At The Money: Agricultural Commodities, with Sal Gilbertie, Teucrium (June 24, 2026)

Looking for a non-correlated trading vehicle that is also a hedge against inflation? Perhaps Agricultural ETFs are a potential for your portfolio.

Full transcript below.

~~~

About this week’s guest:

Sal Gilbertie began trading agricultural and energy commodities in 1982 at Cargill, DLJ, Merrill Lynch, and Bear Stearns. He founded Teucrium in 2009, launching commodity-based AG products like the Teucrium Corn Fund (CORN) and the Teucrium Wheat Fund (WEAT), as well as soybeans and sugar futures markets through ETFs.

For more info, see:

Personal Bio

Professional

LinkedIn

~~~

Find all of the previous At the Money episodes here, and in the MiB feed on Apple Podcasts, YouTube, Spotify, and Bloomberg. And find the entire musical playlist of all the songs I have used on At the Money on Spotify

TRANSCRIPT: Do Agricultural Commodities Belong in Your Portfolio?

Barry Ritholtz with Sal Gilbertie, founder & CEO of Teucrium Trading

BARRY RITHOLTZ: Investors today can gain exposure to any asset class via ETFs — stocks, bonds, real estate, metals, energy, even crypto. One of the most overlooked sectors is agricultural commodities: wheat, soybeans, corn, sugar, coffee, all sorts of diversified commodities. And the ETF structure means a very different kind of K-1. I’m Barry Ritholtz, and on today’s edition of At the Money, we’re going to explore the question of whether agricultural products deserve a place in your investment accounts.

To help us unpack all of this and what it means for your portfolio, let’s bring in Sal Gilbertie. He’s the founder, CEO, and Chief Investment Officer of Teucrium Trading, best known for creating exchange-traded products that give investors direct exposure to ag futures. He’s also an old-school commodities trader since 1982, trading various agricultural and energy commodities. So, Sal, let’s start really basic. What makes agricultural commodities so fundamentally different from other commodities like energy, metals, or equities or bonds as an asset class?

SAL GILBERTIE: Sure. And thanks for having me, Barry. It’s always fun to be with you and talk with you. Let’s face it: everyone eats, and their animals eat. And that’s what ag is primarily used for. Although fuel now has come into the mix, ag is a very stable commodity in terms of the downside, historically. And we all know past performance is indicative of future results and all that. But the downside on ag is very limited, because farmers will just stop planting if they’re losing money.

And the secret with ag is that demand continues to rise. The combined global demand for corn, soybeans, and wheat since 1960 rises every single year. It’s a record, or it’s almost the record — so it’s either the second highest ever or it’s the highest ever, every single year since 1960.

BARRY RITHOLTZ: So is that driven by population growth, or is it driven by — I’m thinking about beef, which seems to not only be benefiting from the whole keto trend, but rising wealth in the rest of the world means people are eating more protein and less of other things. What’s the underlying driver of increased demand for commodities?

SAL GILBERTIE: You just hit it. The underlying driver is a rising population. And more importantly than that, a rising middle class — the people that rise from the bottom to the next level. So if you look at people who are in subsistence living, which used to be defined as, I think, less than $10 a day — $10 equivalents a day — the moment they rise from that, and there are hundreds of studies on this, they increase the protein in their diet, they increase eating meat. That’s what they do.

And that is a huge demand. The number one demand around the world for corn is feeding cattle, feeding animals in general. The second highest demand is for fuel. So corn goes into ethanol, and soybeans go into biofuels. And so what happens is the rising global population, the growing middle class — which has become huge, by the way. I think, as a percentage of the population, we’re at our lowest ever percent of people in the bottom rung.

BARRY RITHOLTZ: That’s amazing. Does this mean we’re going to see a beef ETF — ticker BEEF — from you sometime soon?

SAL GILBERTIE: No. It’s really hard to get people to think about ag — it’s really hard. It’s amazing to me. We always say corn is in everything, right? So the number one use is feeding animals. Number two use is ethanol production. It makes starch — if you use paper, you’re using corn. People don’t realize that. So it’s literally impossible for anyone, anywhere on planet Earth, to not be using corn every single day, either directly or indirectly. It’s not possible. And people don’t understand that it’s a vital commodity.

