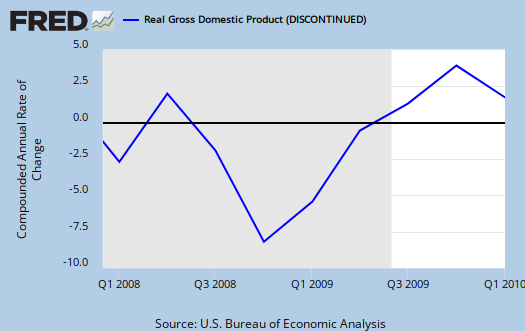

A 1st estimate of Q1 2010 GDP was released Friday and the advanced report is 3.2%. Here is the Q4 2009 GDP estimate. In the initial report, consumer spending (PCE) more than doubled in it's GDP contribution from Q4 2009.

As a reminder, GDP is made up of:

where

Y=GDP, C=Consumption, I=Investment, G=Government Spending, (X-M)=Net Exports, X=Exports, M=Imports.

In the first revision for Q1 20910, those numbers, which make up the total GDP percentage growth are:

- C = +2.55

- I = +1.67

- G = -0.37

- X = +0.66

- M = -1.28

So, what changed? Here are Q4 2009, 3rd estimate breakdown of GDP percentage:

- C = +1.16

- I = +4.39

- G = -0.26

- X = +2.36

- M = -2.09

From the report:

The deceleration in real GDP in the first quarter primarily reflected decelerations in private inventory investment and in exports, a downturn in residential fixed investment, and a larger decrease in state and local government spending that were partly offset by an acceleration in PCE and a deceleration in imports.

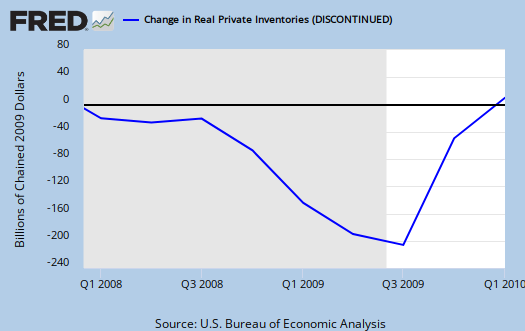

So, as we can see the C, or consumption (PCE), which reflects demand, increased dramatically. The personal savings rate dropped to 3.1%, down from 3.9% last quarter. A main change was in investments again, attributable to changes in private inventories. Fixed non-residential investment also was only 0.10 of the total 3.2% GDP, which reflects weak future growth, but most of that was in residential, down 10.9% from last quarter. Structures, which includes Commercial Real Estate, dropped 14% from Q4 2009. Note that changes in inventories accounted for 1.57, or almost half of the total 3.2% GDP growth.

The price index was also changed from 1.7% in Q1 2010. (paid more means bought less in quantity).

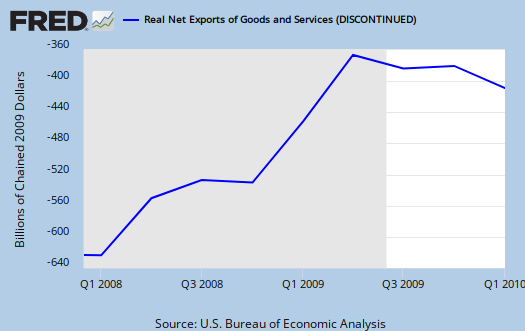

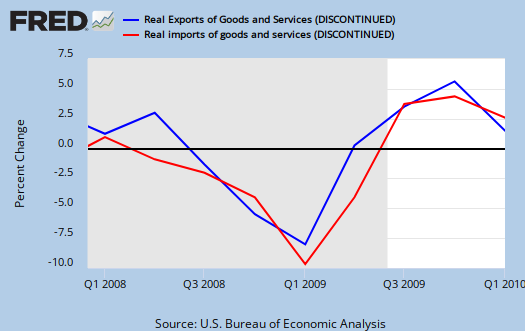

On imports and exports we see the a strange growth implosion on U.S. exports and numbers which imply a slow down in global trade, as well as increased the U.S. trade deficit. From the report, comparing Q4 2009 vs. Q1 2010:

Real exports of goods and services increased 5.8 percent in the first quarter, compared with an increase of 22.8 percent in the fourth. Real imports of goods and services increased 8.9 percent, compared with an increase of 15.8 percent.

The below graph is the change, quarterly, of real imports vs. exports. As we can see, there is a sudden drop in U.S. exports that goes against the grain of recovery.

