"Heavy Casualties" After Massive Twin Quakes Rock Venezuela, Topple Buildings; "International Response May Be Needed"

Twin earthquakes rocked Venezuela on Wednesday evening, collapsing entire apartment buildings across Caracas and leaving behind scenes of widespread devastation.

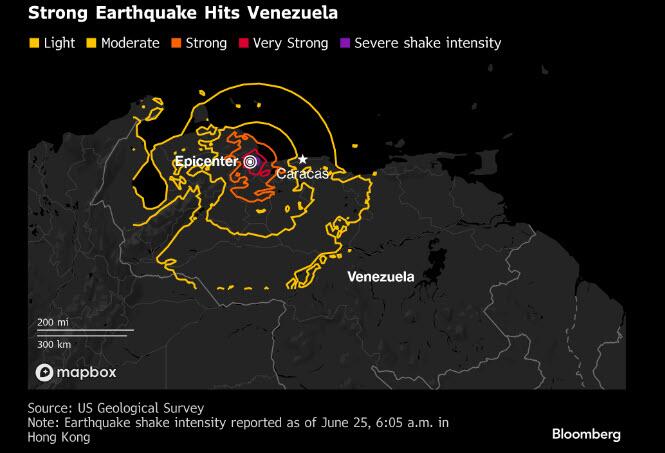

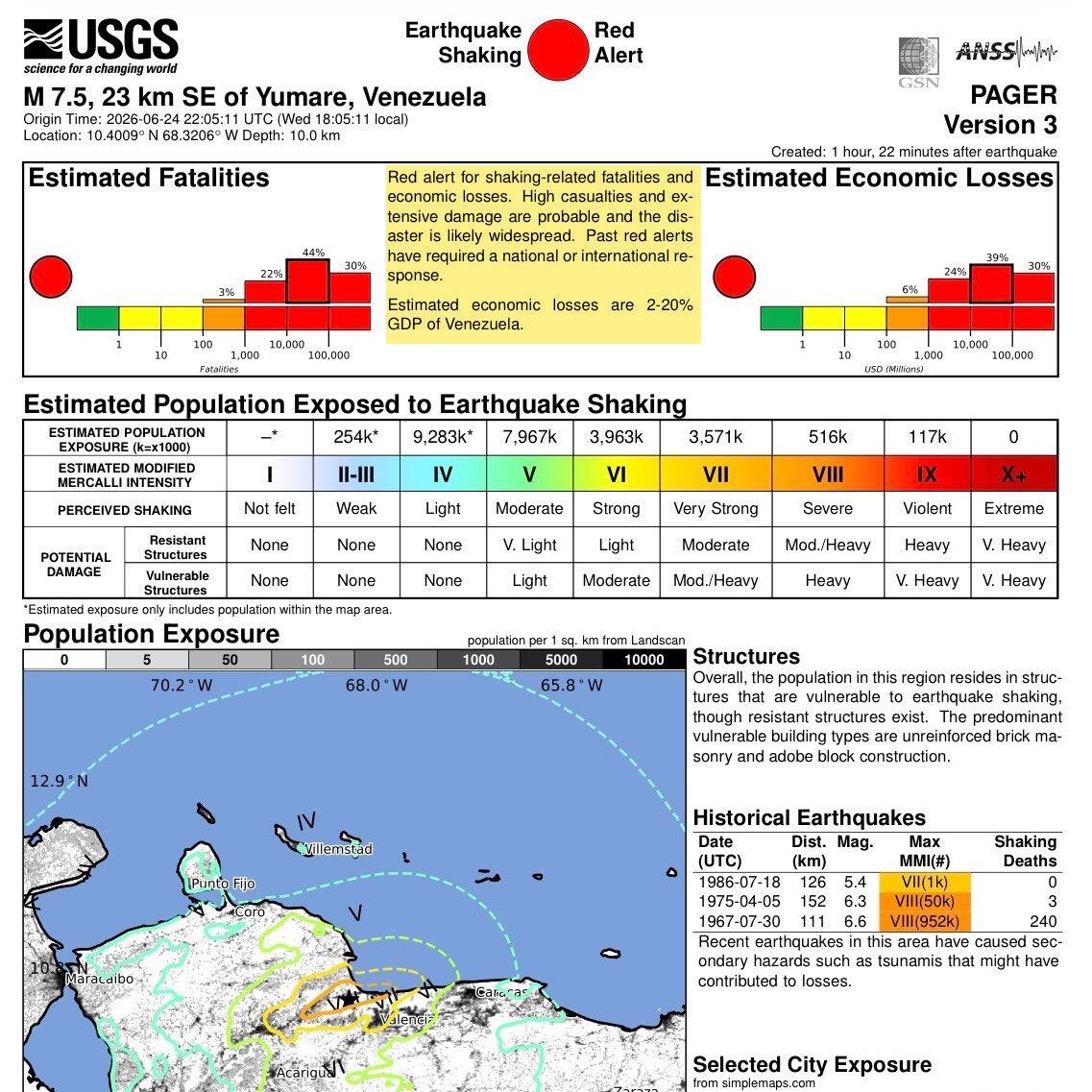

The USGS said the first quake registered a magnitude of 7.1, with an epicenter near Morón, about 104 miles west of Caracas, at a depth of 8 miles. One minute later, a similarly massive magnitude 7.5 quake struck nearby, roughly 10 miles southwest of Morón, at a depth of 6 miles. Remarkably, the dual quake was followed almost immediately across the world by a 6.9 magnitude temblor in northern Japan, which rattled buildings in Tokyo.

USGS issued a red-alert mass-casualty warning due to the combination of shallow depth, heavy population exposure, vulnerable buildings, and estimated losses large enough to require an international response.

"Red alert for shaking-related fatalities and economic losses. High casualties and extensive damage are probable and the disaster is likely widespread. Past red alerts have required a national or international response," USGS said, adding, "Estimated economic losses are 2-20% GDP of Venezuela."

In the Palos Grandes neighborhood in eastern Caracas, residents tried frantically to rescue people trapped under the debris of collapsed buildings, Bloomberg reports. Terrified families remained in the streets as the capital was hit by aftershocks. Venezuelan migrants in Colombia and elsewhere sought to reach relatives, but cellphone coverage was down in swathes of the country.

The early footage emerging from the devastation is dramatic:

Devastating scenes emerge from La Guaira, Venezuela, following a powerful earthquake that struck the region. pic.twitter.com/fBMIDWuabP

— Breaking911 (@Breaking911) June 24, 2026

Fishermen in the sea off the coast of La Guaira record the moments after the earthquake with dust covering large parts of the coast as a result of building collapses#Venezuela pic.twitter.com/D8KNwLkLDf

— CNW (@ConflictsW) June 25, 2026

Local news showed significant damage to the capital's airport, with parts of the roof collapsing and throwing up thick clouds of gray dust.