And so, going back to your original question, it’s a commodity, so it’s volatile, but it has this floor because governments around the world subsidize food production. They subsidize their farmers, because you don’t want your populace to destabilize because they’re hungry — you lose power. So everybody subsidizes their farmers, and farmers get used to operating at breakeven.

And that actually is — I think you’ve mentioned it — the golden grain cycle. We can get into it, but grains kind of flatline and get used to trading there. And because that demand is very static — it’s not a dynamic demand, it’s just always growing — it doesn’t really fall significantly when there’s a disruption. Ninety-nine times out of a hundred that means it doesn’t rain somewhere critical. And one time out of a hundred it means there’s a war, there’s a political upheaval, and the transport of grains, the access to grains, might be limited. They explode higher — they go higher really quickly — because people are afraid.

BARRY RITHOLTZ: That’s really interesting. So you mentioned the golden grain cycle. Walk us through what that means. Where are corn, wheat, soybeans in that cycle today?

SAL GILBERTIE: Sure. The golden grain cycle was developed by Jake Hanley — I think you know him very well. We looked at it and said, look — because we just looked at the spot continuation, the continuation price of the front month of futures over time. And the bottom line on corn is a prime example: between $3.50 and $4 over the last 17 years — actually approaching 19 years, since the Renewable Fuels Act of 2007, 2008. Corn doesn’t go below that. I think it’s traded a few weeks under $3.50 in the last 19 years. I can tell you that in the last five years, corn has only traded under $4 four percent of the trading days.

So clearly the breakeven is between $3.50 and $4, and closer to $4 right now. So if you see corn down near $4, based on past history you’re saying, well, wait a minute — I have limited downside. And in the last 19 years, three times corn has doubled from that price. Twice because of a drought, and once because of the war in Ukraine, which was preceded by a drought in the upper Midwest and problems with China grain production — wheat production — so you had a wheat problem that kind of started the rally. And then Russia invaded Ukraine in 2022, and everything went bonkers. The rally started in 2020 in wheat, and then it went to the whole grain complex.

So if you’ve got an asset and you say to somebody, I’ve got this asset that trades at X, and when there’s a supply disruption every four to seven years, it goes to 2X and then it trades back down to X — and then rinse, repeat. So stage one of the golden grain cycle is trading sideways at X, stage two is going to 2X, and stage three is going back to 1X.

BARRY RITHOLTZ: So it sounds very much like these are trading vehicles that you’re looking to take advantage of these disruptions, such as war or droughts. What are the other variables investors should be aware of? Obviously weather — the war in Iran sent fertilizer costs skyrocketing, I’ve been reading about farmers complaining about that. And then government policy. I’ve been a big fan of both Harry’s Farm and then Clarkson’s Farm on Netflix, both of them complaining about policies in the UK, which are now taxing farm estates and taxing fertilizer and taxing everything from tractors to what have you. How significant are government policies, and what are the other variables investors should be thinking about?

SAL GILBERTIE: Sure. So, in order: the main variable is always weather. And then geopolitical upheaval, like a war — like what happened with wheat when Russia invaded Ukraine. Between Ukraine and Russia, they’re almost 40% of the world’s exportable wheat supply, and everybody was afraid it would get locked in. Well, it didn’t get locked in. So you had this price spike.

And the reason price spikes is because you run out of grain. Remember, you plant grain in the spring, it grows all summer, there’s a big pile at harvest in the fall. And then you take from that pile — the whole world’s taking from that pile — autumn, winter, spring, and summer, because it’s still growing, it’s not harvested yet. And in general, at the end of that cycle you have about six months’ supply of wheat. Historically, you have about three or four months’ supply of corn and soybeans. So if there’s a disruption and that big pile is reduced by 10%, 20%, 30%, now you’re approaching zero in corn and soybeans.

