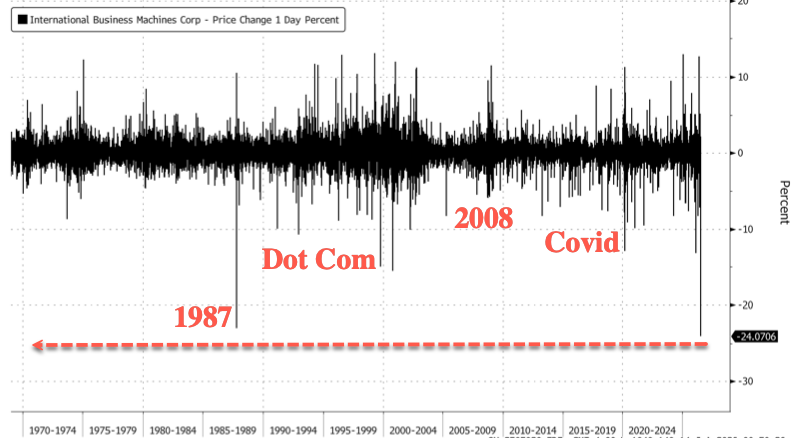

Futures Mixed Ahead Of CPI And Warsh Testimony, As IBM Sinks, Bank Earnings Fizzle

US stocks are struggling for direction as traders waited to buy the dip on a busy day that kicked off with Wall Street earnings whichwith JPM, BofA, Goldman, Citi and Wells all reporting. Kevin Warsh’s testimony before Congress and CPI data are due later. As of 8:00am ET, S&P 500 futures fell 0.2% with Nasdaq 100 contracts up 0.6%, set for a rebound from the selloff in AI-linked names yesterday and defying declines elsewhere. In premarket trading, IBM crashed 20% - the most since 1987 - after unexpectedly preannouncing a big revenue miss; elsewhere, semiconductors are leading after Korea's Kospi staged a powerful rebound from session lows while SK Hynix saw a 10% swing in Korea trading; Mag7 is mixed, and the AI theme is bid. WTI crude traded around $80/bbl and Brent above $86/bbl (both off session highs) as the ceasefire / MoU appear to be voided with both sides claiming control of the SoH. Both Disc and Staples are lower, perhaps reflecting some consumer fears. Energy / Mats are bid on the Middle East, Fins are bid into earnings, Industrials are higher with the AI theme with HC mixed. Higher oil prices lifted odds of a July US rate hike in place, with swap markets signaling a nearly 40% chance of a hike when the Fed meets later this month. The yield on two-year UK gilts touched the highest level since May. Treasuries edged higher and the dollar fell. Traders will closely watch the CPI data, especially after the Fed’s Waller, a former dove, said Monday that a hike is on the table if inflation stays hot and as bond market volatility saw a double-digit jump. The recent fall in gasoline prices likely helped drag down the CPI print, which may notch its first monthly decline since the onset of the pandemic in 2020. The macro focus is on CPI plus the consumer / GDP read-through from GSIBs. The data calendar includes weekly ADP employment change (8:15am), June CPI (8:30am) and May TIC flows (4pm), Fed calendar includes Warsh’s testimony on its Semi-Annual Monetary Policy Report before the House Financial Services at 10am. Also scheduled to speak are Governor Barr (12:40pm), Chicago Fed’s Goolsbee (1pm) and Governors Cook (1:30pm) and Bowman (2:55pm).

In premarket trading, Mag 7 stocks are mixed: Apple is down 0.7% after being cut to underweight at KeyBanc, which expects weaker device demand and service revenue growth in the US (Nvidia +1.2%, Tesla +0.3%, Amazon -0.4%, Alphabet -0.5%, Microsoft -2.8%, Meta Platforms -1.1%).

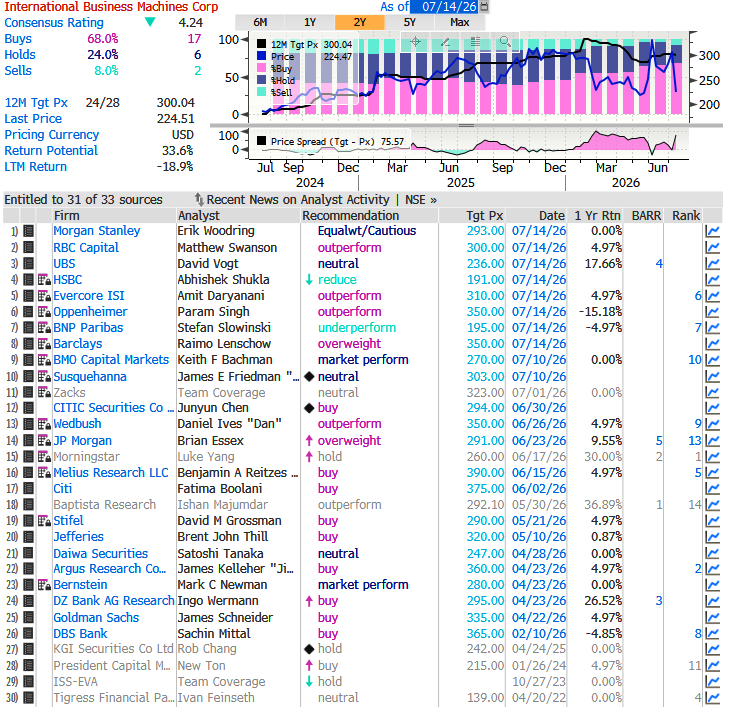

- IBM (IBM) sinks 19% after reporting preliminary quarterly sales results that missed analysts estimates, with Chief Executive Officer Arvind Krishna saying customers were holding back spending.

- Software and IT/professional services stocks are broadly lower after IBM’s preliminary revenue for the second quarter fell short of the consensus estimate. Microsoft falls 2.8%, Intuit drops 5% and Adobe declines 4.8%

- CoStar Group (CSGP) falls 5% after the real estate analytics firm named Robin Rossmann as the company’s next CFO. Rossmann will succeed Christian Lown, who is stepping down to pursue an opportunity outside the company’s industry.

- Goldman Sachs Group (GS) climbs 1.3% after posting $7.42 billion for a quarter with record-breaking stock-trading results, driven by financing and taking profit in arranging bets.

