Apple, Microsoft Tumble On Abrupt Price Hikes Amid Chip-Crunch Contagion; Wall Street Responds

Summary:

- Memory Chip Crunch Crisis May Unleash Flood Of Consumer Device Companies Hiking Prices

- Microsoft Hikes Prices on Xbox

- Apple Hikes Prices on Macs and iPads

Wall Street Responds To Apple Hikes

Apple shares were down 5.5% in late-afternoon trading, on track for their largest intraday decline in 15 months, as the stock tumbled into correction territory. Shares are now down about 14% from their early June peak near $317.

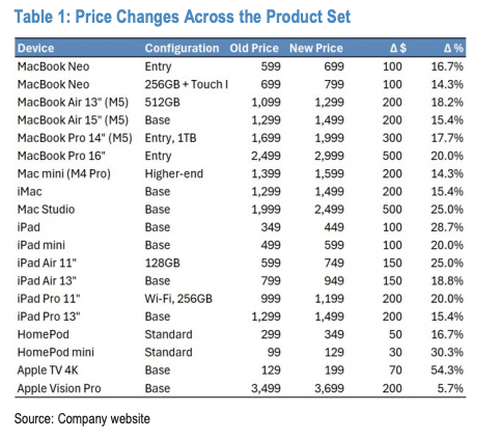

Investors appear spooked by Apple's rare overnight price hike, which boosted Mac computers by 15% to 20% and iPad prices by 15% to 25%.

An Apple spokesperson said that "the rapid expansion of AI data centers has created an extraordinary surge in demand for memory and storage" and that the company has "never seen a component price increase this much, this quickly."

JP Morgan equity research analyst Samik Chatterjee offered clients three takeaways from Apple's price hikes:

1. Higher-than-expected magnitude of price increases on announced SKUs could drive pressure on volume expectations for Macs and iPads, which have been able to deliver robust share gains recently with Apple delaying price increases relative to competition.

2. The magnitude of the price increases announced leads us to believe that our earlier expectations for a mid-single-digit increase in iPhone pricing in conjunction with an announced launch in September is likely to be too optimistic, although we still expect Apple to use additional levers to limit the magnitude of price increases on iPhones with greater volume and installed base implications relative to the price increase announced today

3. The company continues to balance market share, revenue growth, and profitability objectives, which should reassure investors around the resilience of earnings growth drivers.

Price Hikes:

Wedbush analyst Dan Ives noted, "While Apple is well known for using its huge memory and storage purchases as leverage to secure low prices, the current memory price increases have forced Apple's hand to raise prices, but we believe the company is in a strong position to increase prices without sacrificing hardware performance and risking increasing customer churn given the company's increasing focus on the higher-end consumer."

UBS analyst David Vogt also responded to the price hikes, telling clients that while no new iPhone price adjustments were announced on Thursday, there is reason to believe that "iPhone price increases are likely in the fall."

Vogt explained:

We expect iPhone price increases in the fall but likely flows in FY27 ests In conjunction with the expected launch of new iPhones in the fall, we expect Apple to lift effective prices anywhere from $50 to $100 along with possibly changing specs to offset the share rise in DRAM and NAND. For a typical $1,000 iPhone, memory was around $50 to $60 or a mid-single digit % of the BOM before the sharp rise in memory prices. With normalized/blended iPhone gross margins in the low 40s% range prior to recent memory dynamics, memory related BOM depending on the nature of LTAs could now be ~20% implying a broad based price increase approaching $100 could be an offset, hence we forecast 'Product' gross margin stability in FY27 in the 37-38% range.

Beyond Apple's price hikes on Thursday, Microsoft also raised prices on Xbox consoles, suggesting the memory-chip squeeze can not be contained by big tech consumer device companies. MSFT shares were down around 2.4% in late afternoon trading.

We expect more device makers heavily exposed to memory chip price volatility to adjust prices in the coming weeks and months, especially given the chip crunch will persist through year's end.

