Iran's Araghchi Says Talks Delivered "Major Progress" To End Lebanon War, Will Continue For Rest Of Week

- Round 1 ends: The US and Iran made “encouraging progress” in talks on a peace deal and will continue technical-level discussions this week, mediators

- Iran defiant, sees itself in strong position: Ghalibaf rejects US threats and links talks to a Lebanon ceasefire.

- Trump raises stakes via some typical Truth Social lashing out: Warns on Hormuz, Lebanon, and keeps military options on the table.

- Nuclear progress?: Some reports say not addressed, others suggest framework already being worked on.

Yes 12% · No 88%

View full market & trade on Polymarket

* * *

US and Iran Make “Encouraging Progress” In Talks On Peace Deal, Will Continue Technical-Level Discussions This WeekContrary to earlier reports from Iran media that US and Iran talks had concluded hours earlier, Bloomberg reported that the US and Iran made “encouraging progress” in talks on a peace deal and will continue technical-level discussions this week, mediators said, even as President Donald Trump again threatened strikes if Hezbollah keeps attacking Israel.

“Encouraging progress has been made including the creation of a mechanism for further technical talks,” mediators Qatar and Pakistan said in a joint statement. The parties agreed on a roadmap toward reaching a final deal within 60 days.

The sides also established a communication line to avoid incidents and miscalculation, with the aim of ensuring safe passage for commercial vessels through the Strait of Hormuz, the mediators said. They also agreed to create a “de-confliction cell” involving the parties and Lebanon to help ensure adherence to the cessation of military operations there.

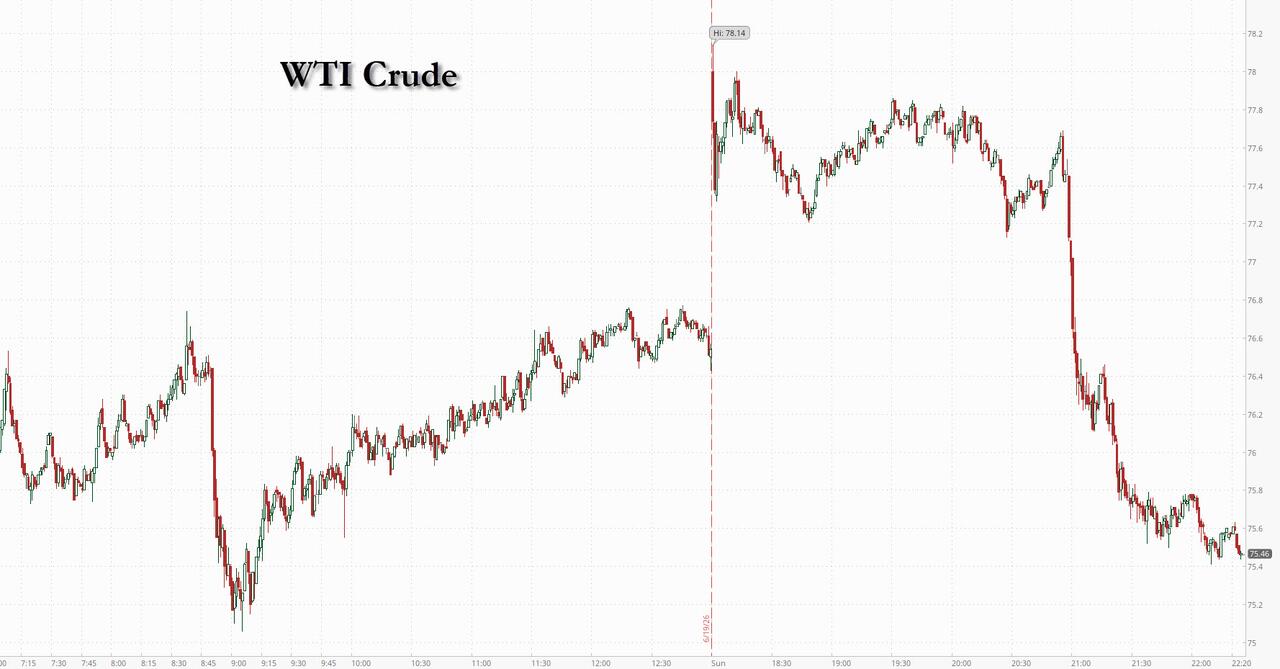

After rising in early trading following reports that Iran (almost but not really) had walked out on talks, crude oil turned lower and US stock-index futures pared losses after the statement.

Pakistani and Qatari mediation delivered major progress to end the Lebanon war, Iranian Foreign Minister Abbas Araghchi said in a post on X: "Tireless Pakistani and Qatari mediation has delivered major progress to end Lebanon War. Oil and petrochem exports are waived, blockade lifted, some frozen assets released, and major reconstruction & development plan launched for Iran. 1st real test: Lebanon deconfliction cell" the post said.

