Over 20 US-Approved Ships Pass Through Hormuz, As Trump Eyes Jump-Starting Next Pakistan Peace Talks

-

CENTCOM: "During the first 24 hours, no ships made it past the U.S. blockade & 6 merchant vessels complied with direction from US forces to turn around to re-enter an Iranian port on the Gulf of Oman," it said. WSJ: 20 US-approved ships have passed, which have not visited Iranian ports.

-

Diplomacy is not yet dead, as Bloomberg reports Iran is mulling a short-term pause to shipments through Hormuz Strait. Trump tells NYP talks could happen again in two days in Pakistan.

-

Mediators are scrambling to put together another round of US-Iran talks in the coming days: Iran is reportedly offering a 5-year moratorium on nuclear program, while US demands 20.

-

Saudis are among those calling for an end to the US blockade of the Hormuz Strait, amid fears the Houthis could shut down Bab al-Mandeb strait. Chinese ship testing America's Hormuz blockade appears to U-turn. North Korea said to be negotiating tolls, safe passage with Tehran.

-

Hezbollah’s Secretary-General Naim Qassem rejects upcoming talks between the Lebanese government and Israel, which are set for 11am in Washington, DC on Tuesday.

Yes 60% · No 40%

View full market & trade on Polymarket

* * *

Over 20 US-Approved Ships Pass Through Hormuz: WSJWSJ writes by close of day Tuesday: "More than 20 commercial ships have passed through the Strait of Hormuz in the past 24 hours, according to two U.S. officials. While commercial traffic is still a fraction of what it was before the war, the flow of vessels is an improvement through a critical chokepoint."

These are of course vessels 'approved' and which transited via US military coordination - and this after earlier this week a couple of sanctioned or nonapproved vessels began making their way out before deciding to turn back. More per WSJ:

The ships that crossed the strait in the last 24 hours include cargo, container and tanker vessels going into and out of the Persian Gulf, one of the officials said. Some ships have traveled without their transponders on to minimize the risk of Iranian attacks. The threat of Iranian attacks and sea mines has deterred most vessels from trying to sail through the narrow waterway during the war.

It remains that ships which aren't under sanction, and which are not visiting Iran's ports can pass through the American-imposed blockade. But oil prices and markets remain unimpressed, as this is not happening at a fast enough rate, and given the presence of mines and the lingering Iranian drone and missile threat to maritime traffic, it's not as if the proverbial flood gates of tanker traffic will open up anytime soon.

CENTCOM Gives First Major Blockade Update, Trump Hints at TalksUS Central Command (CENTCOM) has put out its first major statement and update since the Trump-ordered US naval blockade of the Hormuz Strait went into effect.

"During the first 24 hours, no ships made it past the U.S. blockade and 6 merchant vessels complied with direction from U.S. forces to turn around to re-enter an Iranian port on the Gulf of Oman," it said.

IRAN TALKS COULD BE HAPPENING OVER NEXT TWO DAYS IN PAKISTAN: TRUMP TO NY POST

US WILL ALLOW TEMPORARY WAIVER OF SANCTIONS ON IRANIAN OIL ON THE SEA TO EXPIRE THIS WEEK

"The blockade is being enforced impartially against vessels of all nations entering or departing Iranian ports and coastal areas, including all Iranian ports on the Arabian Gulf and Gulf of Oman," it added, noting that over 10,000 American military personnel are currently involved in the blockade mission. The regional US command center also published an infographic confirming which types of the various navy warships are deployed.

