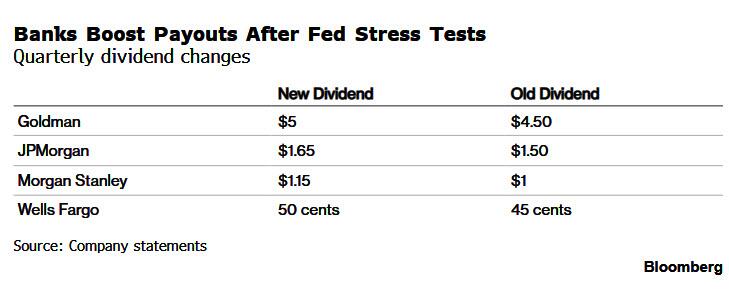

US Escalates Crackdown On Overseas Scam Network Targeting Americans

Authored by Arthur Zhang via The Epoch Times,

The United States has taken coordinated action against a Southeast Asia-based scam and money-laundering network that officials say used forced-labor compounds and online investment fraud to steal billions of dollars from Americans.

Scam center workers and victims from China arrive at the border checkpoint with Thailand, in Myawaddy, Burma, on Feb. 20, 2025. Hundreds of Chinese workers were heading home after being freed from online scam centers. STR/AFP via Getty Images

Scam center workers and victims from China arrive at the border checkpoint with Thailand, in Myawaddy, Burma, on Feb. 20, 2025. Hundreds of Chinese workers were heading home after being freed from online scam centers. STR/AFP via Getty Images

The Treasury Department on June 23 sanctioned 35 individuals and entities linked to the Prince Group Transnational Criminal Organization, a Cambodia-based network that U.S. authorities say operated scam compounds and laundered illicit proceeds through shell companies and financial channels.

Huione Group is a Cambodia-based conglomerate that U.S. authorities say provided laundering services for scam proceeds, including through Huione Guarantee, also known as Haowang Guarantee.

The Justice Department separately announced the seizure of a cloud-computing account it says helped run Huione-linked laundering services used by scam operations.

The Financial Crimes Enforcement Network, or FinCEN, also proposed extending a section 311 anti-money-laundering measure against Huione Group to H-Pay Service PLC and successor entities.

Together, the actions target three parts of a scam-and-laundering ecosystem: the Prince Group network, accused of running scam compounds; Huione-linked services, accused of moving illicit proceeds; and online infrastructure, allegedly used to support laundering services.

Treasury said U.S. authorities estimate that Americans lost at least $10 billion in 2024 to Southeast Asia-based scam operations, a 66 percent increase from the prior year.

"Scam centers in Southeast Asia steal billions of dollars from American victims each year," Treasury Secretary Scott Bessent said in the announcement. "Treasury will continue using its tools to disrupt the networks behind this egregious fraud and protect Americans."

Prince Group NetworkPrince Group is a Cambodia-based conglomerate led by Chen Zhi, also known as Vincent, whom U.S. authorities have accused of directing forced-labor scam compounds across Cambodia.

The Department of Justice (DOJ) unsealed an indictment against Chen in October 2025, charging him with wire fraud conspiracy and money laundering conspiracy. Prosecutors alleged that people held against their will in Prince Group-linked compounds were forced to carry out cryptocurrency investment scams. Chen remains at large, according to the DOJ.

Concurrently with the DOJ indictment, the Treasury's Office of Foreign Assets Control, FinCEN, and the UK Foreign Office imposed coordinated sanctions on 146 targets tied to the Prince Group network. It alleged at the time that Prince Group operated online investment scams targeting Americans and others worldwide and used a web of businesses and shell companies to launder illicit proceeds.

The June 23 action expands that pressure. Treasury's Office of Foreign Assets Control sanctioned nine individuals and 26 entities linked to Prince Group, including people it described as leaders, scam-compound investors, and front companies.

The Treasury said the new targets include Hu Xiaowei, whom it described as Prince Group TCO's "second-in-command," as well as several people it said were involved in investment, management, payment-gateway, or company-director roles tied to the network.

The Epoch Times could not contact Prince Group for comment.

