Bitcoin Perps' Algorithmic '0.01%' Scythe: How The Funding-Rate Mechanism Explains Your "Mystery" Liquidations

Authored by danny (@agintender) via WuBlockchain's Aki Chen,

Why is derivatives trading the exchange’s money printer? Why do some venues dare to take the other side of their customers’ trades? By unpacking the funding-rate mechanics of Bitcoin perpetual futures (perps) and the surrounding market dynamics, we show how traders are led—step by step—into a fatal trap meticulously engineered by the exchange.

The so-called “0.01% equilibrium” in perps - akin, in spirit, to the 0.618 Fibonacci motif - operates as a razor-fine instrument for surgical rent extraction.

Introduction

In the realm of crypto derivatives, Bitcoin (BTC) perpetual futures have become one of the most liquid and influential instruments. Active traders often note a distinctive pattern: across most market conditions, the funding rate on BTC perpetuals appears to gravitate toward about 0.01%. This figure is neither random nor a direct proxy for market sentiment; it is the product of the instrument’s deliberate financial-engineering design.

Based on Coinglass’s recent historical data, the distribution of BTC perpetuals’ funding rate shows a clear clustering pattern. For the vast majority of the past year, the rate hovered tightly around +0.01% as its central tendency. Material deviations typically appeared only during brief bouts of acute market volatility, providing strong quantitative support for the observation that “0.01% is the norm.”

How to Read This Article

From the underlying architecture of perpetuals and the funding-rate formula to arbitrageurs’ behavior and regime shifts in extreme markets, this article attempts to unpack—and demystify—the deeper logic and market dynamics behind the 0.01% equilibrium.

-

For beginners or readers seeking theoretical foundations: read Sections I–II in order to understand the core mechanisms and formulas.

-

For professional traders and arbitrageurs: focus on Sections III and V for details on arbitrage mechanics, venue differences, and actionable strategies.

-

For risk managers: Section IV—the analysis of extreme market conditions—is essential.

I: Architecture of Perpetual Futures and the Funding-Rate Mechanism

To understand the origin of the 0.01%, one must first grasp the design intent and core mechanics of perpetual futures themselves. Perpetuals aim to deliver a futures-like trading experience while cleverly sidestepping the chief complexity of conventional futures—expiry and settlement at maturity.

1.1 The No-Expiry Problem

Traditional futures have a fixed expiry date. As expiry approaches, arbitrage by market participants naturally forces the futures price to converge toward the spot price of the underlying, such that the two are effectively aligned at settlement. In this sense, the expiry date serves as a powerful price anchor.

However, by removing the expiry date, perpetual futures allow traders to hold positions indefinitely. This convenience introduces a serious financial-engineering problem: without the terminal anchor of expiry, how can one ensure that the perpetual’s price does not drift persistently and materially from that of its underlying (e.g., BTC spot)?. Absent an effective anchoring mechanism, the price of a perpetual could wander indefinitely under speculative sentiment, undermining its fundamental roles as a price-discovery and hedging instrument. This design stands in sharp contrast to traditional finance, where interest rates are set by central banks and the interbank market; here the adjustment is endogenous to the market, operating as a peer-to-peer regulatory mechanism.

1.2 Funding Rate: The Core Solution for Price Anchoring

To solve this problem, exchanges designed the funding-rate mechanism. The most important point to understand is this: funding is not a fee charged by the exchange; it is a periodic payment exchanged directly between longs and shorts. In essence, the mechanism is a dynamic, deviation-based compensation system whose sole objective is to anchor the perpetual’s market/mark price to the underlying asset’s spot index price.

Mechanics:

-

When the perpetual price > spot price: market bias is bullish and longs dominate. Funding is typically positive, so longs pay shorts. This raises the cost of holding longs and incentivizes traders to sell the perpetual and/or buy spot, pulling the perp back down and/or spot up toward parity.

-

When the perpetual price < spot price: market bias is bearish and shorts dominate. Funding is typically negative, so shorts pay longs. This raises the cost of holding shorts and incentivizes traders to buy the perpetual and/or sell spot, pushing the perp up and/or spot down toward convergence.

This design reflects a nuanced governance philosophy: instead of directly intervening in prices, the exchange sets incentive rules that prompt market participants—especially arbitrageurs—to correct price deviations through their own profit-seeking behavior. The result is a system with greater resilience and incentive-based self-correction. Accordingly, the funding rate is not merely a feature of perpetuals; it is the core engine that enables them to function properly.