Tireless Pakistani and Qatari mediation has delivered major progress to end Lebanon War. Oil and petrochem exports are waived, blockade lifted, some frozen assets released, and major reconstruction & development plan launched for Iran.

— Seyed Abbas Araghchi (@araghchi) June 22, 2026

1st real test: Lebanon deconfliction cell https://t.co/q0okD2qwSO

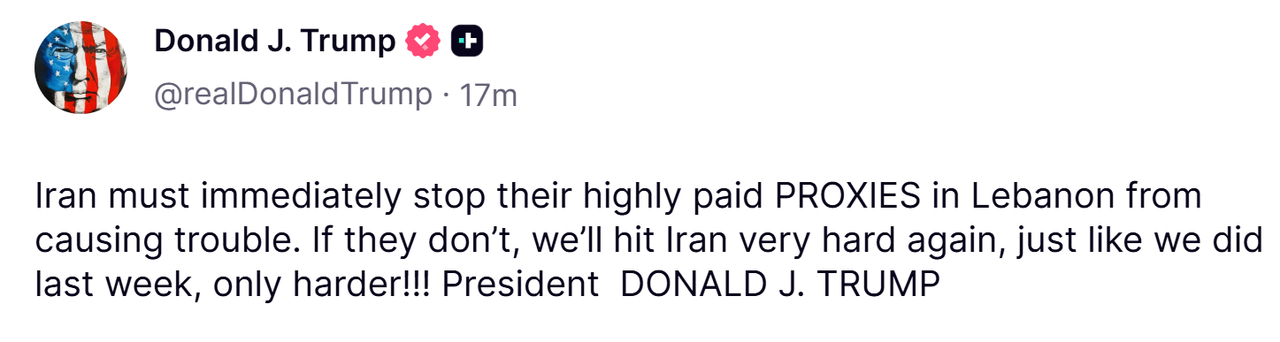

Things got off to a confusing start Sunday when Iranian media reported that Iran halted talks over Trump’s latest threat. As the meetings got underway, Trump said in a social media post that he would strike Iran again if it doesn’t “immediately stop their highly paid PROXIES in Lebanon from causing trouble.”

He also warned Iran that the US might start collecting tolls if there’s no deal. Speaking Sunday to Fox News, Trump said he told Iranian leaders directly that if they close Hormuz, “You won’t even make it back” to Iran, using an expletive.

Some FireworksAl Jazeera is reporting that talks have 'concluded' - but is this in actuality a premature conclusion given all the tension and heated issues of disagreement which came to the forefront?

- GHALIBAF: THEY'D BE BETTER OFF BEING CAREFUL W/ THEIR REMARKS

- IRAN'S GHALIBAF: WE DON'T ATTACH ANY SIGNIFICANCE TO US THREATS

- IRAN PARLIAMENT SPEAKER GHALIBAF COMMENTS ON X

- IRAN WILL END TALKS W/ US IF ISRAEL WON'T LEAVE LEBANON: TASNIM

- IRAN SAYS TRUMP'S THREAT IS A 'BLATANT VIOLATION' OF MOU

Below is a machine translation of what Iran's lead negotiator just issued on X as the day in Switzerland came to an end (also, another translation)...

"Do they not realize that if their threats actually worked, they wouldn't find themselves in today's position of desperation? We don't take American threats seriously.

They should be careful about what they say. Our armed forces stand ready to answer them in other ways. They can keep talking—it's we who take action."

This is immediately on the heels of Trump playing 'bad cop' to Vance's good cop, who has expressed some cautious optimism on Sunday from Switzerland. Bloomberg is reporting that the nuclear file was not dealt with in today's engagement.

The fact that the Swiss event happened at all can be called advancement on some level at least...

This is historic!

— Trita Parsi (@tparsi) June 21, 2026

Not because US and Iranian diplomats haven't met face to face before. Or that they haven't been on camera before (they were regularly during the JCPOA talks)

But never at the Vice President level!

You can see both Aragchi and JD Vance in this clip. pic.twitter.com/jeNBPeQmgr

Rumors of Iranians already calling it quits are false, reports Axios:

A diplomat attending the talks in Switzerland claims the Iranian delegation hasn't left and talks between the U.S. and Iran are still ongoing https://t.co/oQ1UkXwqYv

— Barak Ravid (@BarakRavid) June 21, 2026

Trump Reminds Iran Of 'Harder' Military Options On Table

With Vance and Witkoff in Switzerland, President Trump is still issuing some US redlines via Truth Social, and via apparent 'official leaks' - and quite quickly - through the press.