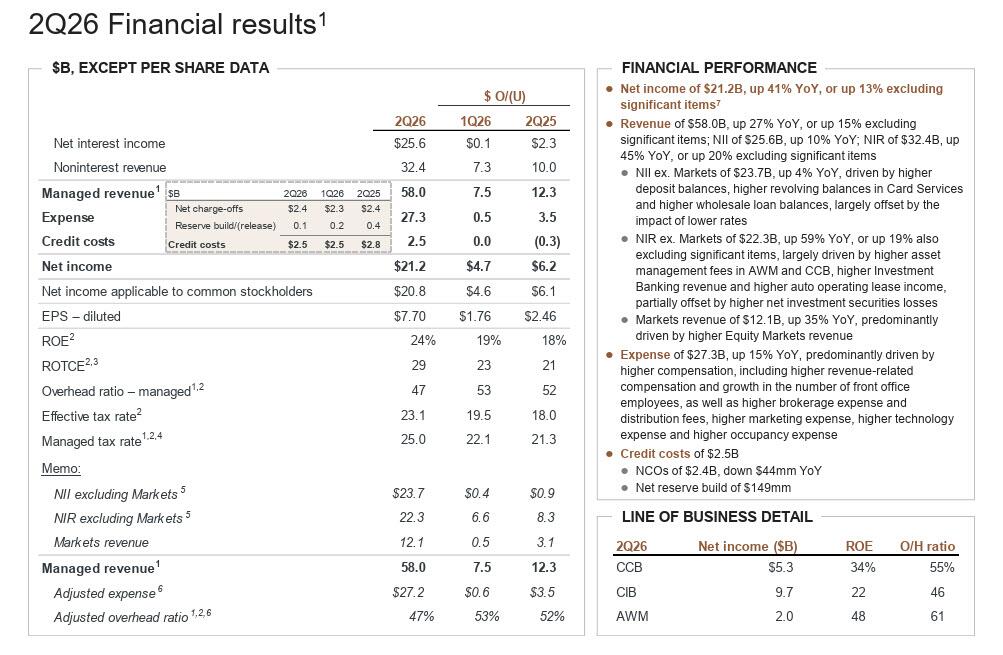

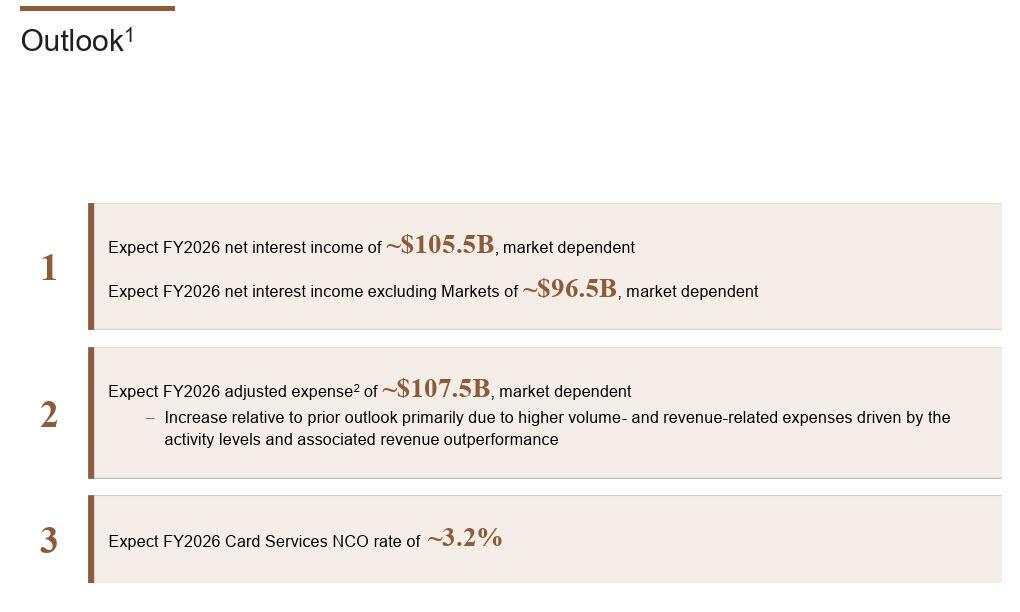

- JPMorgan (JPM) falls 2% after the lender said it sees full year adjusted expenses at about $107.5 billion, previously seeing about $105 billion.

- O-I Glass (OI) slips 3% after BofA cut its rating to underperform from buy, saying relative upside for the shares may lag due to volume weakness in glass packaging.

- Trex (TREX) climbs 3% after the decking manufacturer’s second-quarter net sales forecast beat the average analyst estimate.

In other AI related developments Nvidia and Mitsubishi Heavy Industries are looking to tie up on AI data center technologies, Nikkei reported, and Samsung is said to be in early discussions for a potential US share sale. Memory and chip stocks remain the core equity theme after investors poured $21 billion into ETFs last week, according to JPMorgan. In other corporate news, Brown-Forman President/CEO Lawson Whiting is set to step down once a successor is named. BP said it expects to write down another $1 billion from energy transition assets in the second quarter, as the British major continues the painstaking work of re-orientating itself toward its core oil and gas business. Apple falls in premarket trading after being cut to underweight from sector weight at KeyBanc, which expects weaker device demand and service revenue growth in the US.

Today's event-filled calendar began with a mixed reaction to Goldman Sachs, JPMorgan, Bank of America, Wells Fargo and Citigroup, as the banks were already priced to perfection, and despite blowout earnings, their stocks mostly dipped in premarket trading. June CPI data is expected to show some relief after inflation accelerated rapidly from March through May. Federal Reserve Chair Warsh is scheduled to testify before House members hours later.

“Geopolitics on the margin is a negative, but the oil price has not spiked dramatically,” said Richard Flax, chief investment officer at Moneyfarm. “I expect Warsh will give a sort of data-driven speech rather than say too much about forward guidance. For us, it’s more about the inflation data.”

Warsh would probably prefer not to present this week’s Humphrey-Hawkins testimony, but “Congress isn’t inclined to let Warsh off the hook,” writes Bloomberg Senior US Economist Andrew Sacher, who outlines what to expect from Warsh’s appearances.

In an escalation of the standoff between the US and Iran over the Strait of Hormuz, President Donald Trump reinstated the blockade of Iranian ships transiting the waterway and demanded a 20% reimbursement for all other cargo. US forces also completed another round of strikes against the Islamic Republic.

“We know the market can sustain far higher oil prices and US stocks keep rising,” said Alpesh Patel, managing partner at RootBridge Capital. “The only thing that matters is any indication rates are going to rise.”

