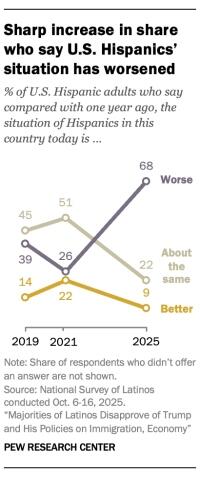

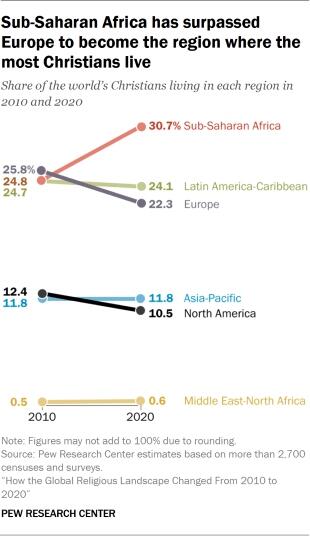

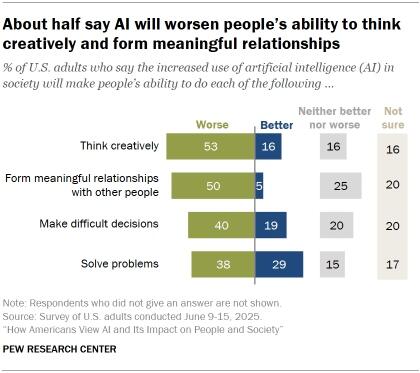

Satyajit Das: AI – Artificial Intelligence or Absolute Insanity?

Authored by Satyajit Das via NakedCapitalism.com,

AI is tracing the familiar, weary boom and bust trajectory identified in 1837 by Lord Overstone of quiescence, improvement, confidence, prosperity, excitement, overtrading, convulsion, pressure, stagnation, and distress.

There are three primary concerns.

First, there are doubts about the technology.

Building on earlier technologies such as neural networks, rule-based expert systems, big data, pattern recognition and machine learning algorithms, GenAI (generative AI), the newest iteration, uses LLMs (large learning models) trained on massive data sets to create text and imagery. The holy grail is the ‘singularity’, a hypothetical point where machines surpass human intelligence. It would, in Silicon Valley speak, lead to ‘the merge’, when humans and machines come together potentially transforming creativity and technology.

LLMs require enormous quantities of data. Existing firms in online search, sales platforms and social media platforms can exploit their own data troves. This is frequently supplemented by aggressive and unauthorised scraping of online data, sometimes confidential, leading to litigation around access, compensation and privacy. In practice, most AI models must rely on incomplete data which is difficult to clean to ensure accuracy.

Despite massive scaling up of computing power, GenAI consistently fails in relatively simple factual tasks due to errors, biases and misinformation in datasets used. AI models are adept at interpolating answers between things within the data set but poor at extrapolation. Like any rote-learner, they struggle with novel problems. Their ability to act autonomously interacting within dynamic environments remains questionable. Cognitive scientists argue that simply scaling up LLMs based on sophisticated pattern-matching built to autocomplete rather than proper and robust world models will disappoint. Claimed progress is difficult to measure as benchmarks are vague and inconclusive.

Cheerleaders miss that LLMs do not reason but are probabilistic prediction engines. A system which trawls existing data, even assuming that is correct, cannot create anything new. Once existing data sources are devoured, scaling produces diminishing returns. Rather than fully generalisable intelligence, generative models are regurgitation engines struggling with truth, hallucinations and reasoning.

AI models can take over certain labour-intensive tasks like data driven research, journalism and writing, travel planning, computer coding, certain medical diagnostics, testing and routine administrative tasks like handling standard customer service queries. Its loftier aims may prove elusive. Predictions of medical breakthroughs have disappointed although pre- OpenAI machine learning models, pattern recognition engines and classifiers, used for years, continue to be useful.

For the moment, GenAI, an ill-defined marketing rather than technical term, remains a costly parlour trick for some low-level applications, making memes and allowing scammers to deceive and defraud – the “unfathomable in pursuit of the indefinable”.

Second, financial returns may prove elusive.

Capital expenditure on AI is expected to total up to $5-7 trillion by 2030. AI startup valuations based on the latest round of funding were $2.30 trillion, up from $1.69 trillion in 2024, and up from $469 billion in 2020. But AI’s capacity to generate cash and returns on the investment remains questionable.

Revenues would have to grow over 20 times from the current $15-20 billion per annum to just cover current annual investment in land, building, rapidly depreciating chips and power and water operating expenses. Revenues totalling more than $1 trillion may be required to earn an adequate return. Microsoft’s Windows and Office, among the world’s most used software, generates less than $100 billion in commercial and consumer revenue. Around 5 percent of its 800 million users currently pay to use ChatGPT. Microsoft’s CEO drew the ire of true believers when he argued that AI had yet to produce a profitable killer application to match the impact of email or Excel.