Trump is warning the Iranians on the sticking points of Hormuz closure and the Lebanon crisis. He has newly threatened on Sunday to hit Iran again if it can't constrain its proxies, namely Hezbollah, in Lebanon. In parallel, Tehran is demanding that Washington reign in Israel. A fresh Sunday Truth Social... brief but firm:

And more on some fresh reported warnings and pressure coming from Trump:

"You close it and you won't have a country." President Trump said he told Iranian officials about the Strait of Hormuz. "You won't even make it back to your fu*king country."

— Trey Yingst (@TreyYingst) June 21, 2026

"We may take over the Strait, if we have to," Trump said. "If they don't make a deal, we'll collect… pic.twitter.com/cErvdjCJmK

As the American delegation continues the high-stakes negotiations in Switzerland aimed at de-escalating, the White House is projecting cautious optimism while simultaneously reminding Tehran that military options remain firmly on the table.

Speaking as talks entered a critical phase, Vice President JD Vance said Sunday from Switzerland Washington has "made great progress over the last few hours" and expects "additional progress in the coming hours," describing the negotiations as an opportunity to "turn over a new leaf" in US-Iran relations. Vance emphasized that the administration's preference is not to return to the cycle of confrontation, adding that the US is willing to fundamentally transform ties with Iran if Tehran permanently abandons its nuclear ambitions.

"The question is how much more we can achieve in the Middle East," Vance said, while expressing confidence regarding the Lebanon front and signaling satisfaction with ongoing efforts to contain broader regional escalation.

"Better Watch His Mouth": Trump to Iran President via MediaYet Trump has just delivered a stark reminder of the consequences should negotiations fail. According to Fox News, Trump warned Iranian officials that closing the Strait of Hormuz would be an existential mistake, reportedly telling Tehran that it "won't have a country" if it attempts to choke off global energy flows, in the segment above. Trump also issued a personal warning to Iranian President Masoud Pezeshkian, saying he "better watch his mouth," while reports indicated the president used unusually blunt language during discussions with Iranian intermediaries over the strategic waterway.

President Trump spoke with the Iranians overnight warning them not to close the Strait.

— Trey Yingst (@TreyYingst) June 21, 2026

"You close it and you won't have a country," Trump said he told Iranian officials. "You won't even make it back to your fu*king country."

Perhaps most notably, Trump reiterated that he retains a "60-day option" and can "do whatever" he deems necessary after that period expires, a statement widely interpreted as preserving the possibility of renewed military action. The president also reportedly threatened additional strikes against Iran should Tehran's regional proxies in Lebanon resume attacks or undermine the emerging diplomatic framework.

The result is a familiar carrot-and-stick approach as talks are unfolding under the shadow of explicit US military threats and a rapidly approaching deadline that could determine whether the region moves toward détente or another round of escalation. But Iran has also made known that it is ready of a long war, but will Trump be willing to risk enduring the political and economic fallout?

Qatari, Pakistani Top Leaders Present, Optimistic Initial StatementsQatar's Foreign Ministry has formally confirmed the launch of the talks between the United States and Iran with the mediation of Qatar and Pakistan in Switzerland, with the Iranian delegation headed by Parliament Speaker Mohammad Bagher Ghalibaf and Foreign Minister Abbas Araghchi.

US Vice President JD Vance is leading the American side along with envoy Steve Witkoff. Also gathered at the Buergenstock Resort Lake Lucerne, near Stansstad, are Pakistan's Chief of Army Staff Field Marshal Asim Munir, and Pakistan's Prime Minister Shehbaz Sharif.

Qatar has expressed "its aspiration that these meetings will lead to the conclusion of a comprehensive and permanent agreement addressing all aspects covered in the Memorandum of Understanding." Iran has reiterated it wants a comprehensive settlement and final end to the war. But it also demands a final Lebanon-Israel peace settlement be linked in. Already there could be an inkling of progress on the nuclear front:

- PAKISTAN:US, IRAN AGREED ON REDUCTION OF ENRICHED URANIUM LEVEL

- PAKISTAN:IRAN'S ENRICHED URANIUM TO BE REDUCED FROM 60% TO 0.7%

- IRAN PRESIDENT SAYS QATAR TO RELEASE $6B AS TALKS START: IRNA

Screengrab via Government of Pakistan footage

Screengrab via Government of Pakistan footage

The last time Vance sat physically across from Iran's lead negotiator Ghalibaf was a full ten weeks ago, in mid-April. Interactions appear to initially be only through intermediaries, which will build up to face-to-face meetings, as happened in prior failed rounds.

What to Expect in 1st Round FormatQatar's foreign ministry has previewed the following planned format to the opening of the talks as follows:

- The ministry statement says “specialized technical and expert groups have been formed to negotiate the terms of the final agreement, which will cover all aspects of the Memorandum of Understanding” between the US and Iran.

- “Additionally, follow-up groups have been established to oversee the implementation of the Memorandum, monitor progress achieved, and work toward the conclusion of the final agreement,” it added.