More than 10,000 U.S. Sailors, Marines, and Airmen along with over a dozen warships and dozens of aircraft are executing the mission to blockade ships entering and departing Iranian ports. During the first 24 hours, no ships made it past the U.S. blockade and 6 merchant vessels… pic.twitter.com/dpWAAknzQp

— U.S. Central Command (@CENTCOM) April 14, 2026

However, RT's correspondent is on the ground and has given a contrasting report, running up against US claims:

South Korea said to be Negotiating Tolls, Hormuz Passage with IranThere is NO naval blockade of Hormuz Strait — RT Exclusive

— RT (@RT_com) April 14, 2026

Local reporter Mojtaba Biglari shows footage of 'completely secure' Strait

Countries hostile to Iran still not allowed to pass

'Trump granted them permission in a parallel world' pic.twitter.com/nvvAxLZPZk

Washington has been urging countries with stranded tankers near Iran not to pay money to Tehran to allow them through the blocked Strait of Hormuz. Various tanker and maritime industry firms have also been vocally against this.

However, amid a 2-week US-Iran ceasefire, South Korea is reportedly negotiating with Iran the pass ships through Hormuz as a temporary solution. Iran state-linked Fars reports, "The South Korean Ship Owners' Association has also proposed to pay tolls for passing through the Strait of Hormuz to Iran as a short-term solution."

As yet, there's been no confirmation of this from Seoul officials, and at the start of the month they were actively denying earlier reports that South Korea was willing to pay tolls to get its over couple dozen stranded ships through. If it happens, there would likely follow condemnation from the White House over this 'compromise' from a US ally.

Iran Could Pause Hormuz Shipping, As Chinese Tanker U-TurnsBloomberg says Tuesday in a fresh report that "Iran is considering a short-term pause to shipments through the Strait of Hormuz to avoid testing a US blockade and scuppering a fresh round of peace talks, according to a person familiar with the Tehran’s deliberations."

"The potential pause reflects a desire to avoid immediate escalation at a sensitive diplomatic juncture as Washington and Tehran sort logistics for another face-to-face meeting, the person said, asking not to be identified as the deliberations are private," continues Bloomberg. It adds, "Holding back maritime activity for several days is seen as one possible, pragmatic step to prevent an incident that could undermine the fragile efforts to revive discussions, people familiar with the matter said."

This would be seen as short-term de-escalation, and suggests that Tehran indeed still has the desire of taking a hopeful, pragmatic approach - rather than returning the all out war by the close of the temporary ceasefire. No one is willing to completely shut the door on all diplomacy, and the bombs have been silent across the Gulf and in Iran and Israel. Per latest emerging reports:

The Nasdaq 100 looked set to notch its longest streak of gains since 2021 as optimism that the US and Iran are considering another round of peace talks pushed oil lower and lifted stocks globally.

