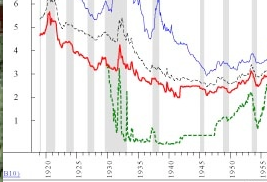

Previously in Part I of this series, I explained the need to re-examine economic indicators to determine how they performed in previous periods of deflation. In Part II, I looked at the year-over-year M1 vs. CPI indicator during the Roaring Twenties. In Part III, I looked at the same indicator during the 1930s and the post-World War 2 deflationary recession of 1948-49. That examination showed that, in the 1920-1950 period, the M1 vs. CPI indicator generally worked well, but missed the 1927 recession and most importantly of all completely failed to appropriately signal the beginning, duration, or end of the 1929-32 Great Contraction.

IV. Interest rates and the yield curve

In this installment, I will look at NY Fed interest rates, short term rates, and long term rates as they apply to the entire 1920-1950 period.

Recent comments