Part I of this series can be found here.

Parts II and III of this series can be read at The Bonddad Blog.

IV. The Federal Government must intervene to Rescue the States, in a morally responsible way

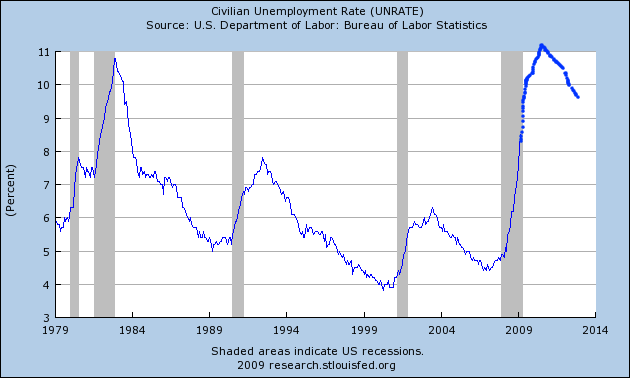

By far, the biggest threat to a bottom being put in to this Recession, is the continuing drumbeat of new layoffs. Thursday's June employment figures over - 450,000 and new jobless claims that have stubbornly, week after week, remained above 600,000, put the kibosh on any idea that the bottom is already here. We simply cannot stand 600,000 people putting in for jobless benefits, week after week after week. And the source of the continuing drumbeat of jobs lost appears to be coming more from anywhere else from the location of what Paul Krugman has called the "50 little Hoovers", i.e., the state (and municipal) governments, which are obliged to balance their budgets and so must throw employees out of work and cut back on spending projects, exactly when they are needed most.

Recent comments