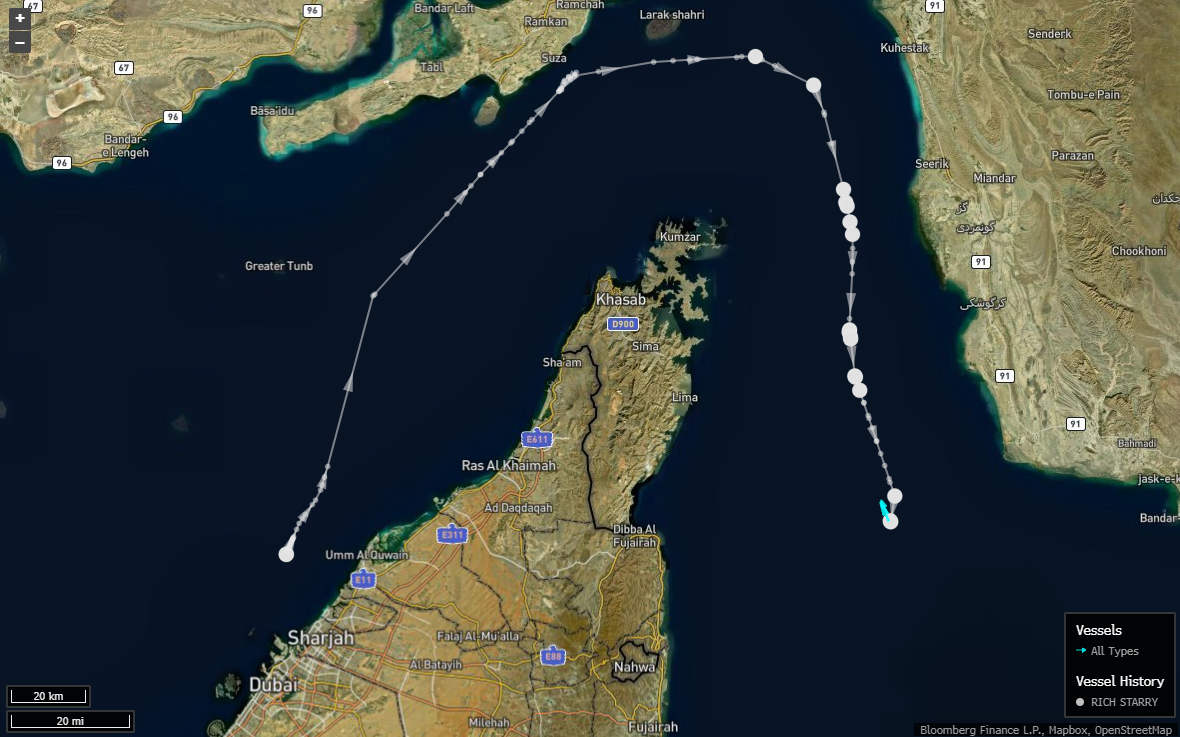

Chinese ship testing America's Hormuz blockade appears to U-turn: Rich Starry was blacklisted by Washington in 2023 for helping Tehran evade energy sanctions.

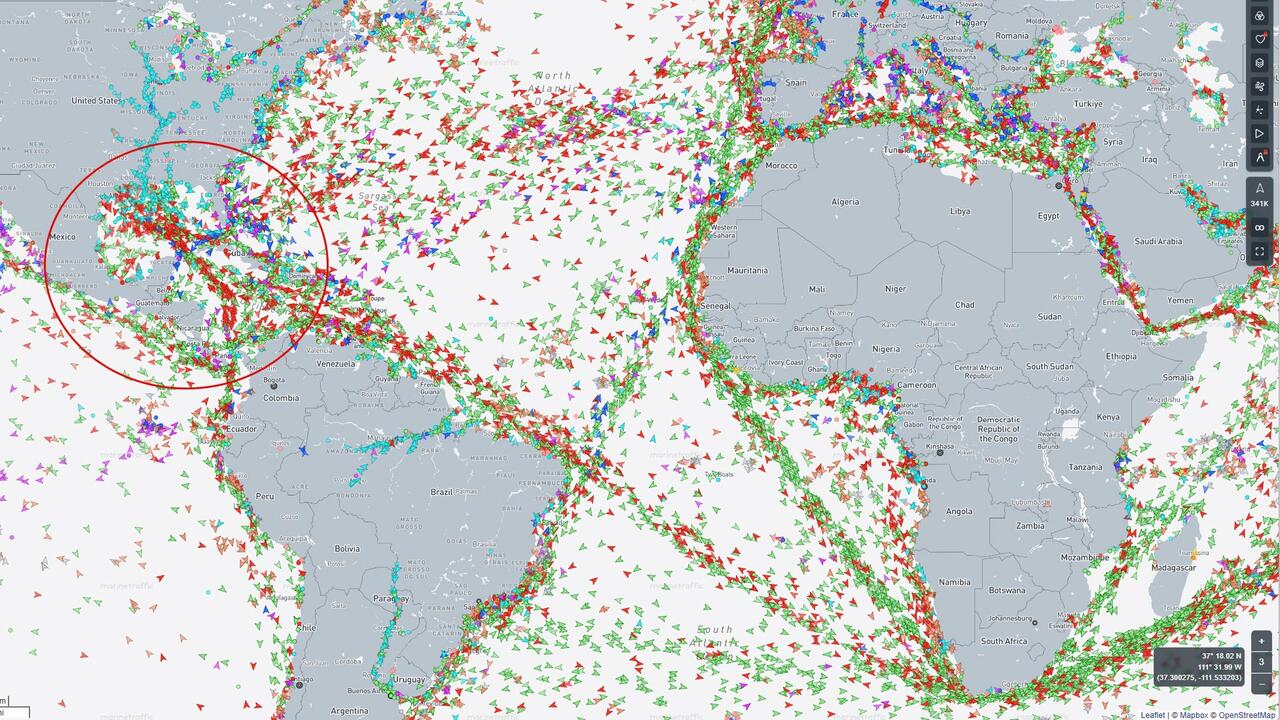

More tracking data via MarineTraffic:

5-Years vs. 20-Year Nuclear MoratoriumTwo tankers turn away from Strait of Hormuz after US blockade begins

— MarineTraffic (@MarineTraffic) April 13, 2026

At least two tankers reversed course near the Strait of Hormuz shortly after the start of the US blockade, highlighting the immediate impact on vessel movements. According to #MarineTraffic data, the 188-metre… pic.twitter.com/dRNi7yEgJI

More info and color has been added in the wake of failed talks between the US and Iran in Pakistan, per The New York Times citing officials from both countries. Iran signaled Monday it would halt uranium enrichment for up to five years. The Trump administration rejected the offer, according to two senior Iranian officials and one US official who spoke to the Times.

The US position, shaped in part by Vice President JD Vance, calls for a roughly 20-year suspension. Vance has argued such a timeframe is necessary to permanently limit Iran's nuclear capabilities. "The Iranians, in a formal response sent on Monday, said they would agree to up to five years, according to two senior Iranian officials and one U.S. official. Trump has rejected that offer, the U.S. official said," writes NY Times.

"The official said the U.S. has also asked Iran to remove highly enriched uranium from the country, and the Iranians have insisted the fuel stays inside Iran. But they have offered to dilute it significantly, so that it could not be used to produce a nuclear weapon," the report adds.

Sides Could Return to Islamabad for TalksThis behind the scenes back-and-forth suggests that the mediated talks might not be entirely over, also as the clock ticks away on the initial 2-week ceasefire, now a week in. US and Iranian negotiating teams plan to return to Pakistan later this week to resume talks aimed at ending the Gulf war, Pakistani and Iranian officials said Tuesday, as cited in Reuters. Other reports say the talks could be hosted in another venue.

However, US officials have not confirmed the plans, and the reality is that in Islamabad the two sides demands were very far apart, having reportedly finally collapsed on the nuclear issue.

Israel-Lebanon talks are taking a separate track, set to begin in Washington Tuesday, but Hezbollah has rejected this process - with only the Lebanese government represented.

