Cerebras Plunges To Post-IPO Low On Striking Admission: The US Has A Dire Shortage Of Operating Data Centers

Just over two years ago, we first penned our views on "The Next AI Trade", which looked beyond the hyperscalers and the data centers supporting the AI revolution, and instead focused on the energy and logistical needs that would be so very critical in allowing the US to dominate China in the existential race to first reach Artificial General Intelligence (which many have dubbed the next nuclear arms race due to its profound civilizational implications). It was here that we defined the "Power Up America" basket as the next AI trade.

Yet as one can see in the chart below, after outperforming the AI Data center and the TMT AI baskets in 2024 and much of 2025, the Power Up America trade has lagged and clearly underperformed, as some investors have started to express doubt that the US would ever be able to "grow" into its massive AI computing needs... with dire consequences for record AI capex budgets, something the market has yet to grasp.

And unfortunately, with every passing day, the outlook for the US AI revolution looks increasingly more dim.

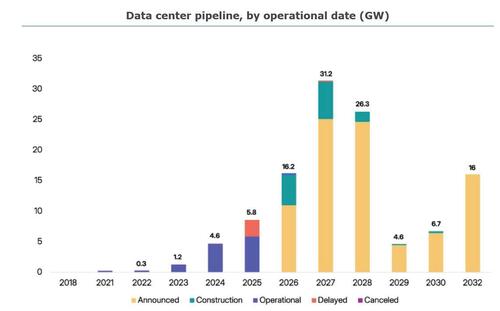

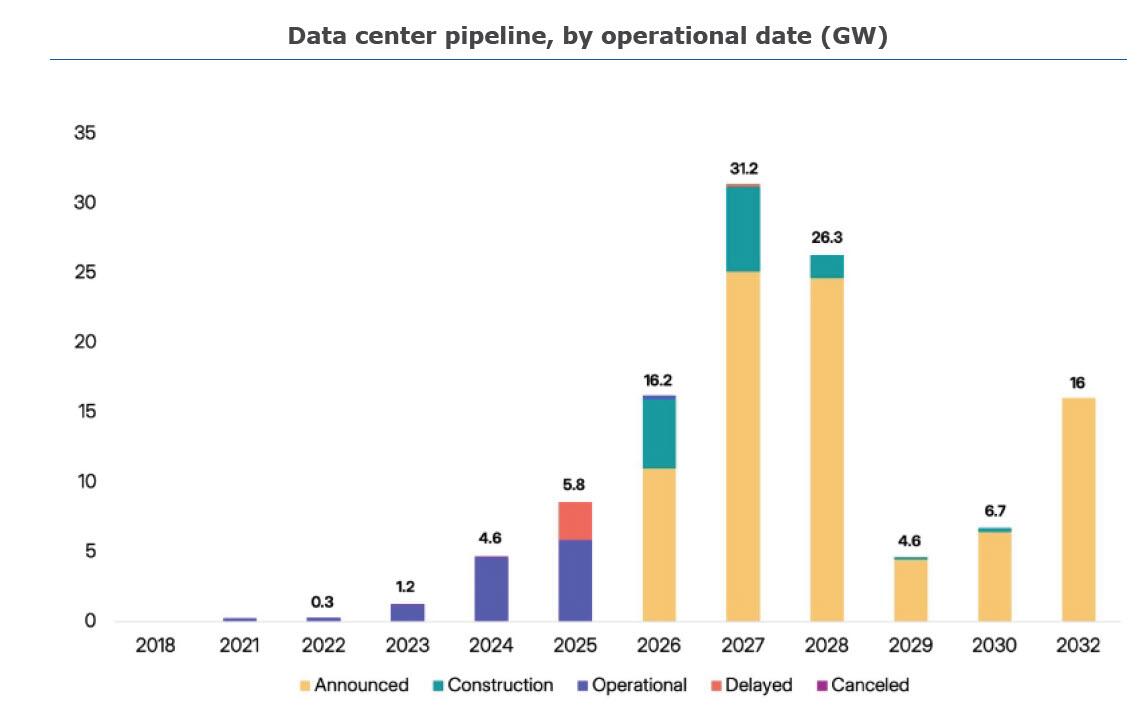

That's because, as Canaccord Genuity analyst George Gianarikas write two months ago, "the American data center boom is hitting a formidable wall of logistical friction." He is referring to the latest outlook by Sightline Climate, which is also reinforced by recent articles from Bloomberg and others, and reveals a sobering reality for 2026: nearly half of the nation's planned 16-gigawatt capacity faces cancellation or delay, with only 5 gigawatts currently under construction.