- “This reflects the commitment of all parties to moving forward in the negotiation process in good faith, with the aim of reaching a comprehensive and sustainable agreement.”

Of course, in terms of "implementation" of just the MoU itself, things are not quite there yet, as sporadic fighting and Israeli aerial attacks continue in Lebanon, which could serve to derail the Switzerland process at any moment.

After roughly 45 min, the bilateral meeting between FM @araghchi and his Swiss counterpart @ignaziocassis came to a close at Bürgenstock Hotel. Quadrilateral talks between Iran, the US, Pakistan, and Qatar are expected to commence shortly at another venue on the same premises. pic.twitter.com/hOmovguWFs

— IRNA News Agency ☫ (@IrnaEnglish) June 21, 2026

Additionally, Iran has declared it has 'closed' the Strait of Hormuz just this weekend, but which the US military has been denying is a reality. VP Vance in media appearances has also been downplaying it.

The Lebanon situation seems the bigger, more pressing threat to the peace process - at least from Tehran's point of view. Dozens of people in Lebanon have been killed while at least six Israeli soldiers have been slain, with 20 wounded over past days of Hezbollah rocket and drone attacks.

Trump Between a Rock & A Hard Place Where Escalation is ConcernedAs a reminder, President Trump doesn't want to oversee an economic catastrophe driven by a worldwide energy crisis. It seems he's ready to anything to not let it happen under his watch:

President Donald Trump said Wednesday that he was motivated to finalize the memorandum of understanding (MOU) with Iran to prevent “economic catastrophe” if the war was not resolved soon.

“So rather than possibly going into a depression, rather than having your favorite president be Herbert Hoover, he was always the one I didn’t want to be,” Trump said of the 31st president whose policies are often blamed for starting the Great Depression.

“I didn’t want to see economic catastrophe. If you kept this going, that could have happened. But all I know is, every time we talked about the possibility of peace, the stock market shot up like a rocket ship,” Trump said during a press conference Wednesday on the sidelines of the G7 Summit in Évian, France.

And so judging by this and other of recent Trump admissions, Iran clearly enters Switzerland in very strong negotiation position. Its current rhetoric regarding the Strait of Hormuz also reveals this.

JD Vance met with Pakistan's Prime Minister Shehbaz Sharif and Army Chief Asim Munir in Switzerland.pic.twitter.com/5bteI1Vtyu

— Clash Report (@clashreport) June 21, 2026

Tehran has accused the US of a "clear breach of its commitments" and announced Saturday that "the Strait of Hormuz will be closed to the passage of vessels," according to state broadcaster IRIB.

More Details on FormatFor more on the details of the format, CNN has reported some further information in the following:

- When and where do the talks start? US and Iranian negotiators will begin their meeting at around 1 p.m local time (7 a.m. ET) at the Swiss mountain resort of Bürgenstock, an Iranian source told CNN.

- Who will be there? Both the United States and Iran have sent high-level officials to Switzerland. Vice President JD Vance is heading up the US side, while Iran’s lead negotiator, Mohammad Bagher Ghalibaf, will lead Tehran’s delegation, Iranian media outlet Saberin News reported Saturday.

- What format will they take? Iran’s Foreign Ministry spokesman, Esmail Baghaei, who is part of the Iranian team, earlier told state media “the Iran-US talks will be held in a quadrilateral format, with the presence of Pakistani and Qatari delegations.”

- What will be discussed? Lebanon is likely set to top the agenda after clashes between Israel and Hezbollah threatened the nascent agreement between the US and Iran. Vance says he hoped he would make advancements on negotiations surrounding the handling of Iran’s nuclear materials.

To put things in perspective about the long road ahead, analyst and reporter James Bayes - who is on the ground for the talks in Switzerland, has offered the following: "This is a very different deal from the Iran nuclear deal that was done by [former US] President Barack Obama … things have changed completely. But I think it’s worth looking at that deal for one reason, which is the timeline – how long these things take."

Iranian Foreign Minister Seyyed Abbas Araghchi, center, arrives at the Buergenstock resort in Obbuergen, near Lucerne. Pool via AP

Iranian Foreign Minister Seyyed Abbas Araghchi, center, arrives at the Buergenstock resort in Obbuergen, near Lucerne. Pool via AP

"Because when they did an interim deal then, in November 2013 until the final deal in 2015, it took 597 days," the correspondent added. "So, even though the circumstances have changed – it’s a very different deal and they’ve got the knowledge of that deal as well which is helpful – it’s a lot to do in just 60 days."

Tyler Durden Sun, 06/21/2026 - 13:00

Reuters/Sky News

Reuters/Sky News Attack on Belarusian bus. MAX/Moscow Times

Attack on Belarusian bus. MAX/Moscow Times Image: Keystone-SDA

Image: Keystone-SDA

Recent comments