Passengers panic and run for cover at Simón Bolívar International Airport in Maiquetía, Venezuela, as the terminal shakes and power flickers, resulting from a massive 7.5 magnitude earthquake off the coast of Caracas. pic.twitter.com/uWN4ZqFjOZ

— OSINTdefender (@sentdefender) June 24, 2026

Interior Minister Diosdado Cabello said in a national address that some houses and buildings have collapsed. He warned residents to stay outside due to the risk from aftershocks. Cabello said that states including Trujillo, Yaracuy, Carabobo, Miranda, Aragua and La Guaira were also affected.

Immense damage seen to buildings across Venezuela’s capital of Caracas, following what now appears to have been a “double-event” 7.2 and 7.5 magnitude earthquake back-to-back near the coast in Northern Venezuela, according to the U.S. Geological Survey (USGS). pic.twitter.com/XoG2jSJMf2

— OSINTdefender (@sentdefender) June 24, 2026

Authorities haven't yet published estimates of the number of dead or injured. There were no immediate reports of damage to the nation's oil infrastructure. Some older residents said the event brought back memories of the massive 1967 earthquake which left hundreds dead.

Pretty rare earthquake activity tonight on Earth.

— Noah Bergren (@NbergWX) June 25, 2026

Both of these things happening within 2 hours of each other:

1 in 1,000 to 1,200 years

• A “doublet” earthquake in Venezuela (two quakes of similar magnitude in the exact same spot)

• A totally separate 6.9+ quake…

The closest historical comparison to the twin quakes this evening likely dates back to the March 26, 1812, Caracas earthquake sequence, which was described as twin destructive shocks within 30 minutes. That quake led to an estimated death toll of 15,000 to 20,000, while a USGS historical summary says it may have claimed about 30,000 lives.

BREAKING: Multiple structures have reportedly collapsed in Caracas, Venezuela, following a powerful earthquake that struck the region. pic.twitter.com/9KSN4srhwB

— Breaking911 (@Breaking911) June 24, 2026

Quake activity elsewhere...

That is not good. pic.twitter.com/3u8MsW2blB

— SpaceWeatherNews (@SunWeatherMan) June 24, 2026

And Japan.