⚡️Israel firing flares in the sky of Tyre, Lebanon pic.twitter.com/EPOhKAlXJ5

— War Monitor (@WarMonitors) April 13, 2026

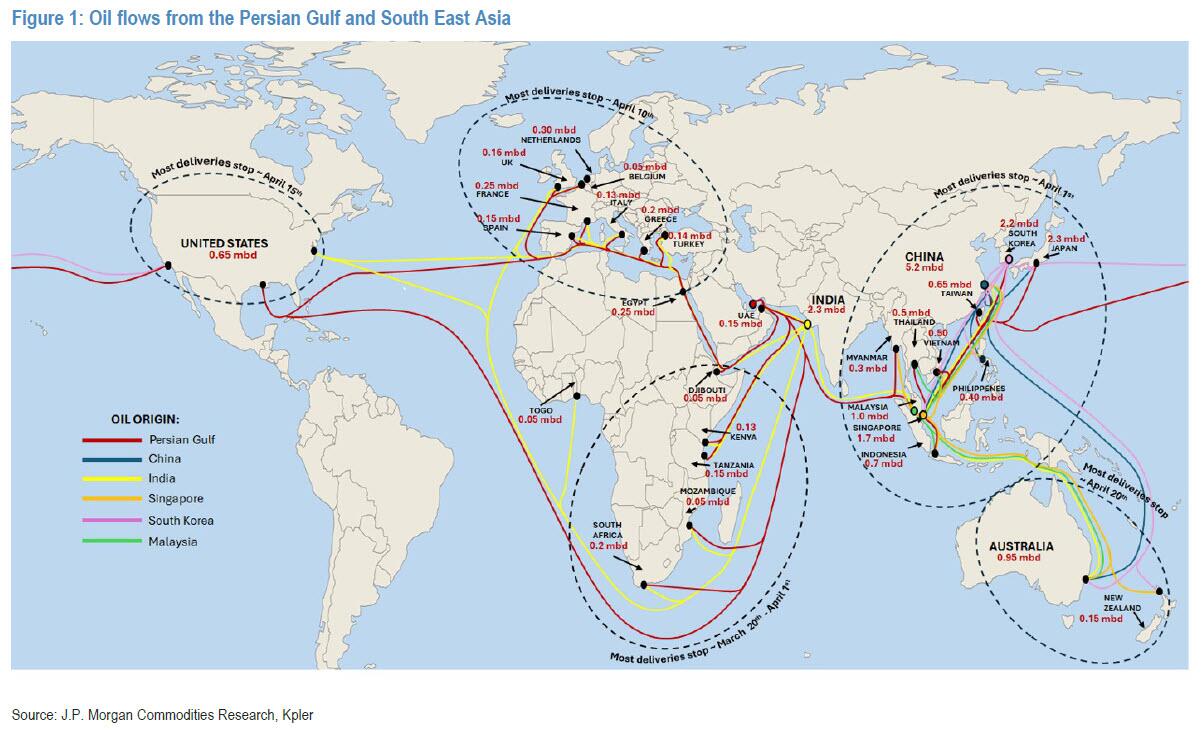

France's President Emmanuel Macron is among those calling on Washington and Tehran to urgently resume negotiations to end the war, and to reopen the Strait of Hormuz "without controls or tolls, as soon as possible." Iran is reportedly charging steep tolls to let a handful of 'friendly' countries' vessels through - a situation which President Trump has warned against.

Saudis Push Trump To Call Off Hormuz BlockadeThe NY Times has on Tuesday highlighted that "Questions over the status of the U.S. military blockade in the Strait of Hormuz persisted on Tuesday, as tracking data showed that several ships had passed through the waterway, including some that had departed from Iran."

The Wall Street Journal reported Monday evening that the Kingdom of Saudi Arabia is urging the Trump administration to reverse its newly implemented blockade of Iranian-linked shipping in the Strait of Hormuz, on immediate fears that Iranian escalation could halt Red Sea traffic. On Sunday, a senior adviser to Iranian Supreme Leader Mojtaba Khamenei said Iran has "large, untouched levers" to respond to such a blockade.

Arab officials who spoke to the Journal said Iran could retaliate by shutting down the Bab al-Mandeb, a 20-mile-wide, 70-mile-long choke point linking the Red Sea to the Gulf of Aden and the Indian Ocean. Iran could do so by leveraging the Houthis, the political and military organization that controls much of Yemen.

Saudi Arabia recently has been able to get its oil exports back up to their prewar level of around seven million barrels a day despite the blockage in the strategic strait by piping its crude across the desert to the Red Sea. Those supplies would be at risk if the Red Sea’s exit route were closed as well. -- WSJ

NEW: US blockade on Iranian ports begins, but tanker traffic through Hormuz continues uninterrupted, with vessels including Peace Gulf, Murlikishan, and Rich Starry, including sanctioned ships, still transiting as long as they are not calling at Iranian ports.

— Levent Kemal (@leventkemaI) April 14, 2026

- Reuters pic.twitter.com/K76oyJbZOv

"If Iran does want to shut down Bab al-Mandeb, the Houthis are the obvious partner to do it, and their response to the Gaza conflict demonstrates that they have the capacity to do it," Adam Baron, an expert on Yemen at the New America policy institute, told the Journal.

More Geopolitical Latestvia Newsquawk...

- The next round of talks between the United States and Iran could take place this week or early next week, according to an Iranian embassy official in Pakistan.