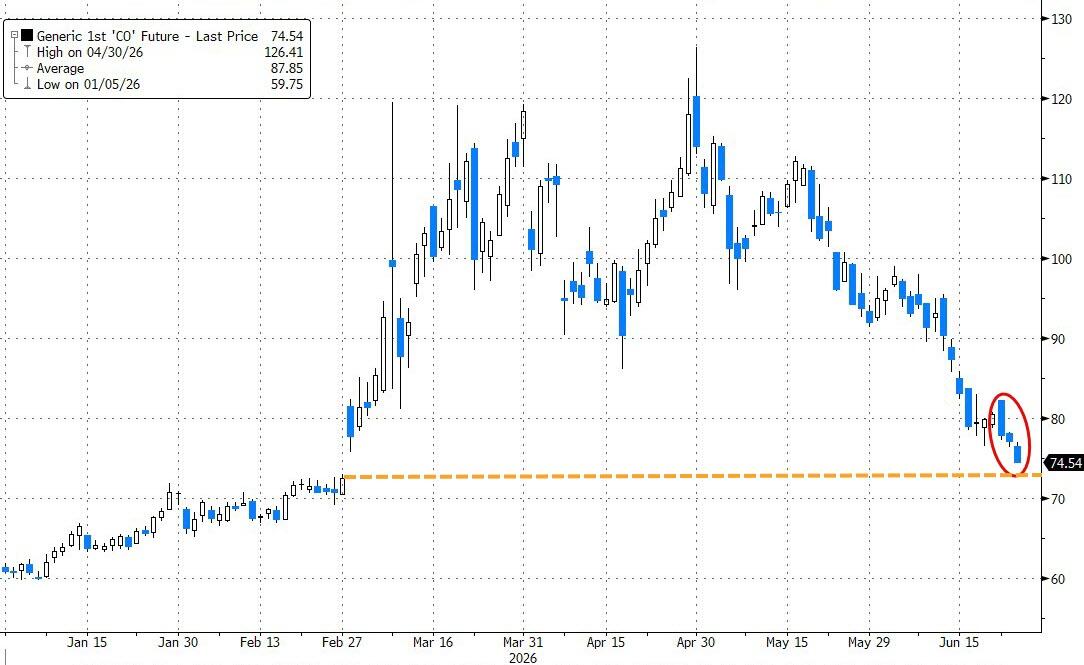

So that’s why the price generally takes a spike in July, if they realize it’s not going to rain in the US corn belt — there’s the weather factor. Prices spike and go up, and they run up. In the next year, what we’ve seen is a lot of money coming into our ETFs. We had, I don’t know, $200, $250 million in our ag ETFs right before the Iran war broke out, and now we have $800 million to a billion, depending on the day. But the price hasn’t really gone up — the price went up maybe 10%.

The reason is people are positioning for next year. The fertilizer story is a 2027 story. Farmers will fertilize mid-season — around now, just to get — they call it side dressing, and that’ll boost the yields — that’s going to be cut back around the world. But a lot of farmers pretreat their fields, especially corn farmers, in the autumn. They get ready so they can get in there in the spring and get everything down. So some of the fertilizer is either priced or laid down in the autumn for next spring. If the fertilizer price remains high in the autumn, or the availability remains limited, you will affect next year’s yields. And I think that’s what investors have done.

And back to your point: if it’s a tradable product, it’s more a strategic allocation, because these doubles that have happened prior to now — and again, it’s just historical, not making any predictions, we’re not allowed, you can’t — but if you have to be prepositioned, I think investors are saying, well, wait a minute, if I stick 1% of my portfolio in corn, or beans, or wheat, or whatever, my downside is pretty limited based on history if I’m buying within 10% of the breakeven price, and my upside is like 90% based on history.

And it’s going to be stable, because — setting aside the one or two days every couple of years that are black days, where everything goes down — grains really remain stable as a portfolio stabilizer. And so people are kind of layering in, trying to say: maybe the stock market’s frothy, maybe I’m getting a little too risky, bonds kind of move in tandem with stocks — what am I looking for that has a lower correlation? Everything’s correlated on certain days, but grains have some of the lowest correlation around, besides natural gas and sugar.

BARRY RITHOLTZ: Really interesting. One of the thoughts I always consider when I’m looking at agricultural products or commodities is as a hedge to inflation — prices go up on food, prices go up on key commodities. There are a lot of different ways to hedge inflation, and owning the commodities that go up is a significant aspect of this. How do investors use commodity ETFs as an inflation hedge?