So, what does this all mean? Signs of life on the economy but fairly lukewarm. One can say the U.S. consumer is back from the dead, but it appears that consumption is coming at the cost of personal savings.

Subject Meta:

Forum Categories:

| Attachment | Size |

|---|---|

| 151.77 KB |

Increase PCE/GDP- don’t forget consumer loans

As per Calculated Risk:

“PCE increased $130.7 billion; Personal Saving declined $88.5 billion and Gov’t social benefits increased $61.1 billion dollars. So the boost in PCE came from the decline in saving and the increase in benefits. That is not sustainable.”

Also, remember RO's observation on 4/25 the incredible spike in “Consumer leading” recorded for March. It seems that some of that first quarter PCE increase is correlated with increase consumer borrowing in March.

CR may be wrong about "sustainability", if March consumer lending continues into April and May, we may well see a similar second quarter increases in PCE and GDP. Also, why are government benefits not sustainable? There are no 'empirical' signs that there are limits on US goverment borrowing. Money the US borrows from China for example can be passed on as 'social benefits.'

What does not seem to be sustainable is unlimited consumer credit. That’s what got us into this mess in the first place- NO?

you're absolutely right Tom

The bottom line is increased consumer expenditures are not a result of increased disposable income. That's why I did a second graph-o-rama on personal income, which has the savings rate.

I saw CR's government transfers but I didn't graph it out. I didn't think it was that significant in comparison to consumer loans, but that's only in March, so 1/3rd of Q1, although we don't have a monthly breakdown of GDP.

Then, on inventories, the claim is those are a build up. Part of that is true, if you look at the graph, but part of it is also reduction, again from the graph.

What I find weird are some of the headlines. I read "business investment drives GDP" and all sorts of stuff, when one can see, it's nominal! Then it seems no one, except this post, talked about the decline in trade. That should not be happening, even if it was an increase in the trade deficit, for global growth. Both decreased. But the decline in U.S. exports is troublesome!

But CR's conclusion that PCE is not sustainable, yes, that's what i wrote in Personal income too, exactly what you're saying, "oh great, let's return to the past". that is what happened before and people uses their home equity as a ATM because the reality is the middle class have been decimated and cannot afford the "lifestyle" (read college, car, clothes).

Home Equites Tapped Out

Thats part of the dynamic going on here. That piggy bank can't drive the economy anymore because available credit facilities and home prices which might allow for that have decreased significantly.

Good analysis Robert very insightful. You may be seeing things that others are ignoring or just missing.

ty, I try, GDP will not drive job growth

That's what the site is about, digging around in the theory and statistics, going to the gov. databases, releases and trying to understand them. I find some things obscure, such as the definitions on some of the categories and locating the details. Gov. is improving, esp. the Federal Reserve, on publicly accessible data. I love the St. Louis Fed site, they just rock, make it so easy for the public.

One thing also, this just isn't strong enough or "Right" enough (need way more investment, non-structures) to drive the job growth the country needs. it's about ~2% just to maintain the status quo and then growth needs to be the "right" kind to generate jobs. This just isn't it.

It's just unreal, with all of the billions thrown at "Stimulus" so much was wasted and we could never get a real direct jobs program and/or business investment, startups/manufacturing policy/trade to jump start the real (read production) economy.

I think it's high time to focus on other policy areas, although financial reform monitoring push is probably job #1 right now for the site...

but other areas to build up a U.S. middle class again.

Home equities are tapped out but it looks like Visa/MC are stepping up to the plate again.

Prada, Oil and the Twin Deficits.

Wacky and counter-intuitive as it may be, the deficit is part of national savings. When the deficit increases, so does national savings. They used to say 'we owe it to ourselves'. Not any more.

That deficit savings number is adjusted for the BOP transfers out. Net imports are a subtract from GDP. Much of the PCE increase is in the increase in the size of net imports, and a lot of the bad news looks so good. Prada and Oil.

Burton Leed

infrastructure

This GDP number could have been followed by a lower unemployment rate had they pursued a real national infrastructure plan.

I think most writing on GDP

who are really reading the report and looking at the details would agree with you. I do not know how much "Stimulus" is in this, I do know "Stimulus" is deployed extensively through Q1 2010. That said, a real Stimulus, an direct jobs/infrastructure/manufacturing/trade reform, would have made the unemployment rate go down, no doubt about it.

I don't see much in here to sustain a recovery. About the only good news I see consistently is manufacturing output increasing, but it collapsed on the twin towers (sorry, that's what it reminds me of) so a long, long way to build up even to pre-recession levels and we know that manufacturing has been decimated by bad trade deals before this meltdown.