- Pakistan’s Foreign Ministry said it has offered to host a second round of U.S.–Iran negotiations, but no date or time has been set.

- Pakistani journalist Mallick said, "While Islamabad has offered to host the next round of in person talks between US and Iran, which could be held at a working level, to my understanding, date and venue for the next round has not been finalised as yet".

- The United States and Iran are discussing another round of face-to-face talks to secure a longer-term ceasefire after Islamabad negotiations ended without a deal.

- Officials aim to meet again before the two-week ceasefire expires next week, according to Clash report.

- The Associated Press reported that a second round of talks is likely and could take place on Thursday.

- U.S. Vice President JD Vance said progress was made in talks with Iran and stated that things did not go wrong.

- Vance said Iran moved in the U.S. direction but not far enough.

- Vance said the ball is in Iran’s court and that U.S. red lines were clearly communicated.

- The United States and Iran left the door open to further dialogue after tense Islamabad talks.

- A source said the sides came "very close" to an agreement and were "80% there" before hitting unresolved issues.

- Iranian President Masoud Pezeshkian told French President Emmanuel Macron in a Monday phone call that Iran will negotiate only under international law.

- Pezeshkian said unreasonable U.S. demands blocked an agreement in weekend talks.

- He said a lack of U.S. goodwill and maximalist positions prevented finalizing a deal in Islamabad, according to IRNA.

- Pezeshkian said diplomacy remains the preferred path to resolve disputes.

- An Iranian National Security Committee spokesman said the end of the truce should not lead to its extension, according to Al Mayadeen.

- The U.S. aircraft carrier USS George H.W. Bush is sailing off the coast of Africa toward the Middle East to join Operation Epic Fury, according to two U.S. officials cited by The Wall Street Journal.

- Saudi Arabia is pressing the United States to drop its Hormuz blockade.

- Gulf energy exporters warn Iran could escalate by closing the Bab al-Mandeb, according to The Wall Street Journal.

- Alarms sounded in the Galilee Panhandle over concerns of potential UAV infiltration.

- A Lebanese source said, "The official mandate of Lebanon's ambassador in Washington is limited to pursuing a ceasefire with Israel", according to Al Jazeera.

- Switzerland is ready to support diplomatic initiatives between the United States and Iran.

- Russian Foreign Minister Sergey Lavrov told Iranian Foreign Minister Abbas Araghchi that preventing further fighting is critical.

- Lavrov said Moscow is on high alert to assist in a settlement.

- Araghchi warned of dangerous consequences from U.S. actions.

- U.S. Secretary of State Marco Rubio will host Israeli and Lebanese ambassadors for talks on Tuesday.

- The talks aim to secure a ceasefire, Hezbollah disarmament, and a peace agreement, according to Axios.

- A meeting between the Israeli and Lebanese ambassadors will take place Tuesday at 18:00 EDT / 23:00 BST, according to Al Jazeera citing Israeli Channel 15.

- Chinese President Xi Jinping issued four proposals to maintain peace in the Middle East, according to Chinese media.

- UK Deputy Prime Minister David Lammy met with U.S. Vice President JD Vance in Washington.

- Lammy urged that the Iran ceasefire hold and emphasized the importance of free shipping through the Strait of Hormuz.

* * *

District Judge James Boasberg, chief judge of the District Court for the District of Columbia, stands for a portrait at E. Barrett Prettyman Federal Courthouse in Washington on March 16, 2023. Carolyn Van Houten/The Washington Post via AP

District Judge James Boasberg, chief judge of the District Court for the District of Columbia, stands for a portrait at E. Barrett Prettyman Federal Courthouse in Washington on March 16, 2023. Carolyn Van Houten/The Washington Post via AP

USS George H.W. Bush (CVN-77) transits the Atlantic Ocean, Feb. 15, 2026. US Navy photo

USS George H.W. Bush (CVN-77) transits the Atlantic Ocean, Feb. 15, 2026. US Navy photo

Source: Alma

Source: Alma Illustration via WIRED

Illustration via WIRED

Recent comments