SAL GILBERTIE: They do. I think when people see inflation coming, or feel it coming — and any commodity, we’re grain-focused, right, but any commodity — if you see it down at its breakeven level. And you don’t have to be an expert in that commodity. Look at a chart, look at a long-term chart, a decade or two. Wherever it flatlines, it’s usually around the same number. That’s your breakeven, that’s your futures-equivalent breakeven cost. Everybody can see those charts. That’s when you might want to layer in, because your downside based on history is limited, and your upside — you can move steadily up with inflation, which we have. Again, that breakeven price of corn used to be $3.50. It’s clearly around $4 now — maybe a little high.

BARRY RITHOLTZ: Really interesting. You know, the first time I ever heard of a USDA crop report was frozen orange juice futures from the movie Trading Places. How significant are these USDA reports to these underlying ag products? Do investors need to track this the way equity or bond investors track non-farm payrolls?

SAL GILBERTIE: I think so. And the reason is — granted, it’s not quite as dramatic, because you may not be as good at predicting the numbers as you are with, say, payrolls. And those numbers get adjusted, as do the ag numbers sometimes. But everybody here knows there’s a whole sub-industry within agriculture that’s watching. They kind of know what the USDA is going to put out. But the USDA is the gold standard. So when that report comes out, all of your hedge funds, all of your pension funds, all the big institutional investors — who, quite honestly, are looking for opportunities — they also want to cover their rear. So if you’ve got the USDA as your gold standard, you just follow that. If the USDA confirms what everybody else already knew, fine, you’re a little late to the game, but you’re probably going to be okay anyway. So yeah, those reports are really big.

The scary thing, Barry — you and I can probably both relate — is when we give speeches now and I say, how many people have seen Trading Places, far more than half the room now has a blank look on their face. Nobody under 35 even knows what the movie is.

BARRY RITHOLTZ: Really? God, that’s awful. Oh my God, it’s just awful. I’m genuinely shocked at that.

SAL GILBERTIE: We require our interns to watch it. You’ve got to watch it.

BARRY RITHOLTZ: It’s Eddie Murphy’s — it could be his very best movie. I think so too. So, you mentioned earlier drought, we talked about war. Given the rise of prediction markets, everybody’s trying to figure out what’s going on. How much of the information about either weather or geopolitics or whatever — even a poor harvest — how much of that is already embedded in crop prices?

SAL GILBERTIE: Most of it is. The one caveat, again, as I referenced earlier: if you get a drought in the US Midwest around July or August — which is what they call kernel fill and pod fill, when the corn gets its kernels and when the soybeans fill their pods — if you’re too dry and hot in that period, it hits hard. And the US being the world’s second-largest exporter of both those commodities — we’re second to Brazil now — that hurts a lot.

But you can see it. So by the end of June, if it’s been dry and hot and the 14-day forecast says it’s going to stay dry and hot, you see that price start creeping up. And you can look back at drought years in the price charts. So it gets built in, but you don’t know how bad it is until harvest. In drought years, you get this slow dribble up, and then when you get confirmation in autumn, late autumn, you get that wintertime spike up.

Seasonally, though, the corn low is a double low. One is the middle to late August — that’s a good time to look at layering corn in, if you’re so inclined to do that to your portfolio, because that’s when people have a really good idea that the crop’s going to be good or bad. And then October 1st is actually — when you do a 20-year or 30-year smooth seasonal, October 1st, the first week of October, is the cyclical low. The actual absolute price low often occurs in August. So August, when you get a good read on the crop — it rained during that critical time, everybody’s happy — and then October, because the whole big pile is on the ground, everybody’s feeling comfortable. Those are good times to look at layering these things into your portfolio.

BARRY RITHOLTZ: Really interesting. China has become the dominant buyer of so many agricultural products, as well as other commodities. How has their growing economy and even geopolitical importance changed the way grain markets trade?

SAL GILBERTIE: It has changed the way commodity markets trade. I’ve watched China for decades, and as they become a net importer of something — so when they became a net importer of crude oil, that changed the crude markets; when they became a net importer of corn, that changed the corn markets; when they became a net importer of wheat, that changed the wheat markets; when they increased their importation of soybeans, they became the soybean market. China buys most of the world’s soybeans that are available for export.

Only three countries export soybeans, basically: Brazil, the United States, and Argentina. Paraguay — a little blip there, but you can’t really see it on a pie chart, it’s so small. And so those three countries, if they have an export problem, China has a problem, because China’s the largest swine herd. They feed swine soybean meal, so they’re gigantic importers of soybeans. So yeah. The interesting part is soybeans — they’ve kind of maxed out — but on corn and wheat, every year, if you look at long-term trends, they increase how much. Exactly like oil: the amount of oil they import just keeps going up.