Second big quake today pic.twitter.com/wWKsq0Ioqx

— SpaceWeatherNews (@SunWeatherMan) June 24, 2026

There were no immediate reports of damage to Venezuela's oil facilities, according to people familiar with the situation. The country's refining hub in Paraguaná, 225 kilometers (140 miles) west of the epicenter, continued operations as usual. Work at the port of Jose complex and at the Puerto La Cruz refinery was unaffected.

The disaster will further strain the nation's crisis-hit economy. The country is reeling from one of the world's fastest inflation rates and rolling power outages. As such, the quake could open a window for President Trump to offer emergency aid and logistical support, potentially creating the first step toward a broader US-backed reconstruction effort in Venezuela.

*Developing...

Tyler Durden Wed, 06/24/2026 - 20:24

Image via Forbes & Caspian post

Image via Forbes & Caspian post

via UN News

via UN News

Microsoft co-founder Bill Gates (C) in Washington, on June 10, 2026. Kent Nishimura/AFP via Getty Images

Microsoft co-founder Bill Gates (C) in Washington, on June 10, 2026. Kent Nishimura/AFP via Getty Images

US President Donald Trump looks on as he stands in front of the VC-25B aircraft gifted by Qatar that will be used as Air Force One, at Joint Base Andrews, Maryland, June 19, 2026. ELIZABETH FRANTZ / REUTERS

US President Donald Trump looks on as he stands in front of the VC-25B aircraft gifted by Qatar that will be used as Air Force One, at Joint Base Andrews, Maryland, June 19, 2026. ELIZABETH FRANTZ / REUTERS Technicians mounting the wings onto the X-65 experimental drone.

Technicians mounting the wings onto the X-65 experimental drone. An artist’s render of the X-65 drone. Source:

An artist’s render of the X-65 drone. Source:  Treasury Secretary Scott Bessent at the Economic Club of New York, on June 23. Photographer: Krisanne Johnson/Bloomberg

Treasury Secretary Scott Bessent at the Economic Club of New York, on June 23. Photographer: Krisanne Johnson/Bloomberg