This design reflects a nuanced governance philosophy: instead of directly intervening in prices, the exchange sets incentive rules that prompt market participants—especially arbitrageurs—to correct price deviations through their own profit-seeking behavior. The result is a system with greater resilience and incentive-based self-correction. Accordingly, the funding rate is not merely a feature of perpetuals; it is the core engine that enables them to function properly.

II: Deconstructing the Funding-Rate Formula — Interest and Premium Components

To answer precisely “why 0.01%,” we must examine the mathematical makeup of the funding rate. The observed 0.01% is not a number directly set by supply–demand; it is chiefly determined by a fixed parameter preset by the exchange.

Most major venues—such as Binance and OKX—use a broadly standardized formula:

Funding Rate = Premium Index + clamp(Interest Rate − Premium Index)

This makes clear that the funding rate comprises two core parts: the Premium Index and the Interest Rate.

2.1 Premium Index: A Direct Readout of Market Sentiment

The Premium Index is the fully market-driven component of the funding rate. It directly measures the gap between the perpetual’s mark/market price and the underlying spot index price. Its calculation is typically more intricate, aiming to reflect genuine buy/sell pressure while deterring manipulation. For example, venues often use depth-adjusted “Impact Bid/Ask Prices” (the average execution price for a reasonably large order, better capturing order-book depth) and apply a moving average over a lookback window to smooth short-term noise. Methods and sampling intervals vary across platforms; traders should consult each exchange’s documentation for exact definitions.

● Premium Index > 0: the perpetual trades above the index price, indicating buy/long demand outweighs sell/short pressure.

● Premium Index < 0: the perpetual trades below the index price, indicating short-side pressure dominates.

In essence, the Premium Index is a barometer of leveraged directional demand.

2.2 Interest Rate: The Source of 0.01%

This section answers the question directly. The 0.01% figure comes from the “Interest Rate” term in the funding-rate formula—a parameter pre-set by the exchange, not an immediate outcome of supply and demand.

Binance, OKX, and Bybit state in their documentation that the interest rate is effectively 0.03% per day (Binance specifies a fixed 0.01% per 8-hour interval). Because funding is settled every 8 hours (i.e., three times per day), the per-interval interest component is 0.03% ÷ 3 = 0.01%.

Why do exchanges set a fixed positive rate? This component is intended to proxy the cost of carry in the real world. For a BTC/USDT perpetual, it represents the interest-rate differential between the quote currency (USDT) and the base asset (BTC). In traditional-finance terms, a 0.03% daily rate translates to roughly 10.95% on a simple annual basis, which corresponds to a relatively elevated USD funding cost and reflects the risk premium inherent in holding highly volatile crypto assets.

Put differently, if you hold a perpetual position you effectively pay ~10% annualized on your levered capital—much like borrowing to buy the asset and paying interest on the funds.

This design has an important structural implication:

1. In a perfectly balanced market—where long/short sentiment offsets—the Premium Index should be ~0.

2. The funding formula collapses to: Funding Rate = 0 + clamp(0.01% − 0), yielding 0.01%.

3. Hence even with no price dislocation, longs still pay shorts 0.01% per funding interval.

This setup is not neutral. It imposes a small but continuous cost of carry on long positions while providing baseline carry income to shorts. On one hand, it gently discourages indefinite, idle, high-leverage longs; on the other, it supplies market makers—who are often net short perps for hedging—with stable base revenue, thereby incentivizing them to supply liquidity.

III: The Invisible Hand of Arbitrage — Forcing the 0.01% Equilibrium

Given that 0.01% is a preset benchmark rate, the next question is: why doesn’t market pressure (i.e., the Premium Index component) typically overwhelm this benchmark and push funding into wide swings? The answer lies in a powerful, efficient market force: arbitrage.

Because the market hosts a large cohort of professional arbitrageurs who relentlessly eliminate opportunities embedded in the Premium Index, the interest-rate term becomes the dominant driver of funding. As a result, 0.01% tends to prevail as the baseline norm.

3.1 Emergence and Removal of Arbitrage Opportunities

Whenever a material divergence arises between the perpetual’s price and the spot/index price, a theoretical risk-free profit opportunity is created. Arbitrageurs, via automated (often co-located) trading systems, detect and execute these trades in milliseconds, rapidly compressing the basis dislocation.

Note 1. Delta-neutral means the portfolio’s value is insensitive to small changes in the underlying asset’s price (i.e., portfolio delta ≈ 0).

Note 2. If, at the time of entry, no spot is purchased for hedging, the position is colloquially called a naked short/long.