BARRY RITHOLTZ: Really interesting. Given the rising role of China in commodity imports, what was the impact of all the mayhem the past year with tariffs? Did that have a significant effect on how much US grain farmers were able to export?

SAL GILBERTIE: Kind of. Because in Trump’s first term, when he did the tariffs, that changed everything. China basically shifted toward Brazil as their first source of choice for soybean imports, away from the US. So it kind of shifted that.

BARRY RITHOLTZ: And that persists — the US fell behind Brazil in exports to China?

SAL GILBERTIE: Yes, absolutely. And Brazil’s beans, by and large, have been cheaper lately anyway. So China — tariff or not — they’re going to go where the cheaper beans are. When China buys our beans now, it’s the state buying them, because our beans are more expensive, and they’re sending a political signal of goodwill toward the Trump administration.

China, I will note, saved the world by cutting down on their crude imports. Their crude imports largely were to support their strategic petroleum reserve. In the last couple of years, they’ve been importing much more than they actually used, to boost up their reserves. China is the number one reason that crude demand went down since the Iran war started. China saved the world — China saved energy prices. Everybody said $150, $200 a barrel, right? If it weren’t for China cutting back on their energy imports, we would’ve seen that.

BARRY RITHOLTZ: I think a lot of people in the United States underappreciate how aggressively — and let’s just call it cleverly — China has pushed into alternative energy, everything from geothermal to solar to wind. Not a surprise there. There are certain things that you can’t replace crude oil with, but everything else they can, and they seem to have really made an effort to do so.

SAL GILBERTIE: Correct. And — don’t quote me on this, I don’t know for sure, we’d have to go look it up — but I think their fossil fuel usage is still going up. You can’t do without it. And the fact that, thank goodness, they were filling their strategic petroleum reserve versus actually needing the oil — so when the Iran war came, they’re not going to pay high prices to fill some reserves. They just stopped importing all that crude, and that has helped us tremendously.

BARRY RITHOLTZ: Yeah, China is not doing this because they’re advocates against carbon and climate change — they’re doing it for strategic reasons. But let’s talk about climate change for a moment. I know in New York our growing season is longer. I’m a gardener, and there are certain plants that I can plant now that 15 years ago I was told there’s no way they’d survive in New York. What does the changing temperature, the changing climate, do to crop yields? Is this a persistent upward trend? Is this going to help prices, or is this just going to create more volatility?

SAL GILBERTIE: I think more volatility. Because rain makes grain, and a warmer earth — honest to God, rain makes…

BARRY RITHOLTZ: Rain makes grain. I love that.

SAL GILBERTIE: A warmer earth — the atmosphere, when it’s warm, holds more moisture, and so you actually get more rain. So global warming has been really good for crops around the world. It’s a really good thing for crop production. That might sound counterintuitive to people. Our phones ring off the hook when you get the occasional storm and a million or 2 million acres flood out in the US, and you get the news flying helicopters over, and as far as you can see all these farms are underwater, and we get the call: what’s that going to do to food prices? Well, they popped up a little bit, but you might want to sell the rally, because — we plant 400 to 500 million acres in the United States. You lose 2 million acres, no one cares in terms of the absolute price. The only people who care are those poor farmers who are underwater. That’s it. And hopefully they have crop insurance.

BARRY RITHOLTZ: So everybody who’s flooded out — the less than 1% — suffers, but the rest of the rain brings more crop, you’re saying?

SAL GILBERTIE: Absolutely. Absolutely.

BARRY RITHOLTZ: Really interesting. You know, we’ve talked about everything but technology. I mentioned I’m a fan of Clarkson’s Farm and Harry’s Farm, and some of the technology — just looking at these tractors run themselves. Autonomous vehicles have been on the farms for years, long before any of the robotaxis that are out there. What does improving technology do to agricultural productivity? Are we seeing precision irrigation, better seeds, higher-quality machinery? What is this doing to production, what is this doing to quality, and what does this mean for price?