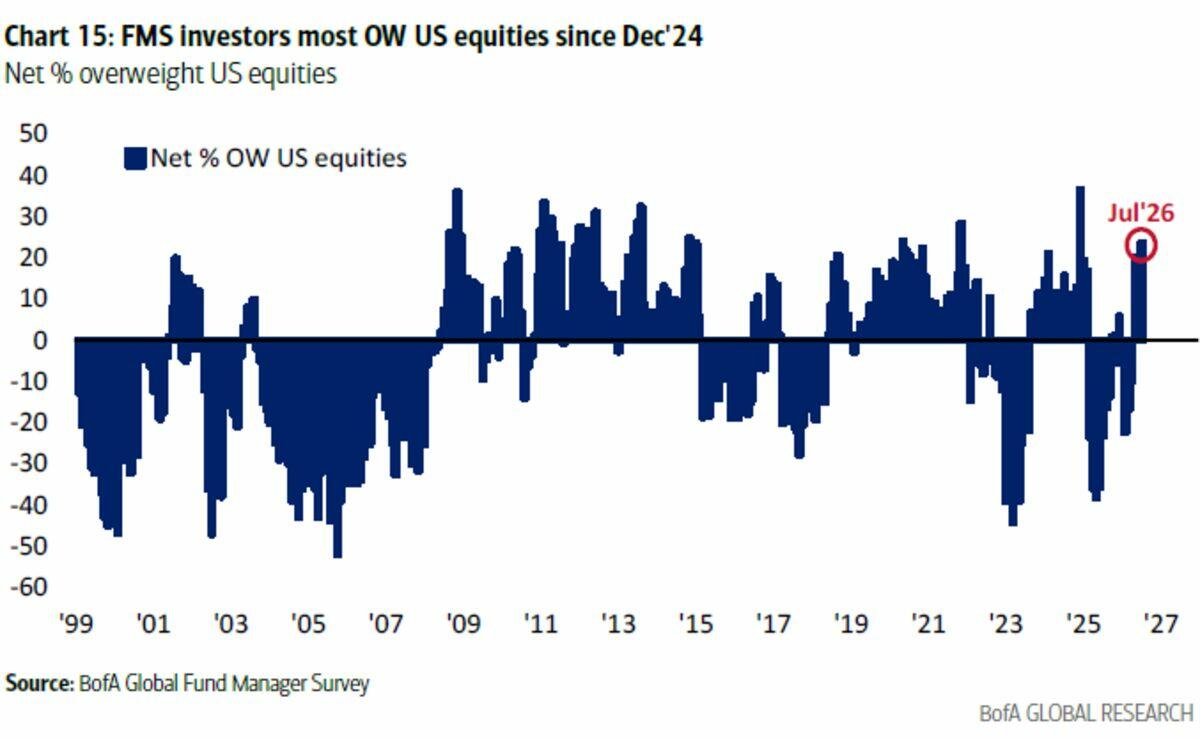

Global investors buying stocks aggressively should consider reducing exposure with investor sentiment getting extremely bullish, according to the latest BofA Global Fund Manager Survey, with positioning on US equities now at its highest level since December 2024 at a net 24% overweight, cash levels “uber-low” at 3.6%, and BofA’s Bull & Bear Indicator now at the extreme bull reading of 9.

Overnight, China exports climbed 27% from a year earlier, exporting a record $412 billion worth of goods in June, blowing past all forecasts and turbocharged by a global investment supercycle in AI.

In a sign of confidence that the artificial-intelligence buildout will keep on fueling demand for chips, people familiar said Samsung Electronics is exploring a potential offering of ADR, similar to SK Hynix, in hopes of top ticking the memory bubble. Semiconductor stocks bounced in early US trading after Monday’s rout. “This suggests that the Nasdaq could break its short-term negative correlation with the oil price, and rise alongside energy prices if this continues,” wrote Kathleen Brooks, research director at XTB.

In Europe, the Stoxx 600 slid 0.4%, having dodged the weakness in tech stocks on Monday, is falling 0.6% with a drag from the media, travel and consumer sectors. Ericsson AB’s shares fell as much as 10% after warning that margins in its main networks business will come under pressure. Here are the biggest movers Tuesday:

- Mycronic shares gain as much as 14% to hit a record high as earnings from the Swedish electronics equipment group beat forecasts. DNB described the report as “impressive”

- BP shares surged as much as 3.3% to touch a one-month high as Jefferies noted that the oil major’s net debt estimates for the second quarter had undershot expectations

- Allegro climbs as much as 6.5% to highest since 2022 after the Polish e-commerce company reported strong preliminary 1H results and indicated it may raise its full-year outlook

- Salzgitter shares rise as much as 7.4% as Jefferies upgrades its rating on the steel producer to buy from hold, citing benefits from EU steel quotas

- Hapag-Lloyd shares rise as much as 8.2% in Frankfurt after the German container shipper boosted its Ebitda forecast for the year

- Genus shares rise as much as 14%, the most in about six months, after the animal genetics specialist said it now sees full-year profit ahead of market expectations

- Ericsson shares fall as much as 10% after the Swedish mobile networks and technology group said margins for its key Networks division will come under pressure in the second half of 2026, overshadowing otherwise in-line figures

- IntegraFin shares fall as much as 5.4%, the most in nearly two months, as the investment platform sees third-quarter flows come in slightly below some analysts’ expectations

- Norske Skog falls as much as 18%, the most since February 2025, after the Norwegian paper and forestry firm reported its latest earnings, which included misses on total operating income and Ebitda

- Norion Bank falls as much as 13%, the most since February, after the Swedish banking group reported weak second-quarter earnings. SB1 Markets points to an underlying miss in net interest income and higher costs

Asian stocks reversed earlier losses as South Korean memory chipmakers rebounded in late trading. The MSCI Asia Pacific Index gained 0.4% after falling as much as 1.6% earlier in the session. Samsung was the biggest boost to the index amid news the company was in early discussion for a potential share sale in the US. SK Hynix also erased an early plunge, helping to lift the Kospi gauge. The movements in Korea’s memory chip stocks underscore the extreme volatility gripping some of the world’s biggest beneficiaries of the artificial intelligence boom. Japan’s Topix rose as investors looked for opportunities in non-tech sectors that have lagged the broader market. Taiwan’s Taiex index dropped 1.4% to its lowest in more than two weeks.

The “recent volatility indicates you are starting to build two camps — one remains very optimistic, whereas you have a growing group that question the sustainability,” said Mattias Martinsson, chief investment officer at Tundra Fonder AB. “That creates a tug of war, from day to day, which has very little to do with geopolitical events. For today the optimists have the upper hand.”

In rates, treasuries are little changed after retreating from session highs reached as oil extended its climb, with investors awaiting testimony by Fed Chair Kevin Warsh and June CPI report. US 10-year yield near 4.62% outperforms bunds and gilts in the sector by 2bp and 4bp following retreat from 4.634%, highest since May 20; curve spreads are also little changed. 2- and 5-year tenors reached new YTD yield highs. Around 11bp of Fed tightening is priced in for the July policy meeting following Monday’s increase on hawkish comments from Fed Governor Christopher Waller. Money markets see at least one Bank of England and one European Central Bank rate hike this year, while leaning strongly toward a second in December. IG dollar issuance slate empty so far. Monday saw a combined $6.7 billion priced as issuers paid about 2.7 basis points in new issue concessions on deals that were 5.5 times covered.

In FX, the Bloomberg Dollar Spot Index is down by 0.2% and moves across currency markets remain relatively muted.

In commodities, Brent extended its gain to $86/barrel on the new US blockade of Hormuz is driving more rate-hike bets from traders and rippling across the short-end of European bond markets. WTI crude oil futures are up about 3%, off session highs reached as the truce between the US and Iran collapsed following fresh attacks on shipping in the Strait of Hormuz. Gold is gaining to move back above $4,000/oz.