That's right: half.

This collapsing inertia stems from a volatile mix of local permitting hurdles, community resistance, and a desperate reliance on overextended global supply chains for critical components like transformers and helium.

Taking a step back, despite over $800BN of expected 2026 hyperscaler capex, a number which seems to jump by $50bn or see every quarter, nearly half of the data centers scheduled to begin operations in the US in 2026 "will either face delays or outright cancellations." The data, which comes from Sightline Climate's 2026 Data Center Outlook, suggests that just 30% - 50% of the ~16 GW of planned US capacity for the year will face risks, with only ~5 GW currently under construction!

And the horizon only grows darker in the coming years. By 2027, the gap between ambition and reality widens further, as a mere fraction of the announced 21.5 gigawatts has actually broken ground. Worse, according to Futurism, data centers slated to open in 2027 are progressing far more slowly than anticipated. "Only about 6.3 gigawatts worth of computing infrastructure are actually under construction, compared to 21.5 announced gigawatts."

And then visibility drops to virtually nothing beyond 2028 as uncertainty increases materially in the outer years. According to the article, "things get even dodgier in the coming years, with the vast majority of data centers planned for launch between 2028 and 2032 having yet to even break ground. There are a further 37 gigawatts of planned infrastructure which haven’t even received a firm completion date, only 4.5 [gigawatts] of which have actually begun work."

This trend suggests an increasingly uncertain future for the industry, where power constraints and grid instability cast long shadows over projects slated through 2032.

But while one can pretend the future is irrelevant, the same limitations are visible in the here and now: according to the SightLine report, "at least 16GW of data center capacity is slated to come online this year across 140 projects. 53% will be grid connected, 3% will be powered solely by on-site power, and 25% have not disclosed their powering strategies. We expect 30-50% of these projects to be delayed. Only 5GW is currently in construction."

And the punchline:

"We expect 30-50% of 2026 projects to be delayed, driven by power constraints (25% of projects have not disclosed powering strategies), increasingly effective community opposition, and potential grid equipment shortages. 11GW of 2026 capacity remains in the announced stage with no signs of construction, despite typical build times of 12 to 18 months. Itʼs still possible for this capacity to come online, but it would need to dramatically accelerate."

As noted above, the market had been stubbornly ignoring the physical limitations in the data center rollout... until last night, when recently IPOed chipmaker Cerebras reminded everyone of just how profound the data center limitations truly are.

Cerebras shares plunged in early trading after the newly public chipmaker gave an annual sales forecast that disappointed investors who were expecting the company to carve out a bigger slice of the AI data center market.

Like other rivals of Nvidia, Cerebras is navigating high expectations from investors who’ve grown accustomed to the rapid revenue growth and profits tied to a worldwide buildout of AI data centers. Nvidia and a small group of chipmakers have regularly blown past Wall Street estimates, creating an environment in which even solid earnings results don’t necessarily translate into share-price gains.

And at first glance, Cerebras fell into that bucket: the company said that revenue in 2026 will be $855 million to $865 million, above the sellside analyst estimate of $824.8 million. First-quarter sales jumped 94% to $193.4 million, beating estimates of $181.4 million. The Sunnyvale, California-based company reported a net loss of $14 million in the period ended March 31, also beating the estimated loss of $58.6 million. Cerebras’ hardware business generated sales of $110.6 million. Cloud and other services reported $82.8 million.

The company reported earnings for the first time since raising $5.5 billion in May as part of the biggest initial public offering in chip industry history. Cerebras has carved a niche for itself in artificial intelligence infrastructure with novel technology built around a massive chip that it says is better at running large AI models and generating fast responses for users.

And yet despite the solid earnings, the stock was punished, tumbling 15% below $200 and the lowest price since it broke for trading at $311 in early May (but still above its IPO price of $185).