SAL GILBERTIE: By and large it’s raising everything except the price. So thankfully, everything you just mentioned has worked perfectly. Because, again, back to 1960, that rising global demand for combined corn, soybeans, and wheat — if you look at the supply line, it follows that very closely, other than in a drought year. So except in a drought year, we generally grow as much or more than we need. And that’s only because of genetic engineering of seeds, of amazing technology. Tractors now not only can be autonomous — they used to run three to five miles an hour, and you had to kind of guess at your fertilizer. Now they run nine miles an hour across these fields, adjusting the fertilizer every three feet, based on the analysis in the soil. They’ve got these amazing laser weeders, so you can actually go over your…

BARRY RITHOLTZ: Zap ’em without chemicals.

SAL GILBERTIE: Zap ’em — you can do stuff without chemicals. And there’s more and more organic land being set aside for less chemicals. It’s all so wonderful. It’s a beautiful world when you look at agricultural technology. It’s amazing.

BARRY RITHOLTZ: So, to wrap up: anyone interested in having exposure to agricultural commodity products — whether you think the price trend is going to go higher, or just as a hedge against inflation — check out some of the ETFs you can get that can give you exposure to wheat, soybeans, sugar, or any combination of things. I’m Barry Ritholtz. You are listening to Bloomberg’s At the Money.

~~~

Find our entire music playlist for At the Money on Spotify.

The post At The Money: Agricultural Commodities appeared first on The Big Picture.

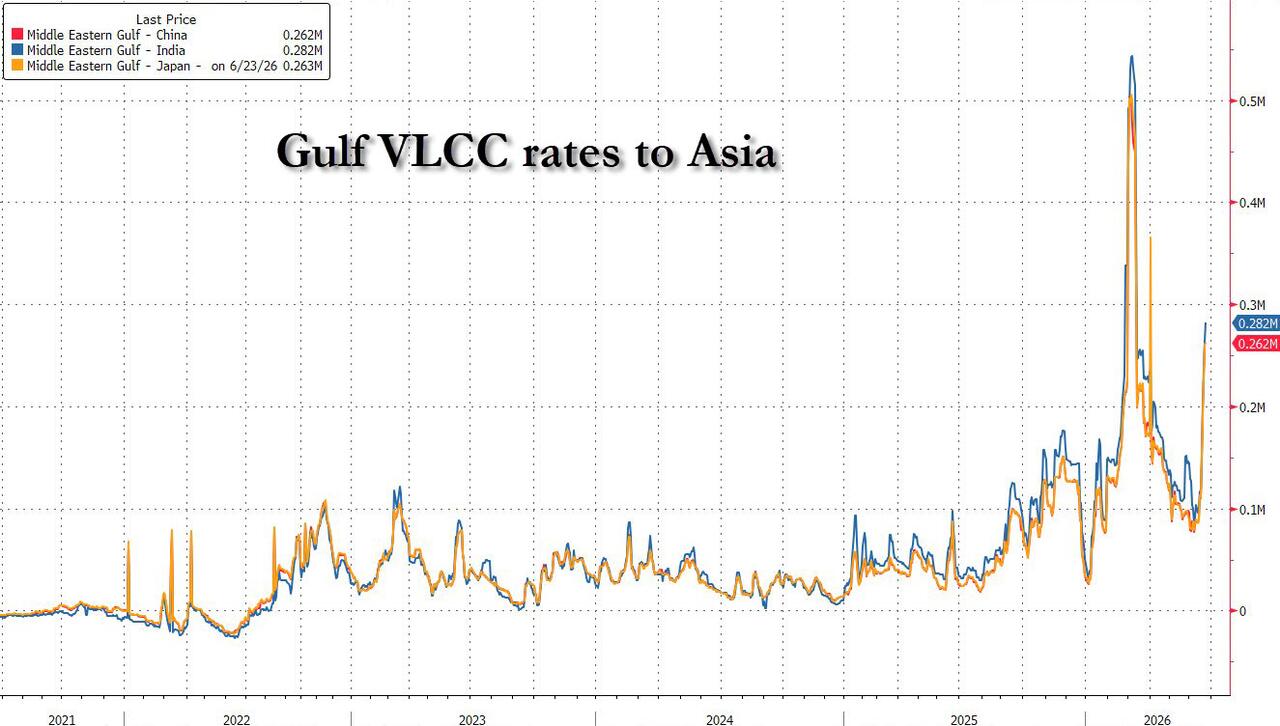

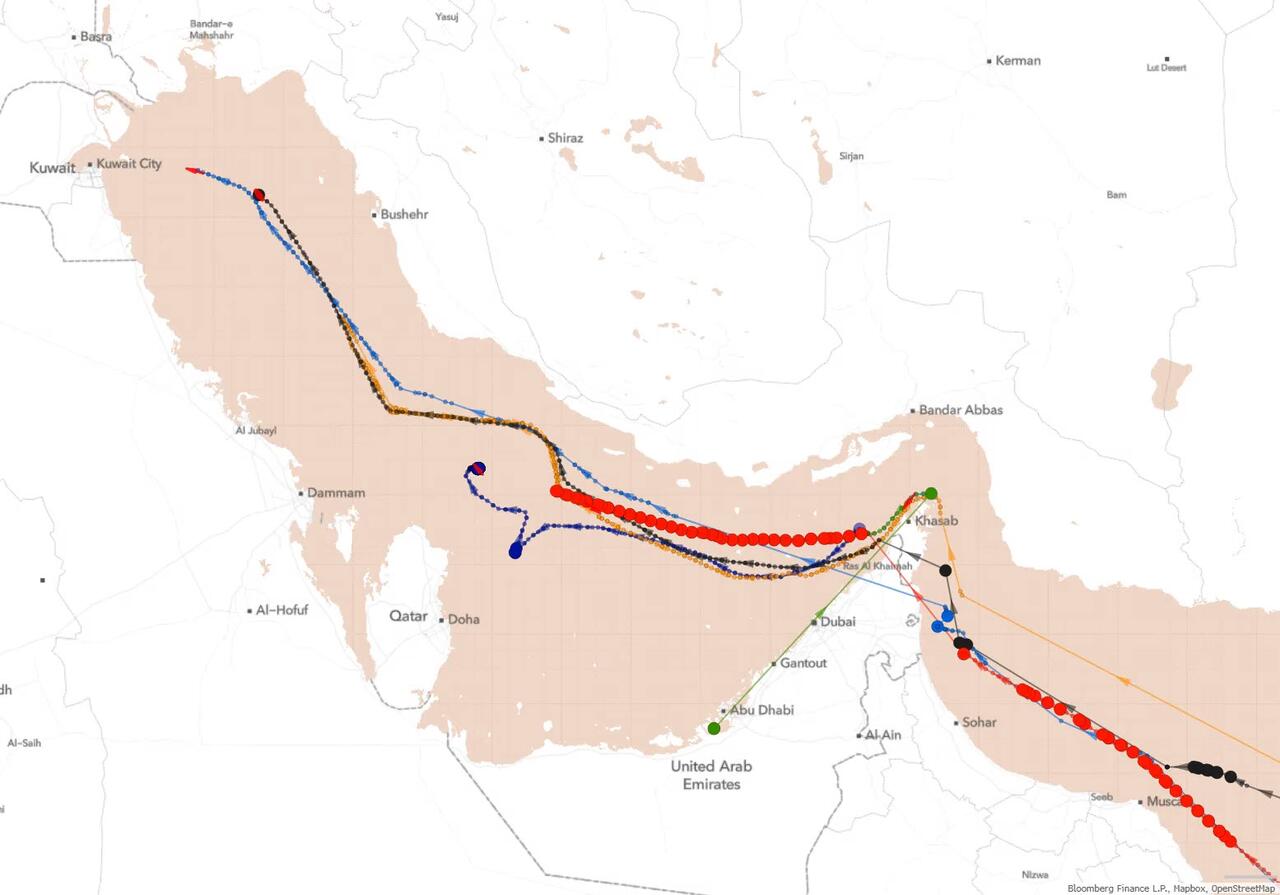

At least seven very large crude carriers have sailed into the Persian Gulf since the US and Iran agreed to an interim ceasefire deal late last week.Source: Bloomberg

At least seven very large crude carriers have sailed into the Persian Gulf since the US and Iran agreed to an interim ceasefire deal late last week.Source: Bloomberg

Iranian state media

Iranian state media Several attacks on Moscow refinery in a matter of days, via AFP

Several attacks on Moscow refinery in a matter of days, via AFP

Recent comments