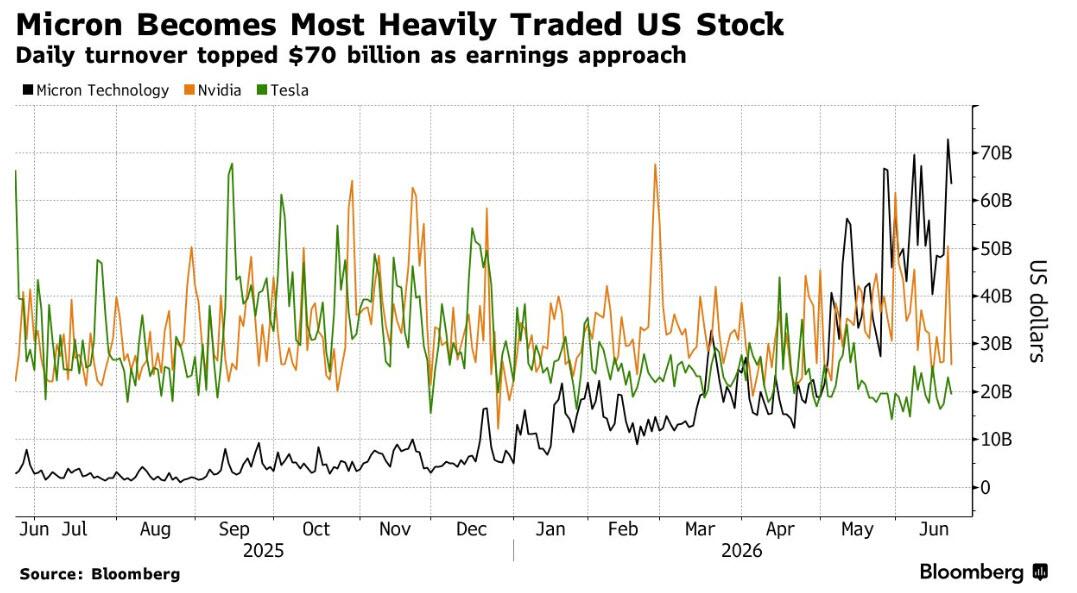

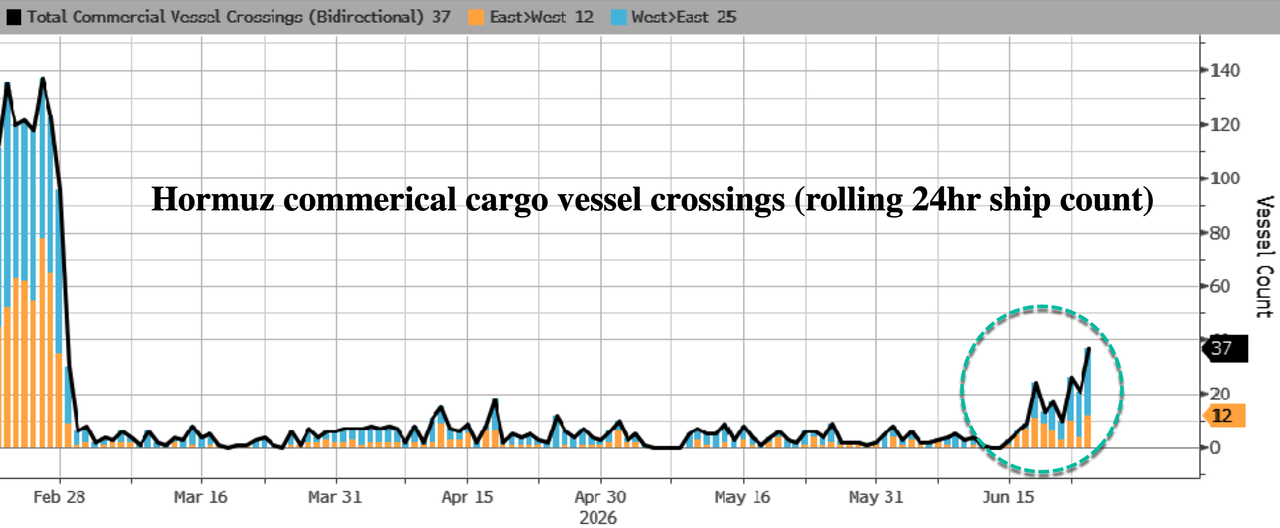

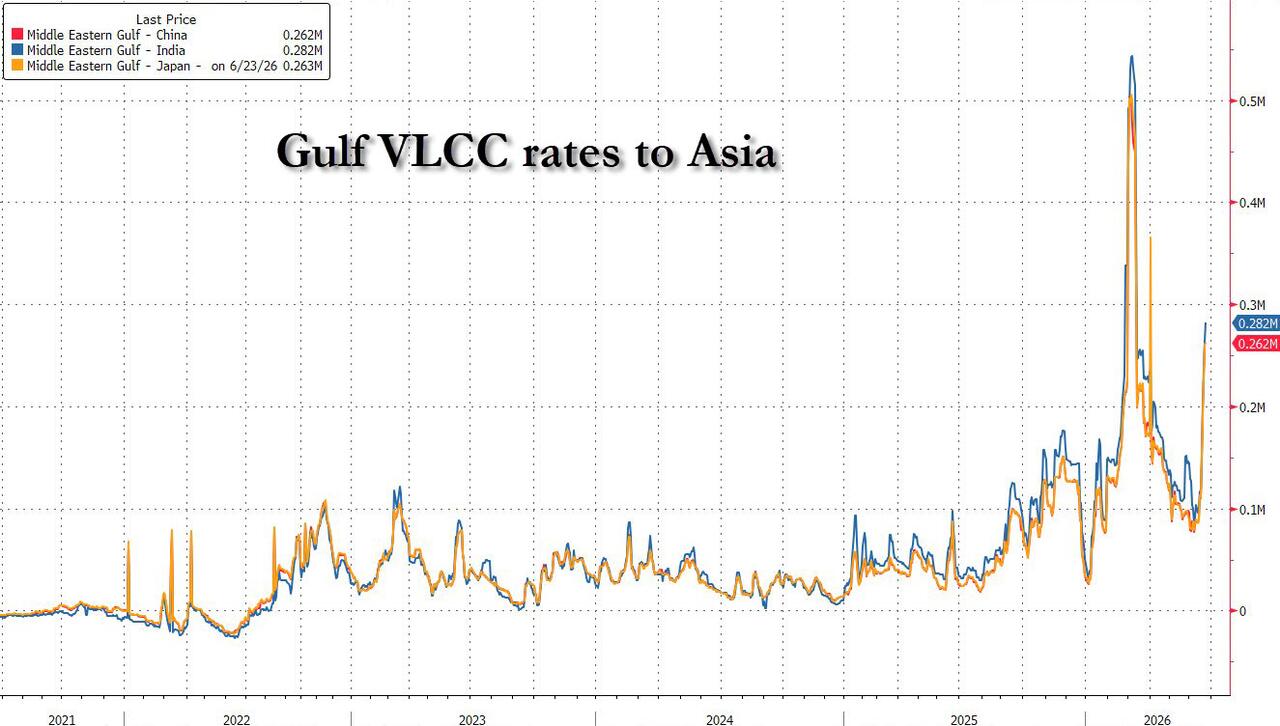

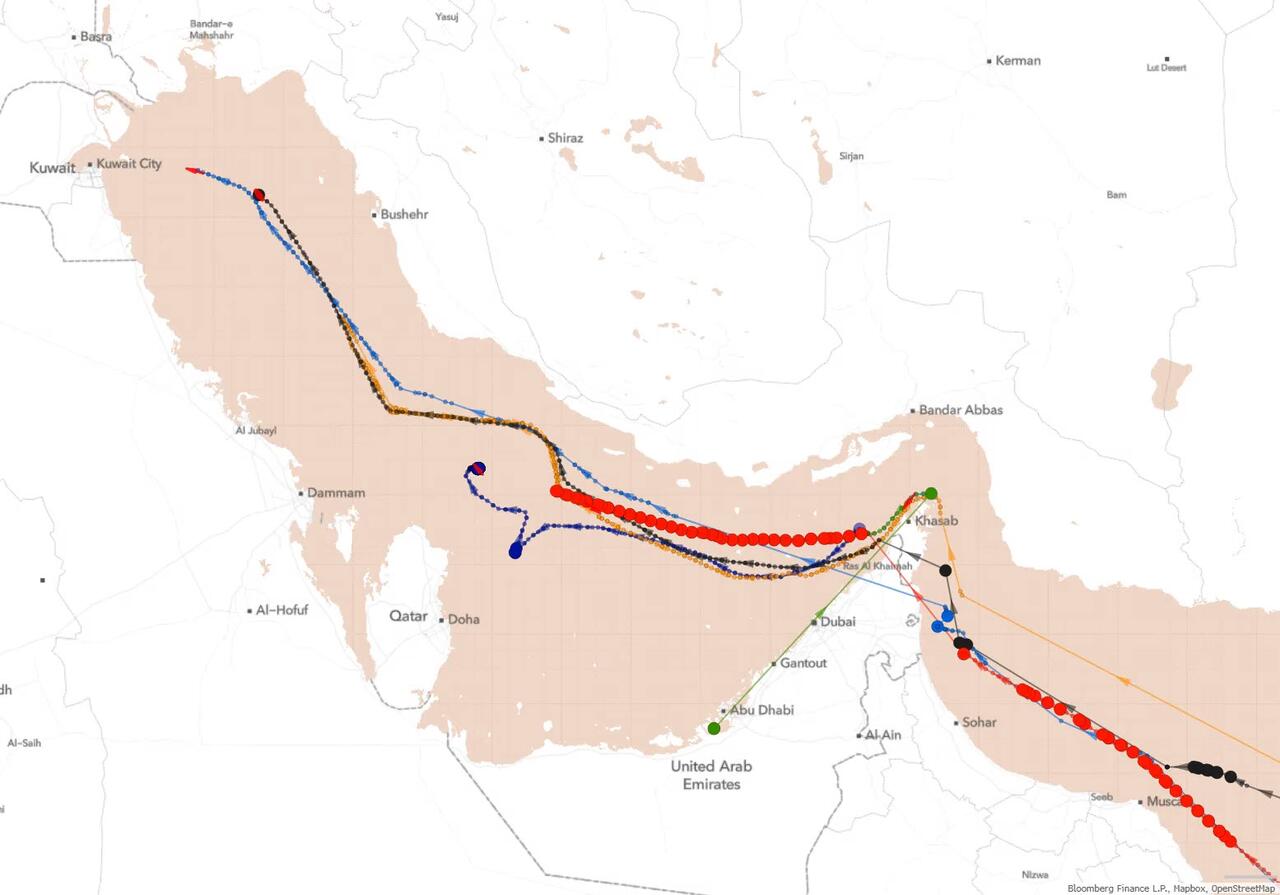

At least seven very large crude carriers have sailed into the Persian Gulf since the US and Iran agreed to an interim ceasefire deal late last week.Source: Bloomberg

At least seven very large crude carriers have sailed into the Persian Gulf since the US and Iran agreed to an interim ceasefire deal late last week.Source: Bloomberg

Iranian state media

Iranian state media

Recent comments