This arbitrage flow is also one of the important bridge use-cases connecting CeFi and DeFi: arbitrageurs frequently shuttle assets between the two to capture superior interest-rate or basis opportunities (e.g., Wintermute, DWF Labs, Jump Crypto).

3.2 Evidence of Market Efficiency

Today’s crypto markets are highly institutionalized, saturated with quantitative trading firms deploying sophisticated algorithms. Fierce competition among these firms means any meaningful basis dislocation (i.e., a significant Premium Index) is identified almost instantly and arbitraged away.

Accordingly, the persistent observation that funding hovers around 0.01% is itself strong evidence of a highly efficient market. Behind this stable figure lies continuous high-frequency arbitrage, executed by innumerable arbitrage bots, the “invisible hand” that keeps the Premium Index compressed within a narrow band near zero.

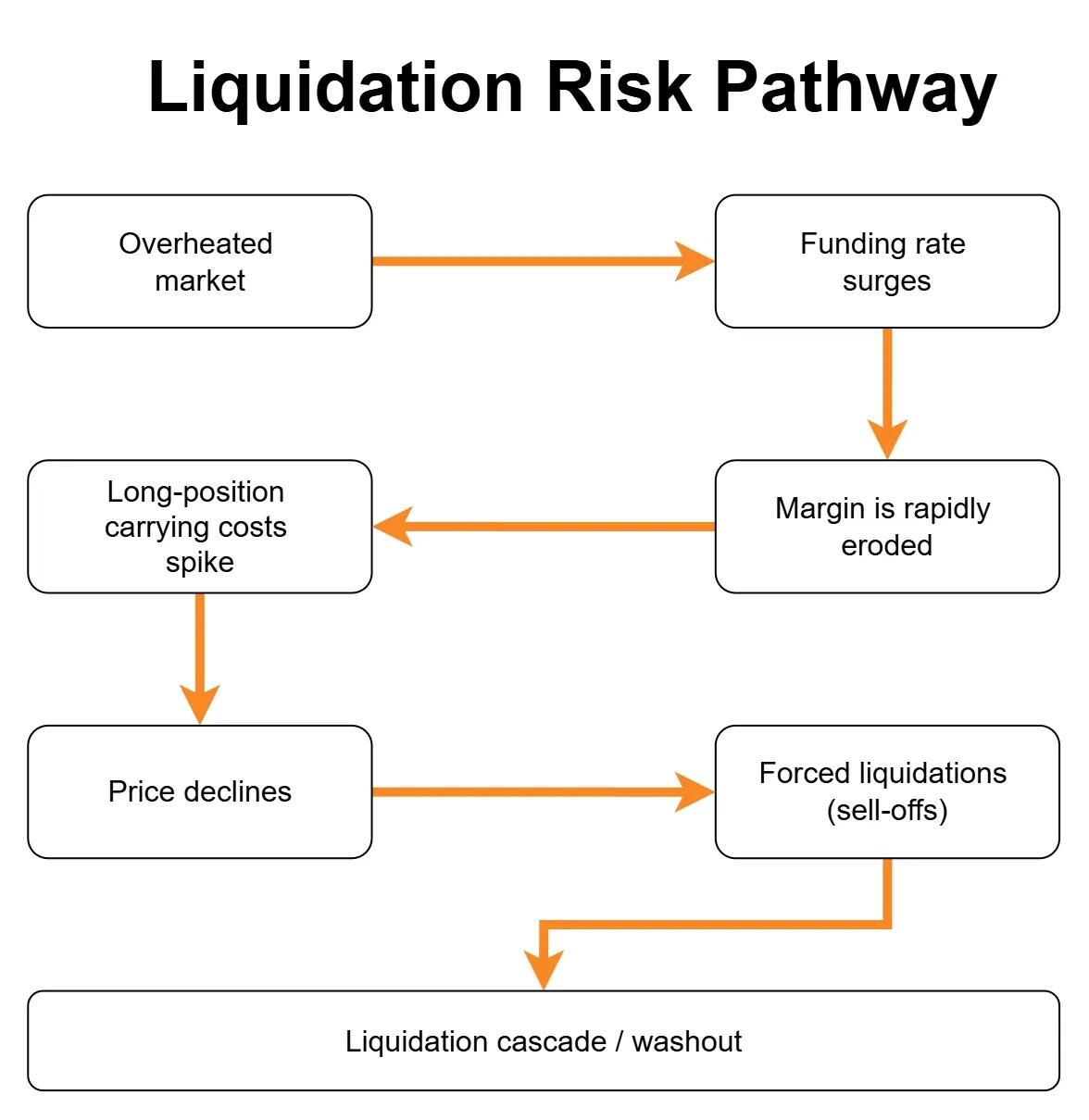

IV: Departures from the Norm — When Funding Moves Away from 0.01%

The 0.01% equilibrium characterizes markets under “normal weather.” Once sentiment turns extreme or stress rises, the supply–demand for leverage can temporarily overpower arbitrage, making the Premium Index the dominant driver of funding and pushing it far from the benchmark.