Why the disconnect? After all sales easily beat estimates and grew at an impressive rate.

The answer: margins. The chip designer warned that annual profit margins would undershoot first-quarter figures. Cerebras forecast adjusted gross margins of 38% to 41% for 2026, compared with the 47% it reported for the first quarter.

The projection is far below those of rivals such as Nvidia's mid-70% range and Advanced Micro Devices' mid-50%, even as it came above analysts' estimates of 29.58%.

To be sure, analysts had flagged that gross margins could be pressured by the company manufacturing relatively larger-sized chips, and as it rents back its own systems from an existing client to meet short-term demand while it builds out more data center capacity.

But according to the CEO, the biggest challenge right now is not the chip size, but - going back to what we said at the beginning - getting enough data center space. As CEO Andrew Feldman said , “It’s a grand irony that after all this technology that we’ve invented, and Nvidia’s invented, buildings are the limiting factor,” he said in an interview before the results were released.

The scarcity of data center space is leading Cerebras to rent back some of its own systems from a customer and “aggressively” build out its own capacity, CFO Bob Komin said on a conference call after the report. It is these costs that will hurt margins by about 10 to 15 points this year, he said.(Adds premarket share move starting in first paragraph).

Which begs the question: where the hell are all the massive orders of GPUs and memory going if there are no data centers to hold them?

We don't know but, like Canaccord's George Gianarikas, we admit "we’re a little spooked."

In a note published earlier this month, the Canaccord strategist wrote that "At this moment, count us as hand-wringers. Panicans. Doomers. We have been writing a series of notes for ~2 years called "Something’s Got to Give" and "Glitch in the Matrix" where we voice our concerns about the speed at which the necessary energy infrastructure for AI is being constructed. Add in data center moratoria. And, financing concerns. Throw in a dash of loopy circularity. Not to mention, eery similarities to the telecom bust."

And yet, Gianarikas goes on, "the happenings of the past few months have been fascinating, historic, and head-scratching. In the face of all that glitching, hyperscalers continue to up the ante - deploying increasingly massive capital to expand data center capacity. While structural inflation and rising component costs are playing their part, the underlying catalyst is simpler (at least to us): an insatiable demand for "more cowbell", driving perhaps the most profound cycle of FOMO in human history."

To be sure, this spending is very much showing up in earnings results. Look no further than semis or power-related deal announcements (e.g., Generac and Fluence) or elements of the industrial supply chain or revenue growth at some of the hyperscalers.

Or look at US GDP. As we noted a month ago when we pointed out that AI now accounts for 75% of US GDP growth, "there is a troublingly disproportionate reliance on AI spending to anchor economic progress."

But - the Canaccord strategist asks - "what about the power? Can the power keep up with the build plans? We don’t think so. Channeling our inner Scotty from Star Trek: "I can't do it, Captain! I don't have the power!""

Even the Wall Street Journal has taken taking notice. In an article published last month, they said that “America’s Data Center Build-Out Is Falling Way Behind Schedule”. Yes. Yes, it is.

As Gianarikas concludes, "Though macro market mechanics sit outside our mandate, we cannot ignore the parabolic split between the AI-enablers and the AI-dislocated. It is a stark tale of haves and have-nots - and it leaves us with a haunting question: What happens if the lights don't turn on?"

We got one answer from Cerebras. But the bigger problem is what happens if there is simply not enough data center capacity to light all the unlit components? And what will the returns be on those hundreds of billions in debt spent to fund the AI rollout? We

Understandably, Canaccord is asking precisely that question: "where is the capital actually going? It has to be landing somewhere. The reality, we suspect, is that mountains of expensive compute hardware are currently operating as high-tech paperweights. While the industry boasts of sky-high capacity utilization, a closer look causes that narrative to fray - at least to us. "Lit" capacity may be humming, but how much remains in the dark?"

The answer from Cerebras is clear: "a lot"... and as more AI companies admit the unpleasant truth, expect a reckoning as the market finally asks the trillion dollar question.