DOJ Seizes Cloud AccountIn a concurrent action, the DOJ said it seized a cloud computing account used by Huione Group's subsidiaries that allegedly facilitated the movement of proceeds from cryptocurrency investment fraud, cyber scams, and other criminal activity across blockchains and into the banking system.

Huione Guarantee allegedly operated Telegram channels that included discussions about stolen credit card and identity information, malware-enabled theft proceeds, the procurement of individuals for human trafficking schemes, and the laundering of proceeds from romance and investment scams.

The department said the seizure is part of Operation Riptide, an FBI campaign targeting the actors, infrastructure, and financial networks behind cybercrime, cyber-enabled crime, and fraud against Americans.

"The FBI is committed to disrupting the infrastructure and services that cybercriminals rely on to profit from their illegal activity," said Brett Leatherman, assistant director of the FBI's Cyber Division, according to the DOJ's June 23 press release. "Today's action targets a key enabler of cyber-enabled fraud and money laundering schemes."

DOJ said the FBI's San Francisco Field Office and IRS Criminal Investigation are investigating the seizure case.

FinCEN Moves Against H-PayFinCEN's notice of proposed rulemaking says Huione Group remains a foreign financial institution of primary money-laundering concern and that the existing section 311 of the USA PATRIOT Act targeting Huione Group remains in effect.

The proposed amendment would add H-Pay Service PLC and any successor entity to the Huione Group definition.

FinCEN said the proposal is intended to address what it described as Huione Group's effort to circumvent the earlier measure by continuing to operate under a different name. The agency said H-Pay has effectively assumed Huione Pay PLC's business role within Huione Group.

The proposal is not final. Written comments on the H-Pay proposal must be submitted within 30 days after the NPRM is published in the Federal Register.

Scam Operations Target AmericansThe Treasury said one common scheme involves digital-asset investment fraud. Citing FinCEN's 2023 alert, Treasury said perpetrators often contact targets by text message, build trust through claims of friendship or romance, and steer victims into purported digital-asset investments on websites controlled by scammers.

Southeast Asia-based criminal organizations often recruit workers under false pretenses, including fake technology or customer-service jobs tied to casinos, resorts, and front companies. Once workers arrive at the compounds, operators confiscate passports and use debt bondage, physical violence, threats of forced prostitution, and other methods to coerce them into scamming people online, the Treasury said.

The Justice Department said reports of cyber-enabled fraud involving cryptocurrency continue to rise, with complainants reporting more than $7.2 billion in losses to the FBI's Internet Crime Complaint Center in 2025 from cryptocurrency investment fraud alone.

Tyler Durden Wed, 06/24/2026 - 22:50

Image source: United Russia

Image source: United Russia Source: Kelly Martin Designs

Source: Kelly Martin Designs

Image via Forbes & Caspian post

Image via Forbes & Caspian post

via UN News

via UN News

Microsoft co-founder Bill Gates (C) in Washington, on June 10, 2026. Kent Nishimura/AFP via Getty Images

Microsoft co-founder Bill Gates (C) in Washington, on June 10, 2026. Kent Nishimura/AFP via Getty Images

US President Donald Trump looks on as he stands in front of the VC-25B aircraft gifted by Qatar that will be used as Air Force One, at Joint Base Andrews, Maryland, June 19, 2026. ELIZABETH FRANTZ / REUTERS

US President Donald Trump looks on as he stands in front of the VC-25B aircraft gifted by Qatar that will be used as Air Force One, at Joint Base Andrews, Maryland, June 19, 2026. ELIZABETH FRANTZ / REUTERS Technicians mounting the wings onto the X-65 experimental drone.

Technicians mounting the wings onto the X-65 experimental drone. An artist’s render of the X-65 drone. Source:

An artist’s render of the X-65 drone. Source:  Treasury Secretary Scott Bessent at the Economic Club of New York, on June 23. Photographer: Krisanne Johnson/Bloomberg

Treasury Secretary Scott Bessent at the Economic Club of New York, on June 23. Photographer: Krisanne Johnson/Bloomberg

Recent comments