4.1 Bull-Market Euphoria (High Positive Funding)

● Mechanism. In a strong bull run, large numbers of retail and institutional traders pile into high-leverage long positions. This speculative fervor creates heavy buy pressure in perpetuals, lifting their prices well above spot.

● Outcome. The Premium Index becomes large and positive, far exceeding the 0.01% interest benchmark. The total funding rate can surge to 0.1% per funding interval (e.g., per 8-hour period) or higher, rendering the cost of holding longs extremely expensive.

4.2 Bear-Market Panic (Negative Funding)

● Mechanism. During crashes or panic selling, the dynamic reverses. Traders rush to short perpetuals to hedge risk or chase downside momentum, pushing perp prices well below spot.

● Outcome. The Premium Index turns large and negative. Funding flips to deeply negative, so shorts pay longs substantial fees. Functionally, this “rewards” those willing to catch the falling knife by going long perps amid extreme fear.

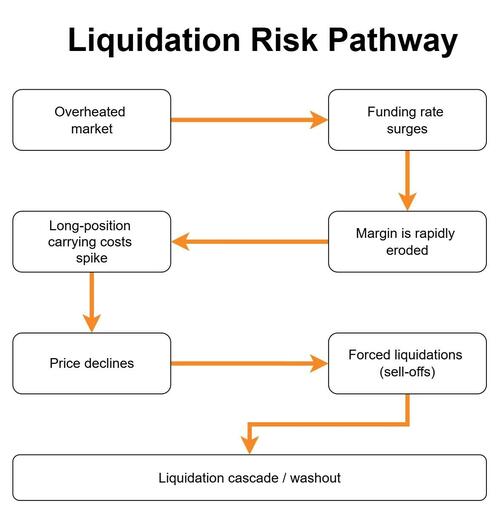

Schematic (caption). Cascading Liquidation Risk Pathway — “Long/Short” Position Fuel

4.3 The Role of the “Clamp” Mechanism

To prevent the funding rate from swinging excessively in extreme markets—thereby triggering liquidation cascades and undermining stability—exchanges impose upper and lower bounds on funding. This is the “clamp” (cap/floor) mechanism.

● Purpose. A key risk-control tool designed to ensure the funding rate itself does not become a catalyst for market breakdown.

● Implementation. The function clamp(x, min, max) restricts a variable x to the interval [min, max]. In the funding formula, clamp(Interest Rate − Premium Index, −0.05%, +0.05%) means that whatever value (Interest − Premium) produces, the term used in the formula is forcibly limited to between −0.05% and +0.05% per funding interval. (BTC is used here as an example; for many altcoins the bounds are wider than ±0.05%.)

In effect, the clamp represents the exchange’s trade-off between pure market incentives and system stability—a built-in circuit breaker (or, if you like, a measure of prudential restraint).

V: Strategic Implications for Traders and Investors

A rigorous grasp of the funding-rate mechanism is not mere theory; it can be converted into practical edge.

5.1 Funding Rate: A Real-Time Quantitative Gauge of Market Sentiment

The extent to which funding deviates from the 0.01% benchmark is among the purest, most real-time indicators of leverage sentiment.

● Persistently high positive funding: typically signals extreme greed, excessive leverage, and an overheated market.

● Persistently negative or deeply negative funding: typically signals extreme fear, short crowding, and capitulation.

5.2 Calculating the “Carry Cost” of Long-Term Positions

For investors intending to hold leveraged long positions over time, the 0.01% benchmark funding rate is a direct cost that must be quantified.

Cost calculation.

For a BTC long with 5× leverage on $100 of collateral

the funding payment per 8-hour interval is Funding per interval = 5×$100×0.01% = $0.05

That implies a daily cost of $0.05×3 = $0.15 and a simple annualized cost of $0.15×365 = $54.75

(This assumes funding is +0.01% and that longs pay shorts on that interval; if funding turns negative, the direction of payment reverses.)

Strategic considerations.