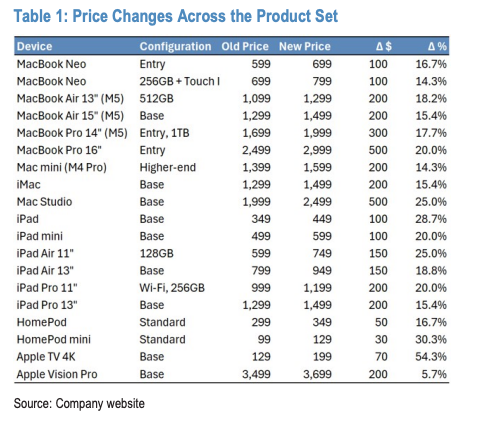

Apple Price Shock: Macs And iPads Jump $200 Or More As Memory Crisis Worsens

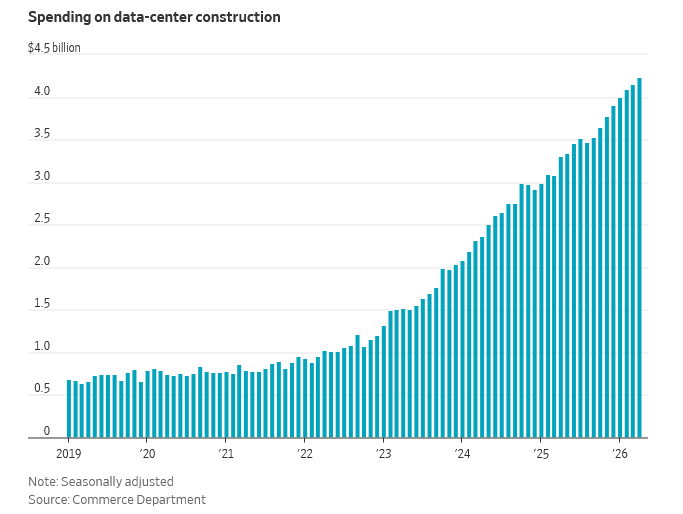

Readers were warned as early as late January to front-run the coming memory shortage by purchasing their favorite electronics, whether PCs, laptops, TVs, smartphones, or anything else dependent on high-end memory chips, as unprecedented data-center demand was already beginning to emerge.

Fast forward nearly five months, and just two weeks after Apple CEO Tim Cook warned that "price increases are unavoidable" for laptops and other devices, a Wall Street Journal report has confirmed that those hikes have now been passed along, potentially delivering sticker shock to customers.

Here's what happened earlier: The Apple Online Store briefly went down, and when it came back online, prices for Mac computers jumped 15% to 20%, while iPad prices increased 15% to 25%.

The company briefly took down its Apple Online Store early this morning as it typically does when announcing new products. When it came back online, the price tags for Mac computers rose roughly 15% to 20% and iPad prices rose 15% to 25%. Among the price increases, the base MacBook Air rose $200 to $1,299; the base MacBook Pro increased $300 to $1,999; the entry-level MacBook Neo increased $100 to $699. The iPad Air increased $150 to $749 and the iPad Pro increased $200 to $1,199. -WSJ

Vision Pro became even more unaffordable.

However, iPhone prices remained unchanged, but the company told the outlet in a statement that additional price hikes could be on the way.

"We have now reached a point where we need to begin raising prices," Apple said in the statement. "We have never seen a component price increase this much, this quickly."

An Apple spokesperson placed the blame on the "rapid expansion of AI data centers, which has created an extraordinary surge in demand for memory and storage," and this is why component prices surged.

Earlier this month, Cook told WSJ that price increases had become "unavoidable" because of higher component costs, adding, "There's less supply at a time when consumers want devices, and the memory guys are passing along huge price increases."

Apple has historically revealed price hikes with new launches of iPhones, iPads, and other devices, making this overnight price hike extraordinarily rare.