The US economic data calendar includes weekly ADP employment change (8:15am), June CPI (8:30am) and May TIC flows (4pm), Fed calendar includes Warsh’s testimony on its Semi-Annual Monetary Policy Report before the House Financial Services at 10am. Also scheduled to speak are Governor Barr (12:40pm), Chicago Fed’s Goolsbee (1pm) and Governors Cook (1:30pm) and Bowman (2:55pm)

Market Snapshot

Top Overnight News

- President Donald Trump formally notified lawmakers this weekend that the nation is once again at war with Iran, giving his administration another 60-day clock to use the military in the region without congressional approval. Politico

- Brent topped $86 as Donald Trump said he would reinstate a blockade of Iranian ships transiting the Strait of Hormuz at 4 p.m. ET today. BBG

- For decades, OPEC influenced the market by how much oil it produced. But China, the largest importer, is demonstrating its remarkable power over prices. Typically the world’s largest oil importer, China slashed purchases this spring, reducing demand so much that it prevented oil prices from soaring even higher earlier in the war. WSJ

- Trump plans to back a Russia sanctions bill championed by late Senator Lindsey Graham, a person familiar said. His support would be a major win for Ukraine’s push to punish buyers of Moscow oil and gas. BBG

- China's exports surged in June, buoyed by orders for chips to fuel the global AI boom and automobiles, deepening producers' reliance on overseas buyers as policymakers in the world's No. 2 economy continue to grapple with how to boost demand at home. The stronger-than-expected trade performance keeps China on track to post a surplus topping $1 trillion for a second straight year, with factories sustaining sales despite slowing growth in major economies and trade frictions with Washington. RTRS

- Japanese policymakers on Tuesday flagged the possibility of changes to the asset allocation of the nation's giant state pension funds, though they offered no clues on the timing or scale of any shift. RTRS

- Over the past year, the Trump administration has made deals to acquire equity stakes in more than two dozen firms, an unusual practice that extended the government’s influence over industries including semis, nuclear energy, minerals, and quantum computers and steel. AI execs are increasingly wondering if they will be next. NYT

- Gov. Kathy Hochul is banning large data-center construction for up to a year, making New York the latest state to confront the rollout of sites powering the artificial-intelligence boom. The move responds to concerns over power costs, water supplies and community impacts as states consider limits on AI infrastructure’s effects on electricity grids and utility bills. WSJ

- As Warsh prepares to face Congress, traders now see a US rate hike later this month as a coin toss. Money-market pricing suggests traders boosted their wagers for a July increase to almost 50% after yesterday’s strikes on Iran. BBG

- US House will vote today on merging the SAVE America Act with a national security and State Department funding bill: Fox

- Trump said they're looking into whether Cuba is storing Iranian drones, while he added that they will take care of it if Cuba has Iranian drones.

