Reserve press release is appears they are actually buying up about $900 billion U.S. Treasuries de facto.

The Federal Reserve Beige Book report is out and they acknowledge overall the economy is decelerating. We're in a slow down, minimum. folks. It's official.

Reports from the twelve Federal Reserve Districts suggested continued growth in national economic activity during the reporting period of mid-July through the end of August, but with widespread signs of a deceleration compared with preceding periods.

They also acknowledge one element we have graphed here, raw capacity in manufacturing, is down.

Reports on capacity utilization were mixed. Manufacturers of high-tech products have been operating near maximum capacity of late, although this partly reflects a substantial decline in industry-wide capacity over the past three years, as noted by Dallas. More generally, the majority of Cleveland's manufacturing contacts reported that capacity utilization remained below pre-recession levels. Capital spending plans for manufacturers and firms in other industries generally indicate little change or modest increases in coming months, based on reports from the Boston, Philadelphia, Cleveland, Chicago, Kansas City, and San Francisco Districts.

They also note the increased use of temp jobs and contract labor is repressing permanent employment.

The U.K. Telegraph is reporting some horrifying news that behind closed doors the Federal Reserve is considering purchasing more toxic assets. A lot more. To bring the total from $2.4 trillion to $5 trillion dollars.

The Federal Reserve leaves the federal funds rate unchanged. Kansas City Federal Reserve President Thomas M. Hoenig was the lone dissenting voice. Below is the press release along with commentary on general economic conditions.

Information received since the Federal Open Market Committee met in April suggests that the economic recovery is proceeding and that the labor market is improving gradually. Household spending is increasing but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software has risen significantly; however, investment in nonresidential structures continues to be weak and employers remain reluctant to add to payrolls. Housing starts remain at a depressed level. Financial conditions have become less supportive of economic growth on balance, largely reflecting developments abroad. Bank lending has continued to contract in recent months. Nonetheless, the Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability, although the pace of economic recovery is likely to be moderate for a time.

Prices of energy and other commodities have declined somewhat in recent months, and underlying inflation has trended lower. With substantial resource slack continuing to restrain cost pressures and longer-term inflation expectations stable, inflation is likely to be subdued for some time.

We can’t wait until unemployment is where we’d like it to be” or inflation gets “out of control” to tighten credit

The above is a quote from Federal Reserve Chair Ben Bernanke.

Gets worse, Bernanke believes the economy will not dip into another recession, yet of course, unemployment will remain at high levels.

While the Fed will raise interest rates from a record low before the economy returns to “full employment,” Bernanke said officials don’t know when that process will start. The banking system isn’t fully healthy and lenders are “cautious” in providing credit, he said.

“The unemployment rate is still going to be high for a while, and that means that a lot of people are going to be under financial stress,” Bernanke said at the event, part of a dinner hosted by the Woodrow Wilson International Center for Scholars.

Bernanke’s stance is consistent with that of several Fed colleagues. Atlanta Fed President Dennis Lockhart said June 3 that the central bank may need to raise rates even with “unacceptable levels of unemployment,” while Eric Rosengren of the Boston Fed said last month it wouldn’t be “appropriate” to have rates close to zero with the economy at full employment.

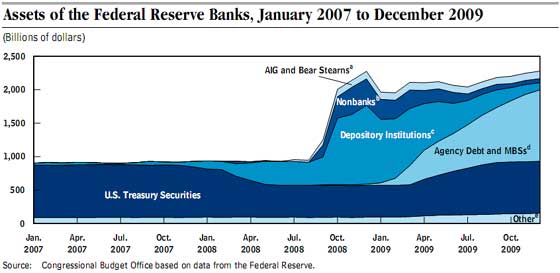

The CBO has a new report on those nasty, toxic mortgage backed securities the Federal Reserve bought, along with a host of other crud from the financial meltdown.

A new amendment, which Senator Dodd has signed onto has been introduced by Senator Bernie Sanders. It appears we have a bait -n- switch or compromise, i.e. back room deal on auditing the Federal Reserve.

This should be a no-brainer for Economic Populist readers...

(Reuters) - It's a mystery that has puzzled even Federal Reserve Chairman Ben Bernanke: if the U.S. economy is growing rapidly, why isn't it creating jobs?

Perhaps we should send Bernanke the link to the site?

For whatever reason, the administration has not taken full advantage of its chance to shape monetary policy during the downturn. The number of open positions is a large fraction of the Federal Reserve Board, and it skews the balance of power on the Federal Open Market Committee (where monetary policy is decided) toward the regional banks. Many of the regional bank presidents are inflation hawks, more so than the Governors, so this may have affected the Fed’s policy choices.

Recent comments