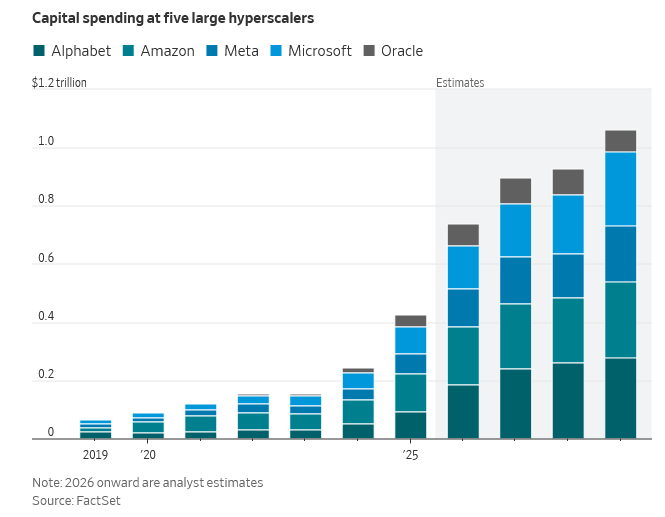

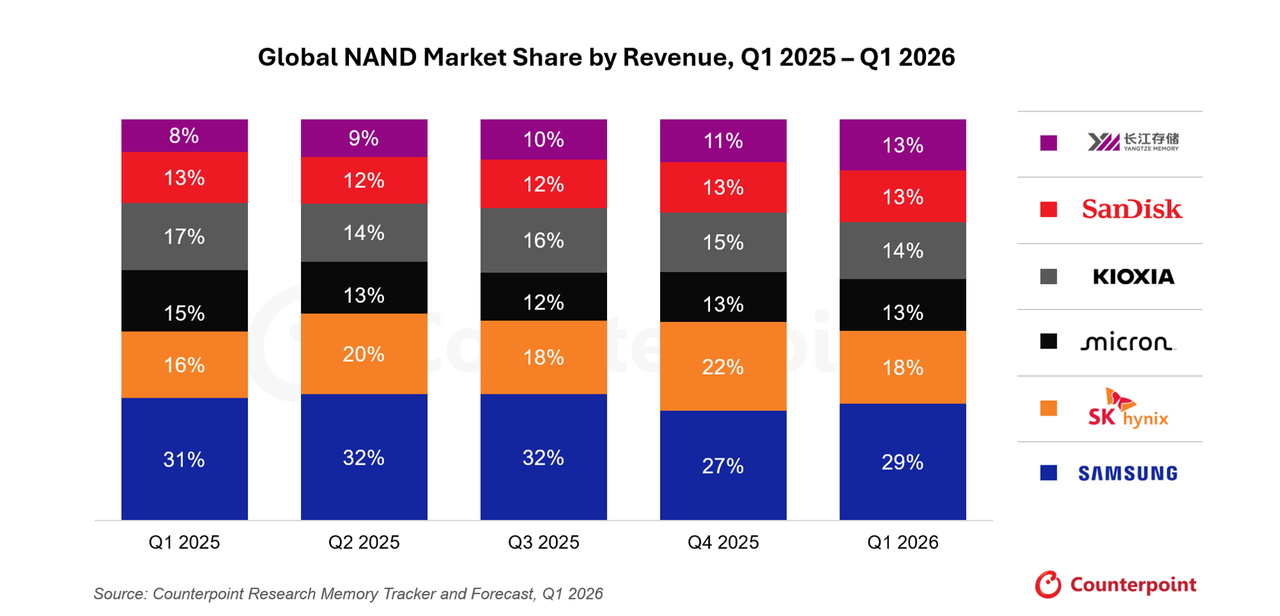

The high-end chip market is dominated by US-based Micron and South Korea's SK Hynix and Samsung, which have all seen massive demand for high-bandwidth memory from AI "hyperscalers" such as Google, Meta, and Amazon.

Apple's price hikes come hours after Micron delivered blowout quarterly earnings, touting gross profit margins that topped 80%. Shares soared nearly 18% in premarket trading.

Micron executives told investors that "tight conditions" will persist beyond 2027 and that only suggests further price hikes are coming not just for Apple but also for other major big tech firms that sell devices.