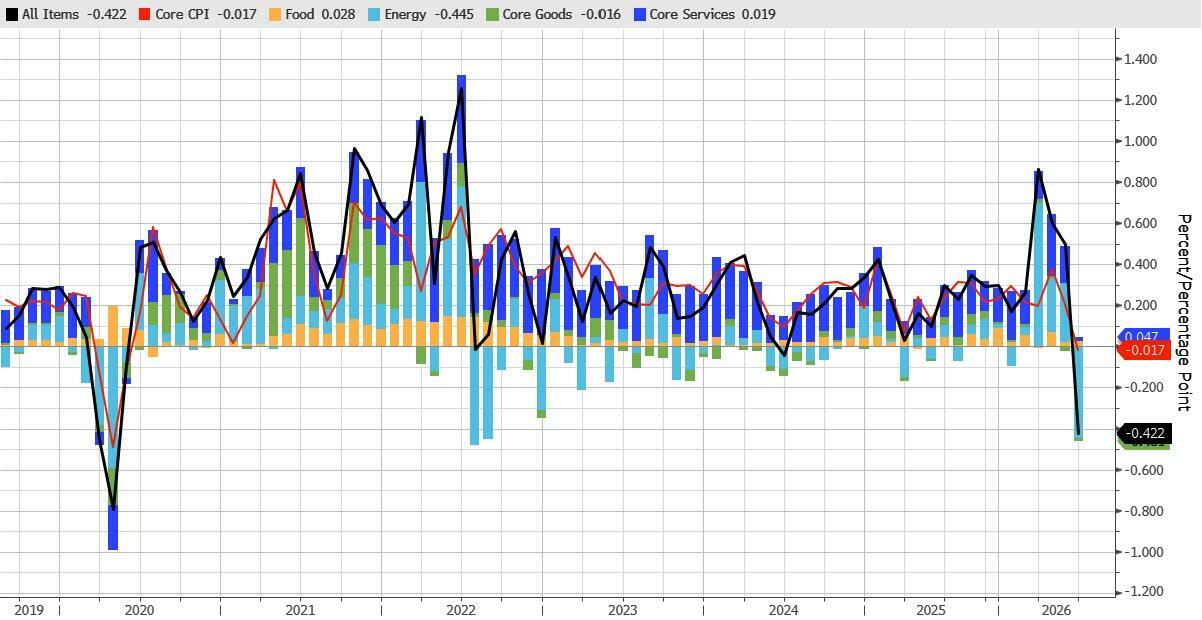

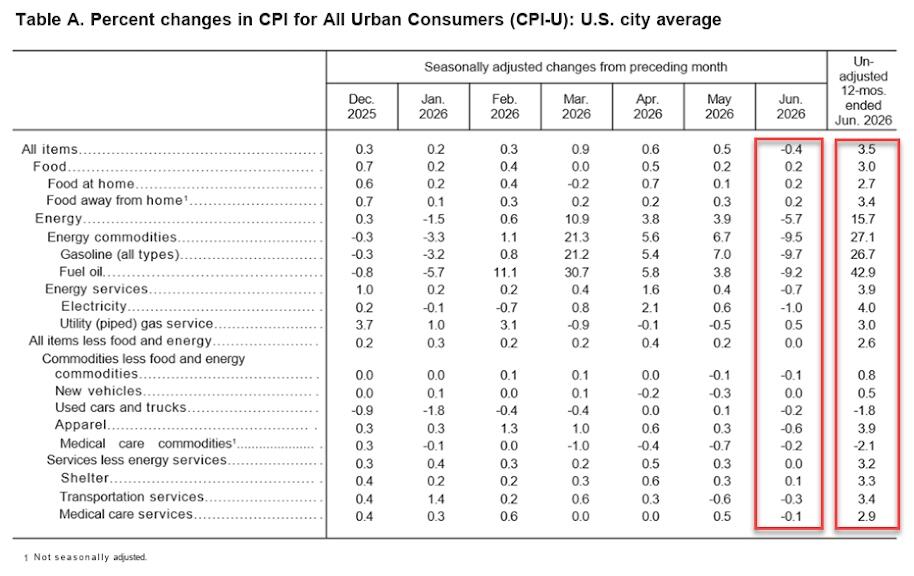

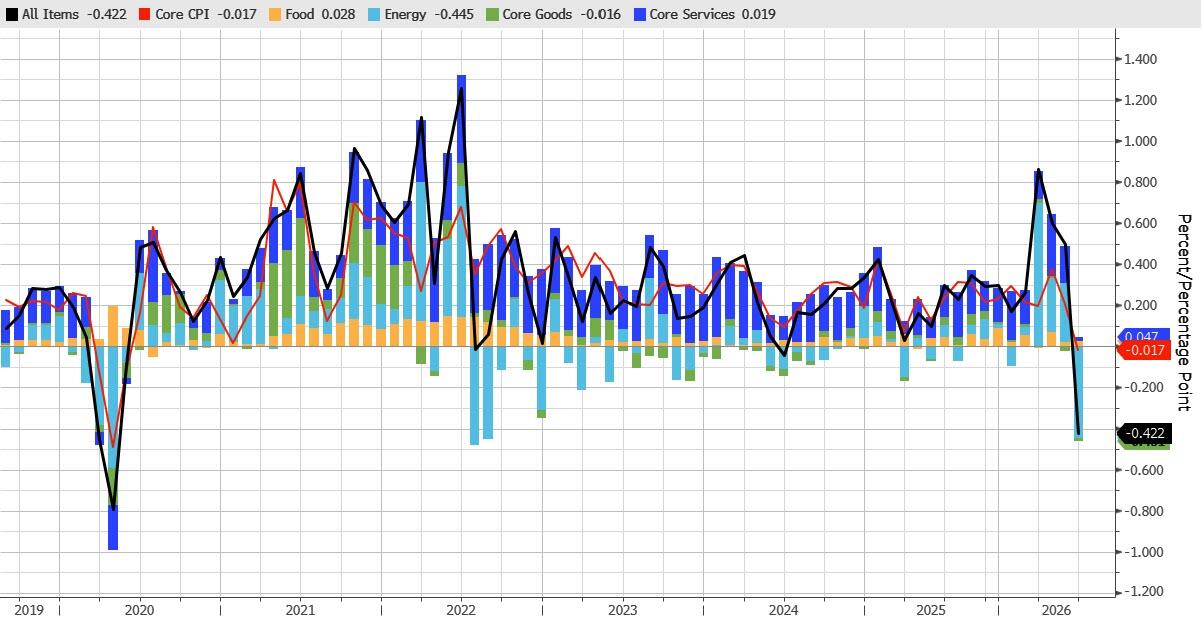

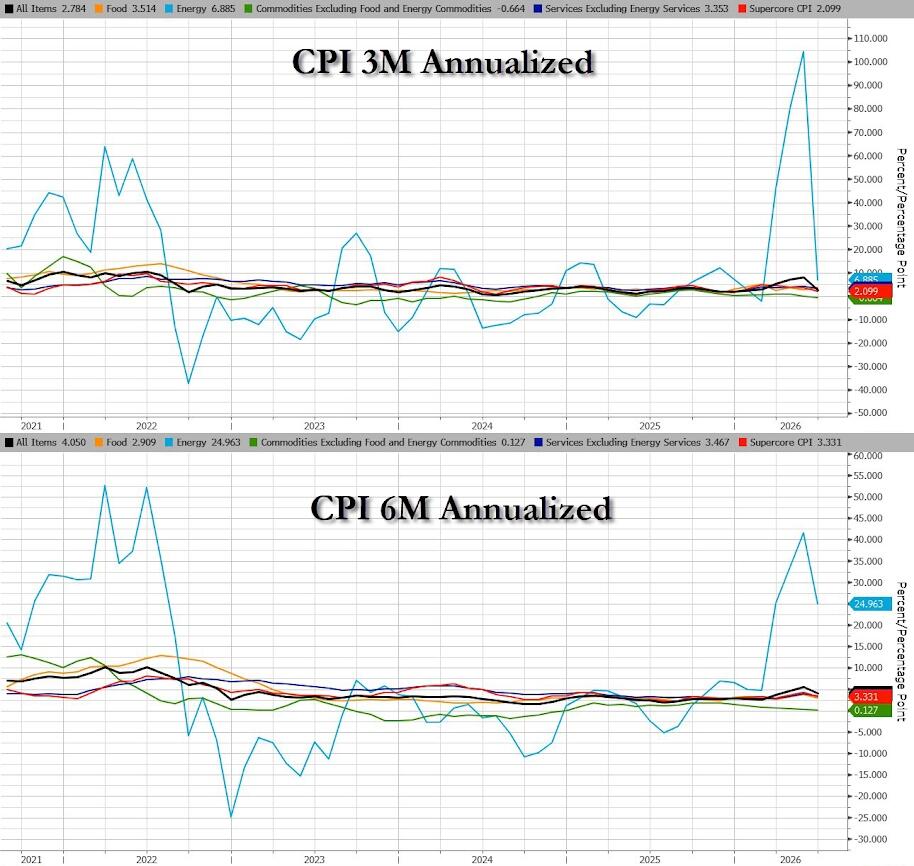

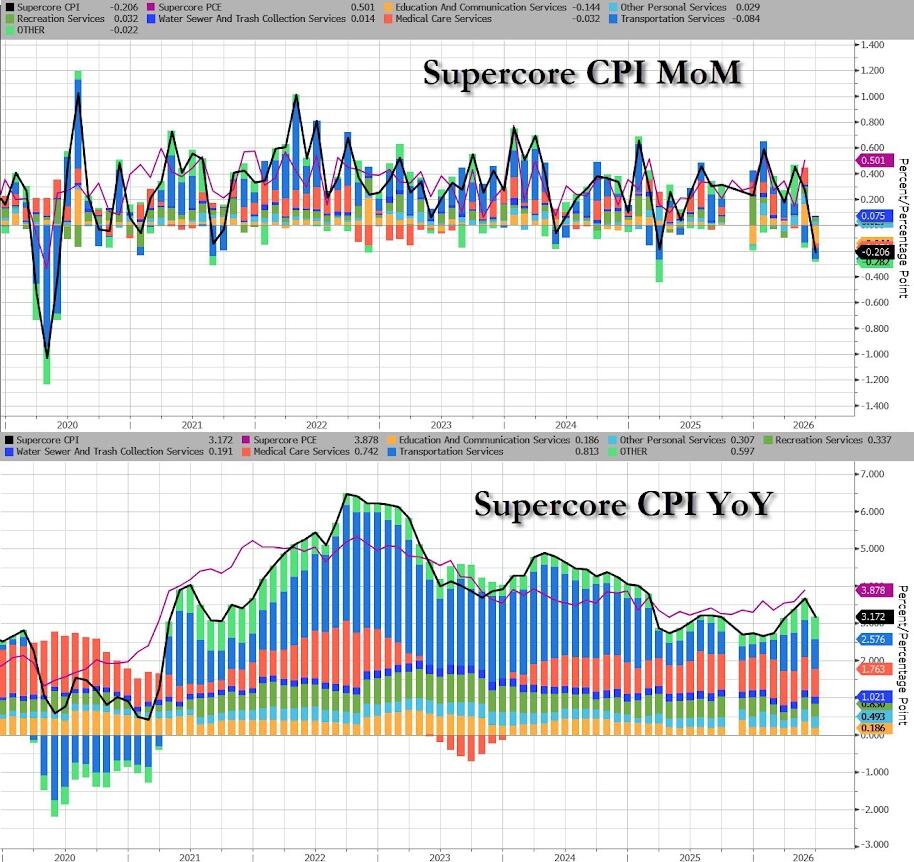

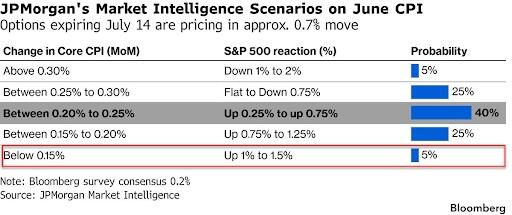

- CPI Preview: Goldaman expects a 0.17% increase in June core CPI (vs. +0.3% consensus), corresponding to a year-over-year rate of +2.76% (vs. +2.9% consensus). The bank expects a 0.11% decline in headline CPI (vs. -0.1% consensus), reflecting lower energy prices. The forecast is consistent with a 0.24% increase in core PCE in June, reflecting another large increase in its financial services component.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly in the red following the weak lead from the US, where risk sentiment was weighed on by tech selling and geopolitical escalation, while US-Iran strikes persisted for the third consecutive night and Trump announced to reinstate the naval blockade on Iran, as well as touted a 20% Hormuz shipping fee. ASX 200 was dragged lower by weakness in tech, industrials, consumer staples and financials, but with the downside stemmed by resilience in energy and utilities, while there was also an improvement in Westpac Consumer Sentiment. Nikkei 225 initially dropped below the 67,000 level amid tech weakness and higher oil prices, but then gradually nursed its losses and returned to flat territory as domestic yields softened. Hang Seng and Shanghai Comp conformed to the tech-related weakness and ultimately failed to benefit from the better-than-expected Chinese trade data.