Tyler Durden

Wed, 06/24/2026 - 10:35

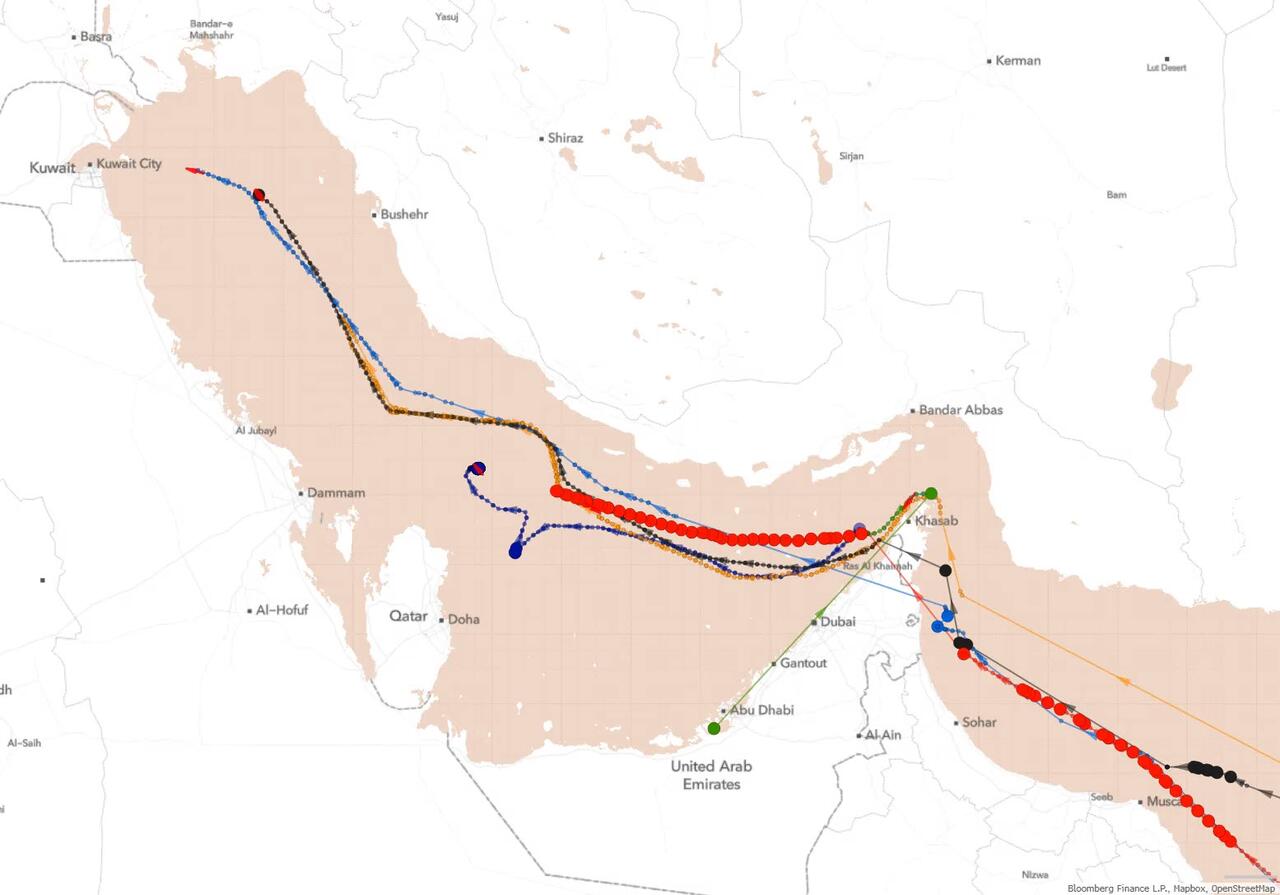

At least seven very large crude carriers have sailed into the Persian Gulf since the US and Iran agreed to an interim ceasefire deal late last week.Source: Bloomberg

At least seven very large crude carriers have sailed into the Persian Gulf since the US and Iran agreed to an interim ceasefire deal late last week.Source: Bloomberg

Iranian state media

Iranian state media Several attacks on Moscow refinery in a matter of days, via AFP

Several attacks on Moscow refinery in a matter of days, via AFP

Recent comments