Graham Platner Wins Maine Senate Democratic Nomination, Locking In Face-Off With Collins

Authored by Joseph Lord via The Epoch Times,

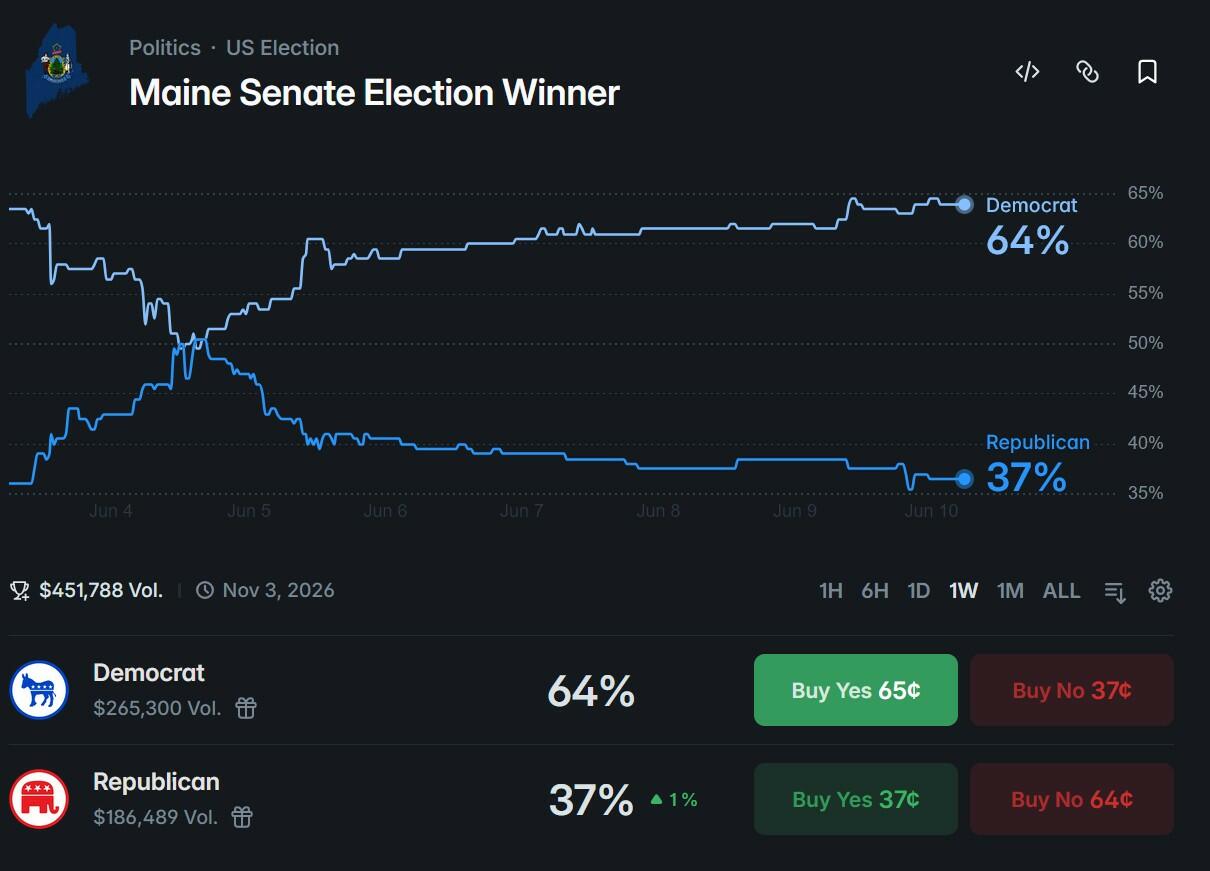

Democratic voters in Maine on Tuesday nominated oysterman and military veteran Graham Platner as their candidate to take on incumbent Sen. Susan Collins (R-Maine), locking in the nominees for one of the most critical Senate elections of the 2026 cycle.

Graham Platner, Democratic candidate for U.S. Senate, greets supporters after speaking at an event hosted by Sen. Bernie Sanders (I-Vt.) in Orono, Maine, on May 24, 2026. Robert F. Bukaty/AP Photo

Graham Platner, Democratic candidate for U.S. Senate, greets supporters after speaking at an event hosted by Sen. Bernie Sanders (I-Vt.) in Orono, Maine, on May 24, 2026. Robert F. Bukaty/AP Photo

At 9:23 p.m, The Associated Press formally declared that Platner would be the Democratic nominee. When the race was called, Platner led Gov. Janet Mills - who withdrew her candidacy after polls showed her trailing the dark horse Platner - by tens of percent, though only around 8 percent of the votes were in when the race was called.

Platner's campaign recently come under scrutiny after several media reports about his past treatment of women and other controversies.

Platner's victory formalizes the 2026 Senate lineup, locking in the final picks for a race that has been characterized as the political fight of Collins's life by many observers.

The five-term Collins was first elected in 1996 and has held on long beyond any other New England Republican at the federal level.

This year, she faced no Republican challenger for the nomination.

Though she regularly breaks with President Donald Trump and her party in the upper chamber, the political odds for a Republican in statewide matches have grown increasingly grim in recent years.

Aside from Collins, the last Republican to win a statewide federal race in New England was Kelly Ayotte, a New Hampshire Republican who won a single term to the Senate in 2010 before being unseated by Sen. Maggie Hassan (D-N.H.) in 2016.

Maine has never voted for Trump on a statewide level, with Vice President Kamala Harris winning by around 7 percent in 2024.

But Collins's brand of moderate, old-school Republicanism has kept her well ahead of most other Republicans in the state.

In 2020, Collins outran Trump by around 17 percent in Maine, defeating her Democratic rival by around eight points in an election former President Joe Biden won by around nine points.

Still, polls have painted a tough picture for Collins, who has fallen behind Platner in most polls conducted since March.

Platner has campaigned as a progressive candidate, winning the endorsement of key figures such as Sen. Bernie Sanders (I-Vt.) and Rep. Alexandria Ocasio-Cortez (D-N.Y.).

However, his campaign has faced some controversies.

The New York Times has run various stories against Platner, which include claims made by Lyndsey Fifield, a Republican political strategist who previously dated him.

Fifield claimed that on one occasion, while they were dating between 2013 and 2015, Platner twisted her arm. The New York Times stated in the article that it was unable to independently corroborate the allegation, which Platner has denied.

A report by The Wall Street Journal also relayed a story involving Platner exchanging sexually explicit text messages with other women during his marriage.

His wife, who knew about the infidelity, had shared the information with a campaign staffer, who later brought the story to The Wall Street Journal. Platner's wife has described the public reporting on the topic as "shameful" gossip.

Polymarket

Tyler Durden

Wed, 06/10/2026 - 08:50

Polymarket

Tyler Durden

Wed, 06/10/2026 - 08:50

Recent comments