Top Asian News

- Japanese Finance Minister Katayama suggested it is time to consider including JGBs in NISAs, and stated that if the environment surrounding asset management changes sharply, a change to GPIF's portfolio could be examined, while she hopes to quickly establish details on steps to make Japanese government bonds more attractive.

European bourses (STOXX 600 -0.6%) are lower across the board after Monday's choppy trade. Escalating US-Iran tensions return as a headwind for Europe, with energy prices rising, weighing on many of the continent's biggest industries (airlines, luxury). European sectors highlight the negative bias. Basic Resources (+1.3%) and Energy (+1.2%) are printing decent gains, while Utilities (+0.3%) and Chemicals (+0.2%) also trade in the green. To the downside is Travel & Leisure (-2.1%), Media (-2.0%), and Consumer Products & Services (-1.9%).

Top European News

- EU Commission approved EUR 659mln German State aid for four new semiconductor facilities.

- German Wholesale Prices MoM (Jun) M/M -0.7% vs. Exp. 0.2% (Prev. -0.6%).

- UK BRC Retail Sales Monitor YoY (Jun) Y/Y 1.7% vs. Exp. 2.9% (Prev. 3.4%).

FX

- G10s are mostly firmer as markets are reluctant to buy Dollars into US CPI, after it gained on Monday. Kiwi is the clear outperformer; energy exporters CAD and NOK also perform well.

- Geopolitics remain constructive for USD with Brent over USD 85/bbl, in addition to this, hawkish Fed speak from Waller saw markets assign a 50% probability of a Fed hike this month. (“Fed would need to consider a rate hike in the near term if core inflation is hot this week”). Despite these factors, the Buck is negative on the day as it stabilises below Monday’s 101.32 peak ahead of a packed session which is slated to see US CPI, and Warsh’s testimony to the US house which potentially sees a text release at 13:30 BST. The level to watch if momentum continues today is the 21DMA @ 101.00, should CPI come in hot, Monday’s 101.32 peak will be in focus, thereafter is July 2nd’s 101.43 high.

- Kiwi is the best performer once again as markets add to RBNZ tightening bets, interest rate futures now implying 58bps by year-end - around 5bps added vs. the end of Monday’s London session. Upside which comes after hawkish remarks from RBNZ's Conway and a strong quarterly NZIER Business Confidence.

Fixed Income

- US and Iran continued to strike each other for a third night, after President Trump warned that they would hit Iran “very hard”. POTUS also announced a naval blockade on all Iranian ports, which is set to begin at 21:00 BST / 16:00 EDT.

- Crude benchmarks were firmer throughout the APAC session, though price action was more-or-less sideways. Into the European morning, the bias turned a bit more bullish after the UKMTO reported another incident on a tanker near Oman. This comes after two Emirati tankers were struck overnight. It is clear that the IRGC will not accept any transits through undesignated paths through the Strait of Hormuz; as such, traffic through the Hormuz is waning. Marine Traffic data has shown that only two tankers completed passages through the Hormuz in the 24 hours up to 07:25 BST today; this compares to c. 28 ships/day following the US-Iran MoU signing.

- As it becomes apparent that ships are no longer going through the Hormuz (and added risk of the blockade and/or nuclear attacks), the crude complex has moved higher. Brent Sep’26 (+3.7%) sits at the upper end of a USD 83.68-87.38/bbl range.

- Spot gold is a little firmer this morning, and trades within a narrow USD 3,983-4,034/oz range; currently holding just above the USD 4k/oz mark. The yellow metal appears to be taking a breather following a couple of sessions in the red, which was spurred by recent geopolitical escalations and a hawkish Fed speak via Waller. Elsewhere, base metals hold a positive bias following stronger-than-expected Chinese data overnight. In brief, Exports and Imports both rose from the prior, and by more than the consensus. 3M LME Copper holds within a USD 13,461-13,624/t range.

- Germany sells EUR 4.222bln vs exp. EUR 6.0bln 2.70% 2028 Schatz: b/c 1.13x, average yield 2.77%, retention 29.63%.

- Japan sells JPY 530.9bln 20-year JGBs; b/c 4.52x (prev. 2.97), average yield 3.626% (prev. 3.542%), Tail in price 0.00 (prev. 0.24).

- The Netherlands sells EUR 3.27bln vs exp. EUR 2.5-3.5bln 2.50% Jan 2031 DSL: Average yield 2.911% (prev. 2.795%).

- Australia sells AUD 400mln 5.00% June 2036 bonds b/c 4.1, avg yield 4.908%.

Commodities

- A bearish start for benchmarks as the complex reacts to the overnight energy move.

- Action that was sufficient to push Bunds below the 125.00 handle and to a 124.82 base, lower by just over 40 ticks on the day. Since, no real reaction to the morning’s updates, including a UKMTO tanker report in Oman, despite modest energy upside at the time.

- For Germany, June’s WPI was dictated by energy, with the Y/Y moderating from the prior but at an elevated level as mineral oil products were just under 22% higher vs June 2025. However, the same component was down 6.8% M/M, leading to a -0.7% headline M/M print (exp. 0.5%, prev. -0.6%). No move to the series.

- Gilts opened lower by a handful of ticks before extending below the 87.00 handle, and then moving sharply lower to an 86.42 base, catching up to the above and continuing the pattern of greater magnitudes of action vs peers on energy-related moves. Pressure may also be a function of pricing into the Burnham coronation on Friday, as he will become UK PM from the point Starmer formally hands over. On that, Rathbones has reduced its Gilts holding in order to protect against “fiscal irresponsibility” ahead of Burnham and the Chancellor decision. Note, likely outgoing Chancellor Reeves speaks at Mansion House this evening.

- USTs also lower, down to a 108-17 trough given the energy move, which has seen a modest extension on the pressure after Fed’s Waller on Monday evening said another hot core inflation read would mean the Fed needs to consider a near-term hike. CPI today is seen at -0.1% M/M (prev. 0.5%), while the now even more pertinent core is seen at 0.2% M/M (prev. 0.2%). Following Waller and the recent energy moves, pricing for July has moved in favour of a hike, with around a 60% chance of a 25bps move currently implied. We now look to testimony from Chair Warsh, which is scheduled for after CPI; note, a text release alongside CPI is possible.

- BP (BP/ LN) says upstream production is expected to be between 2,170-2,220mboepd (prev. 2,339mboepd Q/Q), due to seasonal maintenance predominantly in the Gulf of America and the effects of disruption in the Middle East.