The hope is AI will be paid for from higher productivity and corporate profits. But 95 percent of corporate GenAI pilot projects failed to raise revenue growth. After cutting hundreds of jobs and replacing them with AI, many firm were subsequently forced to reemploy staff when the technology proved deficient. Corporate interest is already showing sign of plateauing.

Monetisation of AI faces other uncertainties. Several Chinese firms, such as DeepSeek, Moonshot as well as Bytedance and Alibaba, have developed cheaper models which cast doubts about the capital investment intensive approach of Western firms. China’s favoured open-source design would also undermine the revenues of firms which have invested heavily in proprietary technology. Required electricity and water supplies may prove to be constraints.

In the meantime, AI firms remain a cash burning furnace. In the first half of 2025, OpenAI, owner of ChatGPT, generated $4.3 billion in revenue but spent $2 billion on sales and marketing and nearly $2.5 billion on stock-based equity compensation, posting an operating loss of $7.8 billion.

Third, there are financial circularities seen during the dot com boom.

CoreWeave, an equipment rental business trying to cash in the AI boom, purchases graphics processers in-demand for AI applications and rents them to users. Nvidia is an investor in the company, and the bulk of revenues is from a few customers. There is concern around CoreWeave’s accounting practices, especially the rate of depreciation of the chips, and its significant borrowings.

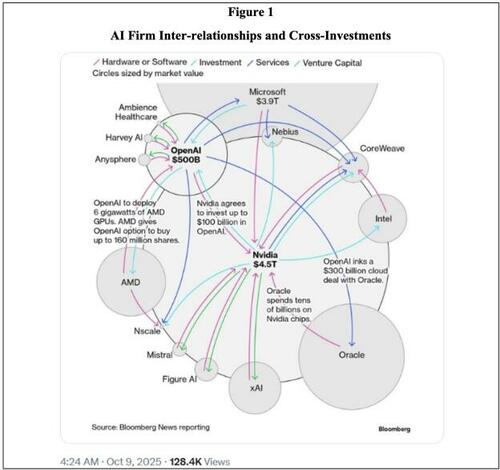

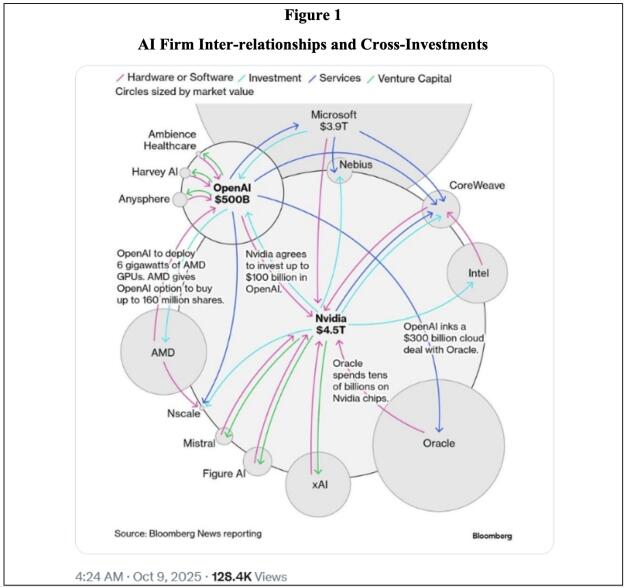

In 2025, Nvidia, the backbone of the boom, agreed to invest $100 billion in OpenAI which in turn bought a similar dollar value of GPUs from it. Open AI proposed to invest in chipmakers AMD and Broadcom. There are side arrangements with Microsoft. Figure 1 sets out some of the complex interrelationships.

Figure 1: AI Firm Inter-relationships and Cross-Investments

This intricate web of linkages creates risks. They complicate ownership and create conflicts of interest. It was not clear how any of these commitments will work or be funded if they proceed. Open AI’s ability to finance these investments depends on continued access to new money from investors because it currently does not have the resources to meet many of these long-term obligations.

These transactions distort financial performance. The firm selling capital goods reports sales and profits while the funding of the sale is treated as an investment. The buyer depreciates the cost over several years. Given that Nvidia seemingly upgrades its chip architecture regularly, depreciation periods of anywhere up to 5 years or longer seem optimistic. This means that dubious earnings boost share prices in a dizzying financial merry go round.

The AI bubble, with its growing gap between expectations, investment and revenue potential, eerily resembles the 1990s. But it is much larger. Investment may be 17 times that of the 2000 dot com and four times the 2008 sub-prime housing bubble.

AI’s acolytes deny any excess and argue that this time it is different because it is financed by equity capital. In fact, a large proportion is funded by debt with the amount tied to AI totalling around $1.2 trillion, 14 percent of all investment-grade debt.

The funding pattern is intriguing. Hyperscalers, firms that build and operate large data centres providing on-demand cloud computing, storage, and networking services, such as Microsoft, Meta, Alphabet and Oracle, are providing much of funding alongside venture capital investors. These firms are currently spending around 60 percent of operating, not free, cash flow, on capital expenditure, the vast majority of which is to support AI projects. This is supplemented by borrowing, relying on their credit standings, to finance their investments. Increasingly, a significant proportion of the funding is being provided by private credit with. expected volumes as high as $800 billion over the next two years and $5.5 trillion through to 2035. Given the high return, high risk appetites of these lenders, the level of financial discipline applied to these loans remains uncertain.