Micron Chief Business Officer Sumit Sadana said in a WSJ interview last night that "a couple of the customers who were being very aggressive with pricing at that time were not constructive," without naming Apple...

Sadana noted, "A lot of the industry investments got shut down in 2023 because of really poor pricing and really poor margins."

A recent Morgan Stanley note found that memory prices have climbed sixfold over the past year, with new manufacturing capacity likely to take years to build and ramp up.

The iPhone price hike may be unavoidable: JPMorgan analysts estimate DRAM and NAND could jump from roughly 10% to 15% of an iPhone's total component cost today to more than 45% by 2027.

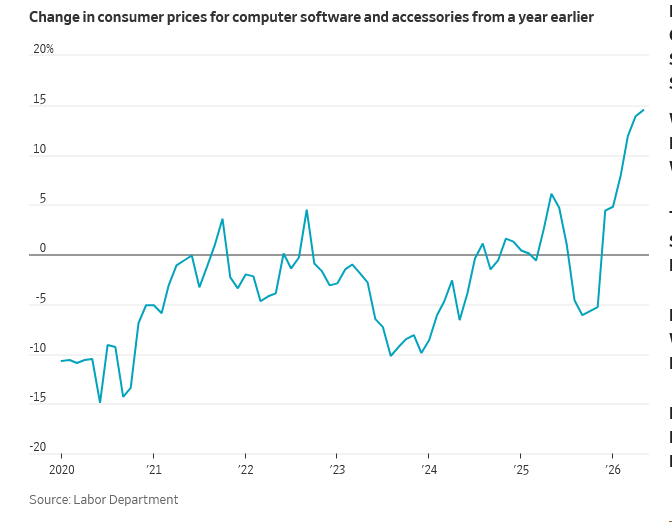

Memory price spikes are already showing up in the Producer Price Index for semiconductor and other electronic component manufacturing.

... and at what point does President Trump start raging at memory prices, just as his administration has successfully sent oil prices crashing by entering a diplomatic phase with Tehran to secure a permanent peace deal?

Tyler Durden

Thu, 06/25/2026 - 14:50

The Supreme Court in Washington on June 23, 2026. Madalina Kilroy/The Epoch Times

The Supreme Court in Washington on June 23, 2026. Madalina Kilroy/The Epoch Times A 12-year-old boy watches YouTube on his smartphone on March 27, 2026. Ulet Ifansasti/Getty Images

A 12-year-old boy watches YouTube on his smartphone on March 27, 2026. Ulet Ifansasti/Getty Images via Reuters