- Pakistan LNG is reportedly seeking an additional LNG cargo for July as US-Iran hostilities in the Strait of Hormuz constrain supplies from Qatar, according to Bloomberg.

- Turkey’s energy minister said Iraq requested retaining oil export capacity of 750K BPD through the Kirkuk-Ceyhan pipeline for 12 months under an agreement.

- Iran’s Oil Minister Paknejad said Iran’s oil exports continue as usual despite the US removal of oil waivers.

- Freeport-McMoRan (FCX) Indonesia unit is targeting 2026 copper production of 0.8bln pounds.

Central Banks

- RBNZ Chief Economist Conway said the Middle East conflict complicates monetary policy like all supply shocks, while he added that understanding how firms respond to cost shocks is crucial in maintaining low and stable inflation. Furthermore, he said that despite easing prices, the effects of the shock are expected to continue impacting the economy for some time, and that a further reduction in monetary stimulus is likely to be required.

- BoE Governor Bailey said that the core banking system in the UK is resilient and that debt levels are not stretched. He stated that renewed hostilities in the Gulf underline continuing instability. The UK's position is supported by its fiscal framework as well as monetary policy.

Geopolitics: Iran

- US President Trump reiterated that Iran has no air force, no navy and no military, while he said they will hit Iran very hard on Monday night and on Tuesday. Trump said they had a deal yesterday and that Iran breaks deals, as well as commented that the MoU was built to test Iran and that Iran didn't honour it. Trump also stated that they will hit 'Pickaxe Mountain' pretty soon and have their eyes on the site all the time, which is a good potential target

- US Central Command announced that it conducted and completed a third consecutive night of strikes against Iran, with US strikes reported in Bushehr, Bandar Abbas and Bandar Kangan, while explosions were also reported in Iran's Qeshm Island and Kish Island. More recently, there have been reports of explosions have been heard near Bandar Abbas, Bushehr and Choghadak.

- Details of US President Trump’s proposed Strait of Hormuz toll plan are still being finalised, according to Semafor, saying Trump is 'very serious about the tolls.

- Iran's armed forces have begun targeting US naval vessels in the Strait of Hormuz with cruise missiles, Al Mayadeen reported.

- Iranian Army Spokesperson said the Strait of Hormuz will not be open with US aggressions and war, SNN reported.

- IRGC said it targeted weapons warehouses, satellite communications centres, and US forces' housing building at Bahrain's Juffair base. Iran's army also targeted US military facilities and equipment in Kuwait with drones, as well as targeted a 'hostile' US vessel with cruise missiles, while it was separately reported that a US military base in Jordan was hit by a missile attack and that a missile attack hit an Iranian Kurdish opposition group site east of Iraq's Erbil.

- UKMTO received a report that a tanker was hit by an unknown projectile 40NM northeast of Qalhat, Oman. UKMTO reports of an incident 13NM southeast of Lima, Oman, the tanker was reportedly hit by a missile transiting outbound on the southern route

- The UAE Defence Ministry reported that two national tankers were targeted by Iranian cruise missiles in the southern Strait of Hormuz, with the incident occurring in Omani territorial waters, although the fires on both tankers were brought under control, and it reserved the right to respond to the escalation.

- ADNOC confirmed tankers "Al Bahyah" and "Mombasa B" were hit in the Strait of Hormuz.

- Oman’s Foreign Minister said complex talks are under way to make a long-term arrangement to guarantee freedom of navigation through the Strait of Hormuz.

Geopolitics: Ukraine

- Russian ballistic missiles targeted Ukraine's capital of Kyiv, with sirens and explosions heard across the Ukrainian capital, according to FT.

- Russian forces conducted group strikes at night, damaging military industry and enterprises involved in missile production in Kyiv, while it damaged infrastructure facilities in Odessa, used to store Ukrainian armed forces' fuel and lubricants.

- Ukraine Navy spokesperson said Russia struck a civilian vessel near Ukraine’s Black Sea port of Odesa. Additionally, Ukraine said it struck two Russian oil refineries in the Bashkortostan and Krasnodar regions.

US Event Calendar

- 6:00 am: Jun NFIB Small Business Optimism, est. 95.7, prior 95.3

- 8:30 am: Jun CPI MoM, est. -0.11%, prior 0.5%

- 8:30 am: Jun Core CPI MoM, est. 0.2%, prior 0.2%

- 8:30 am: Jun CPI YoY, est. 3.8%, prior 4.2%

- 8:30 am: Jun Core CPI YoY, est. 2.8%, prior 2.9%

- 4:00 pm: May Total Net TIC Flows, prior 26.1b

- 4:00 pm: May Net Long-term TIC Flows, prior 103.1b

Central Bank Speakers

- 10:00 am: Fed Chair Warsh Testifies at House Financial Services Cmte.

- 12:40 pm: Fed’s Barr Speaks on Artificial Intelligence

- 1:00 pm: Fed’s Goolsbee in Fireside Chat

- 1:30 pm: Fed’s Cook Speaks at Conference on Financial Inclusion

- 2:55 pm: Fed’s Bowman Speaks at Conference on FInancial Inclusion

DB's Jim Reid concludes the overnight wrap

The most striking financial market takeaway is the extraordinary shift in Japan’s relative affordability over the past decade and a half. When we launched the series in 2012, Japan was one of the most expensive countries in the world, while the US sat towards the cheaper end of the spectrum. Today, that picture has completely reversed. Tokyo is now the cheapest city in the world in which to buy an iPhone, you can almost get two dates there for the price of one in London, enjoy three meals out for the cost of one in Zurich or New York, and buy property at a fraction of the prices seen in New York, Hong Kong and London. With Japan’s PPP-implied price level falling from 125 in 2012 to just 60 today, the report poses an intriguing question: if reading the 2012 edition would have encouraged you to buy America, should reading the 2026 edition make you take a fresh look at Japan? Tens of thousands of data points have been analysed to compare relative prices across 69 cities that matter to global financial markets. Click here to see where your city ranks on everything from everyday prices to overall quality of life and click now to get ahead of the 45,000 readers who might already be planning next year’s bargain holiday. Tokyo, perhaps?

Staying in Asia, markets are again weak this morning on the back of the escalating tensions in the Middle East and the softening sentiment towards the AI trade. Oil is up just under another couple of percentage points this morning having been up around 9% yesterday. More on that below. The KOSPI (-0.02%) has actually fought all the way back to flat after being down -5% an hour ago when I started work on this. It might still be an hour until you read this so you may want to check yourselves. Elsewhere, the Nikkei (-0.25%) has been much less volatile but has also been recovering while I type. The Hang Seng (-0.47%), the CSI 300 (-0.39%), and the Shanghai Composite (-0.66%) are also lower. S&P 500 (-0.09%) and NASDAQ 100 futures (flat) have also been recovering as the overnight session has progressed but with Stoxx (-0.6%) futures still lower.

Today we have a huge day with US CPI, Warsh’s testimony to the House and the unofficial start of Q2 US earnings season with 5 big banks reporting.