In effect, these large firm are now acting as financiers, borrowing money which is on-lent or invested in AI start-ups with unclear prospects. This exposure is troubling. Investor and lender assumptions that their exposure is to a strong firm is undermined where it is heavily invested in speculative AI ventures with unclear prospects. Microsoft’s share of Open AI’s losses is significant, over $4 billion in the latest quarter, representing around 12 percent of its pre-tax earnings.

Oracle’s experience is salutary. The shares rose 25 percent when it announced a transaction to provide cloud computing facilities to OpenAI. The data centres do not currently exist and will have to be constructed. The transaction requires Oracle, which is significantly leveraged, to borrow funds to create these centres meaning that the firm is taking significant exposure to Open AI. As of December 2025, investor concern was palpable. Given its current net debt of over $100 billion which will need to increase substantially to finance the data centres, the cost of insuring against Oracle default rose sharply and presumably will flow through into the value of existing debt and the cost of future debt. A credit ratings downgrade from its current BBB, low investment grade, is possible, potentially to non-investment or junk grade. Its share price has fallen to levels around that before the announcement of the OpenAI transaction. While Microsoft, Meta and Amazon have stronger balance sheets, the risks are not dissimilar.

The impact of the AI boom on the wider economy is material. AI companies account for 75-80 percent of US stock returns and earnings growth and 90 percent of capital expenditure growth. It has added around 40 percent or a full percentage point to 2025 US growth. Any retrenchment would affect the wider economy. It would also result in financial instability because of the direct and indirect exposure of banks and financial institutions to the AI sector. It is not inconceivable that some tech firms may require bailouts, such as that engineered for Intel, alongside familiar support for financiers, who will plead that without assistance the economy will collapse.

Investors have convinced themselves that the greater risk is underinvesting not overinvesting. Amazon founder Jeff Bexos hails it a “good kind of bubble” arguing that the money spent will bring long-term returns and deliver gigantic benefits to society, the tech-bro’s persistent bromide. Investors should be cautious. In the 1990s telecoms and fibre optic cable bubble, investors drastically overestimated capacity required. The percentage of lit or used fibre-optic capacity today, much of it installed during the dot com boom, is around 50 per cent, and global average network utilisation is 26 percent.

Investors believe that they have minimises risk by avoiding direct exposure to AI firms investing instead in firms like Nvidia, which provide the ‘picks and shovels’ of the revolution. The case of Cisco, for which the investment case during the halcyon days of the 1990 was similar, provides an interesting benchmark. It briefly became the world’s most valuable company on the largely correct assumption that its routers and other products would be crucial to the Internet. While the company’s financial performance has been generally steady, investors in Cisco lost out as its share price plummeted in 2000 only reaching the same level after 25 years.

When the dot com boom ended, Microsoft, Apple, Oracle and Amazon fell 65, 80, 88 percent, and 94 percent respectively taking 16, 5, 14 and 7 years to recover their 2000 peaks. The economy slowed requiring government support and historically low interest rates, at the time, to sustain economy activity which set off the housing boom which resulted in the 2008 crisis.

Consensual Tolkien-esque hallucinations notwithstanding, it would be surprising if the ending is different this time.

This is an expanded version of a piece first published on 4 November 2025 in the New Indian Express print edition.

Tyler Durden

Tue, 12/16/2025 - 14:05

Honda Motor's new N-BOX mini-vehicles at the company's headquarters in Tokyo on Aug. 31, 2017. Kazuhiro Nogi/AFP via Getty Images

Honda Motor's new N-BOX mini-vehicles at the company's headquarters in Tokyo on Aug. 31, 2017. Kazuhiro Nogi/AFP via Getty Images People cross a street under the hot sun in Tokyo on June 20, 2025. Kazuhiro Nogi/AFP via Getty Images

People cross a street under the hot sun in Tokyo on June 20, 2025. Kazuhiro Nogi/AFP via Getty Images

A marijuana grow site in California’s Mendocino County on Oct. 9, 2025. John Fredricks/The Epoch Times

A marijuana grow site in California’s Mendocino County on Oct. 9, 2025. John Fredricks/The Epoch Times

A sign advertises that "Food Stamps (EBT)" are accepted at a convenience store in Chelsea, Mass., on Oct. 24, 2025. Brian Snyder/Reuters

A sign advertises that "Food Stamps (EBT)" are accepted at a convenience store in Chelsea, Mass., on Oct. 24, 2025. Brian Snyder/Reuters

via Reuters

via Reuters

The U.S. Department of Justice in Washington on Oct. 21, 2025. Madalina Kilroy/The Epoch Times

The U.S. Department of Justice in Washington on Oct. 21, 2025. Madalina Kilroy/The Epoch Times

Recent comments