via Reuters

via Associated Press

via Associated Press

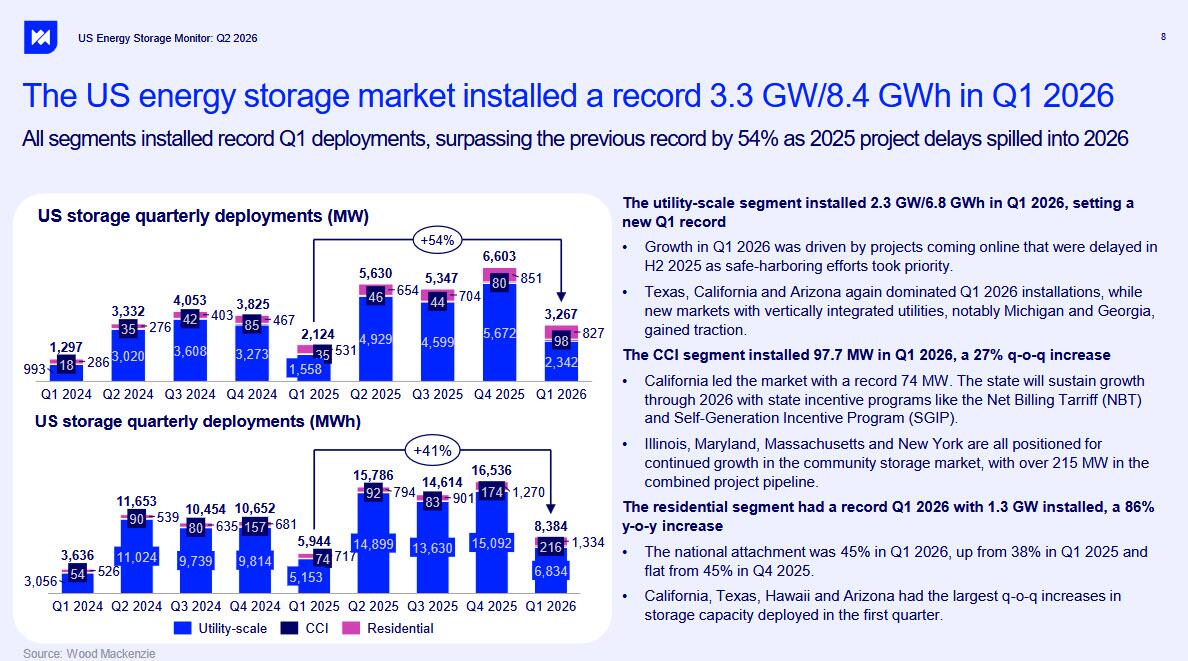

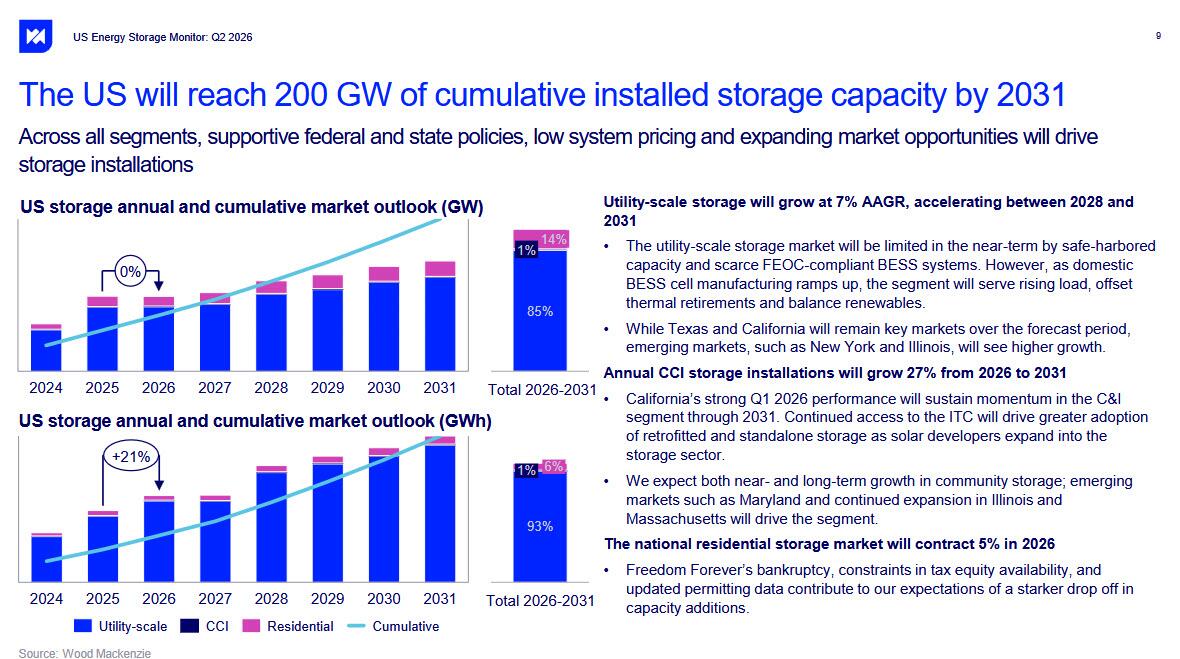

A battery energy storage facility. The United States added 3.3 GW/8.4 GWh of energy storage in the first quarter of 2026, according to a June report from Wood Mackenzie and the American Clean Power Association

A battery energy storage facility. The United States added 3.3 GW/8.4 GWh of energy storage in the first quarter of 2026, according to a June report from Wood Mackenzie and the American Clean Power Association

Recent comments