This carry erodes P&L for extended holds. The impact falls primarily on overnight/swing and longer-term positions. Intraday traders who flatten before the funding timestamp can avoid the charge entirely.

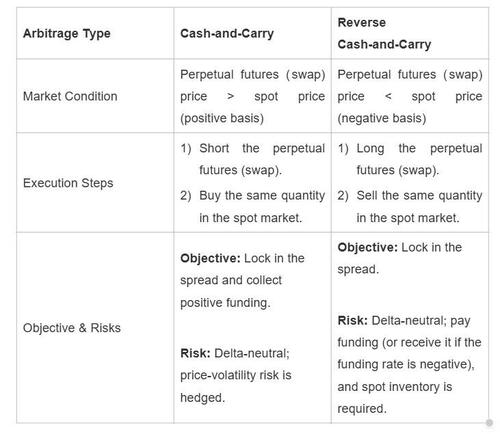

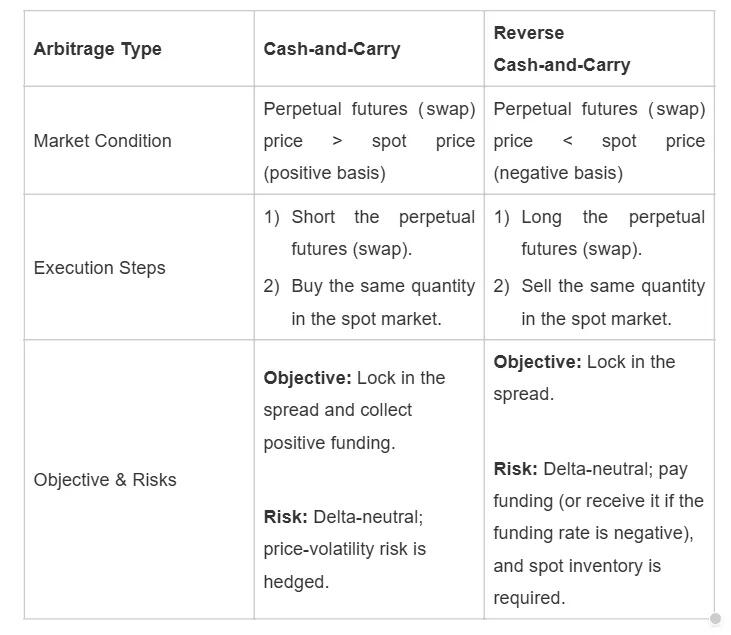

5.3 Cash-and-Carry (Basis) Arbitrage: A Delta-Neutral Way to Earn Funding

The funding-rate mechanism itself can be used to create a relatively low-risk yield strategy—namely the cash-and-carry (basis) arbitrage referenced earlier.

Execution.

1. Buy 1 BTC on the spot market;

2. Short 1 BTC notional in the perpetuals market.

The combined position is delta-neutral.

Profit source.

All P&L comes from the funding payments collected on the short-perp leg. In “normal” conditions, this approximates the 0.01% benchmark per funding interval (e.g., every 8 hours). In bull-market euphoria, the inflow can become materially larger.

5.4 Using Extreme Funding as a Contrarian Signal

Extremes revert. Extreme funding-rate levels can warn that a trend is overextended and that the probability of reversal is rising.

High-funding alert. When funding reaches historical highs, it implies longs are paying a steep carry for leverage and positioning is exceptionally crowded.

Negative-funding opportunities & case study. When funding turns deeply negative, it signals peak pessimism. A canonical example is May 19, 2021, when Bitcoin fell by nearly 40%, driving funding to deep negative readings not seen for months. For contrarian investors, this marked an extreme in panic and served as an early indicator of the subsequent bottom-and-rebound.

Conclusion

In this high-frequency arena, 0.01% is not an isolated rate parameter but the product of a dynamic balance between market efficiency and capital incentives.

It originates from the exchange-set benchmark rate and is maintained by an efficient arbitrage ecosystem, ultimately serving—under stress—as a valuable, real-time gauge of market sentiment.

It is not static; it is a harmonic produced by countless bots and human traders across billions of executions. A deep understanding of this mechanism is required coursework for any serious market participant—from first principles to proficiency. May we always approach the market with humility and respect.

Tyler Durden

Tue, 06/09/2026 - 19:15

via Associated Press

via Associated Press via YNet

via YNet Anadolu Agency

Anadolu Agency

via Reuter

via Reuter Five Tax Moves to Make Before December 31; Image Credit: Pexels

Five Tax Moves to Make Before December 31; Image Credit: Pexels

via social media

via social media

Recent comments