Ahead of this and all the overnight moves, the big story yesterday was the latest jump in oil prices, which revived fears around stagflation, and hit bonds and equities on both sides of the Atlantic. That followed further strikes between the US and Iran over the weekend, which meant Brent crude (+9.59%) saw its sharpest rise since March 2020, reaching a 4-week high of $83.30/bbl by the close. Moreover, yesterday saw a fresh escalation in the rhetoric, with Trump saying that “We’re taking over the Strait”, before announcing that the US was reinstating an “Iranian blockade”, which Trump said was “so named because it is only stopping Iran’s ships or customers from entering or leaving. All other countries will have fair and open use of the Strait.” He also said that the US would “be reimbursed, at the rate of 20% on all cargo shipped, for any and all costs necessary to do the job of providing safety and security to this very volatile section of the World.” I asked AI how much that could raise if you assumed pre-war volumes. It came back with a figure of around $400-500m a day based on $2-2.5bn of daily cargo passing through the Strait.

President Trump has a habit of starting with an extreme negotiating position so no doubt this would come down if it was ever implemented, but the very spectre of tolls will make markets and customers nervous. US Central Command said that it will resume the Iran blockade at 4pm NY time today, so that still leaves a bit of time for a possible climbdown. Yesterday’s mood out of the Middle East also wasn’t helped by escalation between Saudi Arabia and the Houthi rebels, with the latter targeting a Saudi airport after the Saudi-backed Yemen government carried out strikes against Sanaa airport.

The escalation over Hormuz saw inflation concerns creep back into play yesterday, with investors pricing in more rate hikes from central banks. For instance, pricing of a Fed hike in just a couple of weeks’ time jumped from 34% to 43% yesterday and the amount of hikes priced by the December meeting was up +5.4bps on the day to 43bps. The Fed repricing was also supported by some hawkish comments from Governor Waller, who kept the door open to an imminent hike, saying that “If we get another hot reading on core inflation this week, then the FOMC will need to consider tightening monetary policy in the near term”. Similarly for the ECB, the number of hikes priced by December was up +10.5bps on the day to 44bps, so it was clear that higher oil prices were shifting market pricing in a hawkish direction.

This backdrop also had a clear effect on sovereign bond yields, which continued to move higher on both sides of the Atlantic. So for US Treasuries, the 2yr yield (+7.6bps) closed at a 16-month high of 4.28%. And notably, the 2yr real yield (+2.2bps) closed at 2.23%, which was its highest closing level in almost two years. Meanwhile the 10yr yield (+6.3bps) was also up to 4.62%, marking its highest level in nearly two months, and the 10yr real yield (+3.6bps) closed at 2.34%, its highest since 2023. And over in Europe, yields on 10yr bunds (+4.3bps), OATs (+5.5bps) and BTPs (+7.0bps) all moved higher as well.

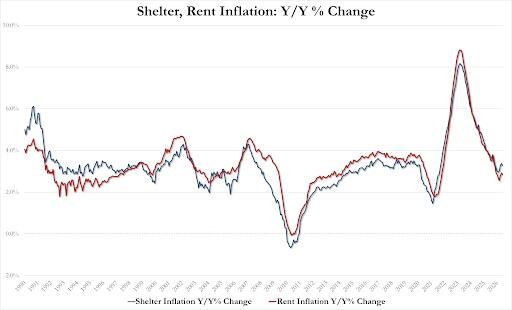

Looking forward, the question of Fed rate hikes will be in focus today, as we’ll get the US CPI print for June at 13:30 London time. This is a significant one, because market pricing for the next Fed meeting is still in the balance, so any surprises could easily push that in either direction. In terms of what to look out for, the recent decline in gas prices means our US economists expect headline CPI to come in negative for June, with a monthly price decline of -0.16%. So if realised, that would take the year-on-year rate down to +3.8%. But core CPI is expected to still be more resilient at a monthly +0.23%, with the year-on-year rate at +2.8%.

Whilst the CPI print will be the initial focus, attention will then shortly turn over to Fed Chair Warsh, who’s testifying before the House Financial Services Committee at 15:00 London time. That’s part of the regular semi-annual testimony from the Fed Chair, with the Senate Banking Committee hearing taking place tomorrow as well. But our US economists expect him to remain reticent about providing guidance for any upcoming policy action and remember that Warsh was the one official who didn’t submit a dot in the most recent dot plot.

Whilst sovereign bonds were struggling, it was also a rough day for equities as the rise in oil prices coincided with a fresh slump for chip stocks. The Philly semiconductor index (-4.78%) fell back sharply, with the NASDAQ (-1.55%) also pulling back. And in turn, that slump for tech stocks dragged on the S&P 500 (-0.79%), with the index posting a sizeable decline despite most of its constituents rising on the day. Meanwhile in Europe, equities put in a relatively better performance, given the region’s comparatively smaller concentration of chip stocks and as European markets closed before the full rise in oil prices, with the STOXX 600 only down -0.01%.

Finally, China’s latest trade data surprised to the upside overnight, with both exports and imports growing significantly faster than expected in June. Strong global demand for AI-related products and technology goods helped offset increasing geopolitical pressures. Exports rose 27.0% year-on-year, surpassing expectations of 19.0% and accelerating from May’s 19.4% growth. Imports increased 36.0%, well above the forecast of 26.1% and stronger than the previous month’s 27.4% rise. As a result, China’s trade surplus widened to $125.62 billion in June from $105.43 billion in May, exceeding market expectations of $120.10 billion.

Looking at the day ahead, and the main data highlight will be the US CPI print for June. Otherwise, Fed Chair Warsh will be speaking before the House Financial Services committee, and we’ll also hear from the Fed’s Barr, Goolsbee, Cook and Bowman, along with BoE Governor Bailey. Finally, today’s earnings releases include JPMorgan, Citigroup, Goldman Sachs, and Bank of America.

Tyler Durden

Tue, 07/14/2026 - 08:24

Bill Gates with an unidentified but manifestly well-proportioned brunette number, in a photo from the Epstein files (House Oversight Committee)

Bill Gates with an unidentified but manifestly well-proportioned brunette number, in a photo from the Epstein files (House Oversight Committee)

A health worker at a mobile COVID-19 vaccination station in a shopping mall fills a syringe with the Pfizer-BioNTech vaccine in Ludwigsburg, Germany, on Nov. 11, 2021. Thomas Kienzle/AFP via Getty Images

A health worker at a mobile COVID-19 vaccination station in a shopping mall fills a syringe with the Pfizer-BioNTech vaccine in Ludwigsburg, Germany, on Nov. 11, 2021. Thomas Kienzle/AFP via Getty Images

via Reuters

via Reuters A man cools himself during a heatwave in Chamonix, France, on June 25, 2026. Reuters/Pierre Albouy

A man cools himself during a heatwave in Chamonix, France, on June 25, 2026. Reuters/Pierre Albouy A Dash Q400-MR Fireguard aircraft of the civil security drops retardant mixed with water during a demonstration of firefighting capacity by the Gironde's Fire and Rescue Departmental Service in Saint-Aubin-de-Medoc, France, on July 3, 2026. Christophe Archambault/AFP via Getty Images

A Dash Q400-MR Fireguard aircraft of the civil security drops retardant mixed with water during a demonstration of firefighting capacity by the Gironde's Fire and Rescue Departmental Service in Saint-Aubin-de-Medoc, France, on July 3, 2026. Christophe Archambault/AFP via Getty Images

Recent comments